The Investment Banking interview guide to Barclays LIBOR scandal

There is a simple question being asked within financial circles these days. When the dust settles what would be the final tally (toll) of the LIBOR scandal?

To answer this question you have to get involved in a larger debate. One that crosses over the boundaries across perceived liability, the ability to collect damages and the willingness of the regulatory system to impose penalties and sanctions when such sanctions threaten its own existence.

This “larger” debate raises even more questions.

1. Is the fuss over? With the resignation of Bob Diamond as well as the fall of the Chairman of the Board of Barclays Bank will this scandal die down and leave Barclays and other banks alone?

The short answer – No.

2. If a civil suit is filed, who will lead it and where will it come from. What would be its impact?

There is no longer an if or a who. The only question now will be how much and when?

3. What will happen to Barclays Bank? Will it go the way of Citi and AIG and become part of the living dead? Or will it go the way of Bear, Lehman and Enron and become part of an HBS case study? Or will it come out golden and untouched just as it did a few years ago by cutting opportune deals for raising capital in the Middle East at the peak of the financial crisis?

Let’s see what history can tell us about Barclays future prospects…

Barclays LIBOR crisis. Establishing guilt.

The evidence is quite clear. If you have been sitting on the sidelines wondering which side to take, all you have to do is read the FSA report on the scandal.

The FSA report is very clear. Everyone did it, inclusive of Barclays. It adds a new term to our exotic financial vocabulary – “clean, clean” versus “dirty, clean”. We are no longer debating if a wrong was done. Neither are we arguing that it was a onetime oversight or a bad judgment call made by a few over ambitious bankers that have now run through their swords and have been conveniently dispatched to colder pastures.

There is documented evidence of manipulation, reporting of said manipulation to the regulators involved, compliance calls, misrepresentation and inaction over a four year period. This is not an oversight, a mistake or a bad judgment call. In any criminal court repetitive criminal behavior with intent and knowledge of impact of that behavior over a four year period would lead to the harshest possible sentencing. Why should banking be any different?

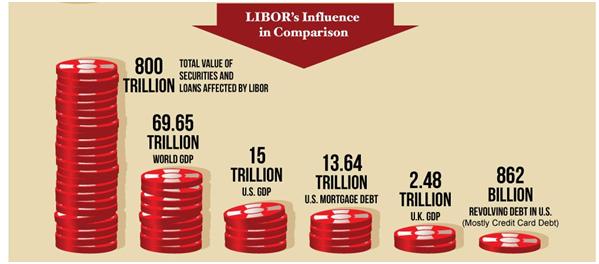

Barclays Libor crisis, establishing impact. Mispricing 800 trillion USD of notional.

Figure 1 – Barclays Libor Crisis. Total exposure to LIBOR

Why does it matter? An interest rate is an interest rate, what difference do a few basis point here or there make between friend in London. Enough has been said about how lower quoted rates impacted everyone, not just the banks involved (take a look at our infogram collection at the end of this note). But what’s the impact? Mispricing 800 trillion of notional principle leads to some very large numbers. Numbers large enough to trigger debate and engage public imagination.

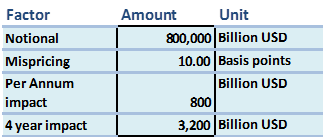

Figure 2 – The math behind large claims

While 3.2 trillion US dollars in damages is very interesting, is it likely to be awarded?

No.

You have to remember that the 800 trillion exposure number is the gross notional number, the net number is going to be lower. For example if I have one USD 300 million paying fixed interest rate swap and decide to unwind it with a receiving fixed rate swap of the same notional amount, my gross notional number is 600 million, my net number is zero.

According to Forbes, Nomura securities (Schorr and Joshi) estimates that of the 126 trillion Swaps outstanding about 26 trillion are just between primary dealers (unlikely to sue each other) leaving us with a gross notional amount of 100 trillion.

They further reduce it to 6 trillion US$ after adjusting for US jurisdiction and estimate a penalty exposure ranging between 18 – 36 billion USD across the submitting banks on the BBA USD Libor panel, if the court decides against them.

The same exercise needs to be repeated for each individual slice of the market for floating rate notes, structured notes, investment deposits and bonds. However if the Nomura Swap estimate is anything to go by, the total exposure across the submitting bank could easily exceed 250 – 300 billion USD in penalties and damages. It may actually turn out to be larger because with notes, debts and deposits there would be no netting involved.

Admittedly a court will look at actual ownership of underlying assets, US jurisdiction, opportunity cost and the impact of a misquoted rate from a member on the panel on the actual Libor rate set for that period or later.

European and Asian counterparties and other primary dealers in these markets are unlikely to sue. Europe is still very much a closed institutional loop and the banks on the BBA panel have enough influence and connection to forestall such challenges.

