Valuing and marking to market over the counter interest rate (IRS) and cross currency swaps (CCS) has always been a painful topic. Model assumptions, liquidity and open interest in any given tenor vary from one valuation interval to the next and there is generally a big issue around model transparency and dependability on the executing bank for rates. God forbid if you need to unwind early or seek termination before the scheduled end date. To this context add Value at Risk for swaps. How can you calculate VaR for a security where you are not sure about the final liquid exit price?

Pricing IRS & CCS using Monte Carlo Simulation – The Problem

Once upon a time in a different life, we wrote a model for valuing a portfolio of IRS and CCS positions using Monte Carlo simulation. It worked perfectly in an ideal world. It was a disaster in the real world. Let’s just say that we were naive and simple and hopelessly confused and the model was much worse.

The primary problem with using Monte Carlo simulation for determining the value at risk for swaps (IRS and CCS) is that rates (FX & Interest rates) are not normally distributed. The same is also true for all other price risks. However, for vanilla instruments we are lucky to have trade prices that can be used to calibrate the pricing and VaR model. That is unfortunately not always true for IRS and CCS exposures. This means that the model is already out of alignment and drifts even further from reality as we pile on assumptions after assumptions.

A historical simulation model for calculating Value at Risk for Swaps

The solution is a simple tweak in the valuation model itself. Here is the model that we finally evolved after a number of high profile drubbings by the trading desk and the sales team. Not that this model is any better but it is an improvement as it uses the actual distribution of results rather than an assumed normal or log normal distribution.

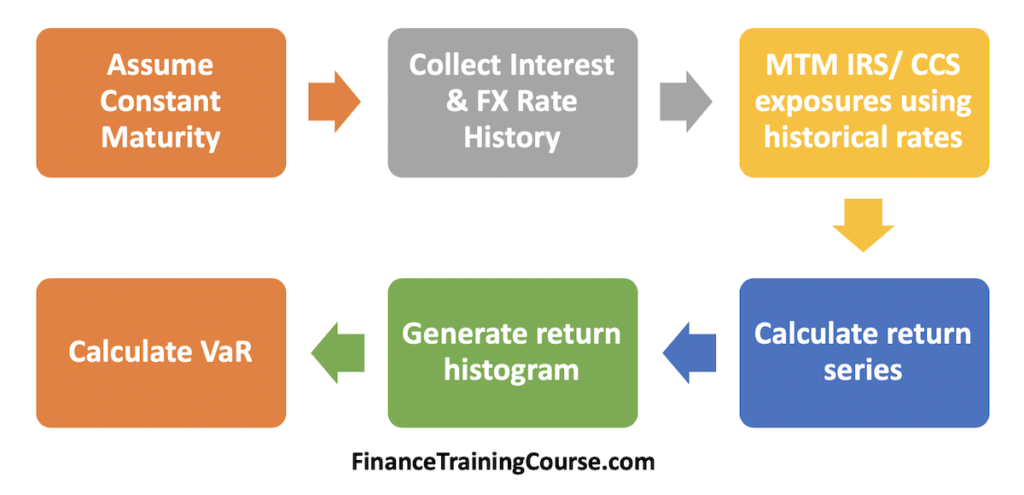

Calculate the value at risk for swaps using the following steps:

a) Assume that the swap will retain the same life (constant maturity).

b) Collect historical interest rates and currency rates for the last 2 – 4 years.

c) Use historical rates to mark to market the constant maturity swap. Generate a historical (simulated) price series for the IRS/CCS.

d) Use the simulated price series to calculate daily returns over the last two years.

e) Generate a Histogram from the daily return series.

f) Use the Histogram to calculate Value at Risk for the swap using the historical simulation approach.

One note of caution though. This is a full valuation approach which for a single IRS and CCS turns out to be a handful. If you have a large portfolio, your safest (possibly only bet) is a platform or software that does all the valuation, bootstrapping, curve building work for you. Doing all of that in EXCEL will quickly become a tedious exercise.

See the MTM & Valuation of a simple Interest Rate Swap post for the valuation model and the Bootstrapping Zero and Forward Curves from treasury term structure data post for building the underling interest rate model.

Comments are closed.