The swap estimate and the reduction from 100 trillion to 6 trillion (and extrapolation) factors that in. But a US class action suit (the direction these civil suits are likely to take) could easily grow to troublesome dimensions for any one individual bank. More so if the court decides to award punitive damages.

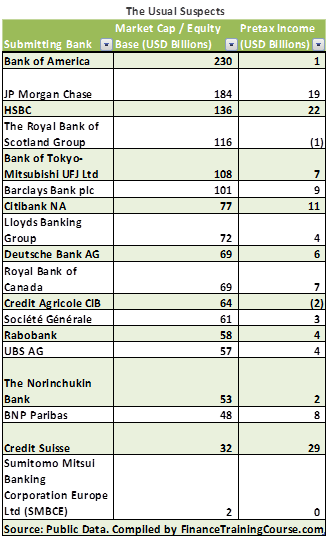

The usual suspects, the banks on the USD LIBOR Panel

The BBA Panel for USD Libor can be categorized under the following four segments.

a) State “owned-rescued” recoveries in progress (BAML, Citi, RBS, and perhaps Lloyds)

b) The healthy (JP, HSBC, Barclays)

d) The irrelevant (everyone else)

Figure 3 – The USD LIBOR BBA Panel

The healthy are the only one with meat and fat on the bone that a legal team would like to target.

While a civil suit may name all of them as counter parties, smarter money would go after the ones that really matter and will have something of value to settle with. A bank with nothing to give will simply give up and take the easy way out by either going under or seeking bankruptcy protection.

It is a defense that has been exercised before in the oil industry and may certainly be used by banking industry, though the cost of seeking bankruptcy protection are likely to be much more traumatic for a bank than they were for Texaco. Unlike a cash rich, profitable petrochemical giant, a bank can’t keep on operating with business as usual if it has just sought bankruptcy protection.

The three targets that then fit that bill are JP Morgan Chase, HSBC and Barclays. If you sued RBS, Bank of America Merrill Lynch and Citi you will effectively be taking the British and US governments to court. Even if you ignored the state ownership aspect, there is really nothing left at these three entities that you could go after as a claimant.

The case against Barclays

The smartest money in town would go after Barclays only because it is the easiest of the three to target and close. JP Morgan Chase and HSBC have their own unique posture (large international retail foot print, sizeable war chest for a legal defense) that makes them an unlikely successful target (more on that later) and unlike Barclays their culpability still remains to be proven.

So let’s look at the odds against Barclays.

It is the smallest of the group of three and the only one so far to be penalized under the joint FSA, US Treasury and Federal Reserve settlement.

Bob Diamond testimony at the parliament and Barclays attempt to drag the Exchequer, the FSA and the “higher authorities” down with it hasn’t won it any friends or support. In fact when Barclays will most likely need a moment of understanding, spine or forbearance from the regulator, it will most likely find itself alone and abandoned.

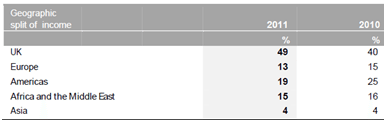

Barclays is still a British Bank with its largest exposure to the UK market. It has limited exposure to North America and a limited fall out radius in Europe. In US courts, its failure or demise will not represent a threat to the US or European financial system.

Figure 4 – Barclays split of income across geographies

In the end the only thing that stands between Barclays and the mob of lawyers is government intervention and indirect support that only the FSA or the Exchequer can provide . The Fed and the US Treasury is unlikely to support a soft stance for many reasons.

a) There is the old Lehman score that some would like to settle with their British counterparts.

b) The “make a shining example” paradigm that has driven US regulatory action for the last two decades. I don’t think they will make an exception in the case of Barclays, more so if the FSA stands back and doesn’t intervene.

c) Middle Eastern money always helps your cause when it comes to regulatory action (historical precedence?). The GBP 11 billion in capital the bank raised in 2008 may actually come back to haunt investors as well as shareholders. While Barclays has some political clout that clout is likely to backfire and disappear if a broad class action suit is filed by the likes of CalPERS, State and US Municipal governments.

The civil suits have already started. They will pick up pace. They will go the class action route and while some may take years to settle, others will have an immediate impact on survival prospects of the banks involved.

Barclays Libor Crisis. Future Timeline and Triggering events

Figure 5 – British Bank. RBS, Lloyds, Barclays stock returns

Unlike the mortgage crisis and the bankruptcy of Bear and Lehman, contributing banks involved in the Libor crisis are with a few exceptions deposit taking institutions. They have deeper pockets and are less reliant on the fickleness of the interbank market. Unless a bank run develops on account of regulatory action there is less of a chance that a bank like Barclays would actually shut down.

However Barclays does have GBP 27 billion of Term maturities (read: institutional lines) coming up in 2012 as well as 265 billion in wholesale (largely unsecured) debt as per their 31 December 2012 annual report. Under normal conditions, these would automatically rollover but a few more penalties and a handful of adverse judgments can turn the sentiment of the market and the future prospects of the bank. While the balance sheet suggests that wholesale debt pool is secured by a matching liquidity pool, the mismatch between the two, at 80 billion and change, can become a significant headache for the bank if a judicial event triggers the material adverse deviation clause.

If Barclays board shares this prognosis the first confirmation we will see will be the sale of the Barclays Investment management and European Retail Business, both with significant losses in 2011. You may even see unsolicited bids for Barclays Capital come in.

Barclays also has GBP 530 billion of gross notional exposure in derivative contracts. While net exposure is about GBP 40 billion, it stands at risk of taking significant mark downs on a mark to market basis if counterparties start unwinding these positions in anticipation of an eventual crisis at the bank.

If I know that you have a portfolio of a specific ill-liquid positions that will be unwound because of expected future stress, sharp money would be to get them out of your portfolio, as early and quickly as possible. Sharper money would be to keep on shorting the positions and force Barclays to eventually get out. Derivatives settlement and netting is exceedingly sensitive to changes in your credit grade and standing and as more rating agencies cut Barclays rating, the derivative exposure would start becoming a problem.

First because it would start bleeding cash in additional margins and then eroding P&L equity on a mark to market basis.

Once again a second confirmation of corrective action from the bank would a be a significant reduction in net derivative exposures by the bank.

The two triggers can work both ways. It can be interpreted as an indication of battle stations at the bank as well as a trigger event for a less rosy future at a franchise established over the last thirty years.

The third and final trigger would be the well tried and time tested defense of buying time by declaring healthy (healthier) profits and assuming the posture that the bank has enough margins, reserves and cash to forestall any or all of the above. Bank generally keep items in hard to reach accounting classifications for rainy days that could be used to shore up profit warnings and income shortfall. Bear and Lehman both tried and used it four years ago, Barclays will be the most recent client of this tactic.

Will it work? We don’t know.

Having said that, Barclays is not new to difficult times. Its ability to raise investment from Qatar was viewed as a coup by many. It has weathered similar crisis before. Barclays Capital rose from nowhere to visibility in the last decade. They have done this before.

The primary question is, will it be able to fare similarly in 2012 without the support of its domestic regulator.

Annexures

In good company

HSBC, along with HBOS the bank subsidiary of Lloyds also mentioned in its 2011 annual reports that the future liability wrt. these lawsuits is uncertain.

JP Morgan is being examined for the alleged fixing of Libor, Tibor (Tokyo Interbank Offer Rate) and Euribor rates in 2007-08.

Japan’s financial regulators are more focused on CITI group citing that they found a trader moving from UBS to Citi who attempted to manipulate TIBOR.

Charles Schwab, the discount brokerage and money manager has mentioned 11 banks in two lawsuits for rigging the benchmark rates. Bank of America being one of them.

The Bank of Tokyo-Mitsubishi UFJ suspended two traders who were based on. The bank is currently under investigation by the Swiss Competition Commission for suspicion of rigging.

Swiss Competition Commission is scrutinizing Credit Suisse about traders grouping together to manipulate the derivatives spread of bid-ask.

According to Der Spiegel, two employees at Deutsch Bank have been suspended after external auditors probed into the possibility of rigging.

Lloyds has been more upfront on this issue. In May, it officially suspended two derivatives traders for the possibility of rigging.

The traders suspended in Bank of Tokyo- Mitsubishi UFJ worked previously at Rabobank. This led the regulators to include Rabobank in their investigation as well.

RBC, Canada’s largest bank as well as RBS are also under investigation. Last month a newspaper report mentioned that RBS could face a 150 million pound.

UBS, the Swiss bank mentioned that it is cooperating on the assurances of the regulators granting leniency if any rigging claims turns out to be true.

German Bank West LB in July 2011 had requested to be dropped from the panel of banks that contribute to setting of Libor for USD.

Norinchuckin, the Japanese bank was one of the 12 banks sued by FTC Capital asset management in April 2011 for attempting to influence Libor.

Related Materials

Liquidity Risk Management Framework for Banks

Lehman Brother Failure: Timeline to Insolvency

AIG: The race to ground zero

References & Sources

http://www.equities.com/news/headline-story?dt=2012-07-28&val=320031&cat=finance

http://www.cityam.com/latest-news/libor-crisis-spreads

http://www.citigroup.com/citi/investor/quarterly/2012/ar11c_en.pdf

http://files.shareholder.com/downloads/ONE/1996056988x0x556139/75b4bd59-02e7-4495-a84c-06e0b19d6990/JPMC_2011_annual_report_complete.pdf

http://www.hsbc.com/1/content/assets/investor_relations/hsbc2011ara0.pdf

http://www.huffingtonpost.com/2012/07/11/libor-rate-scandal_n_1664737.html

LIBOR Crisis Infograms.

Libor Scandal Explained, courtesy of AccountingDegree.net

LIBOR Rigging scandal courtesy HealthCareAdministration.com