While we have shared a great deal about Simulation Modeling and Analysis on this blog, over the years, I felt it would help to finally have some organization around this topic. The need became more apparent when I ran sessions in Singapore, Abu Dhabi & Dubai for my students on Monte Carlo Simulation and realized that there was no one resource page that I could direct my students to.

A fair warning before you proceed.

Almost everything here deals with Finance or distant relatives. I flunked Physics twice in my life and the memory still traumatizes me. So no engineering, design, ASIC or basic electronic simulations from yours truly. I did write microcode in another life but couldn’t find a strong enough connection to cold hard cash and quit early.

Second, financial simulation models (mostly) trace back to good old Black Scholes analysis. In other words Geometric Brownian motion and normal distributions. While the mathematics is a combination of non-decipherable Greek and Latin symbols, the Excel implementation is deceptively easy, once you get your mind around the concept.

Guess what we will be doing on this page? Excel implementations.

Also due to a good friend, I recently learned that I had spent a large part of the last decade modeling noise. I didn’t want it to be a surprise for you a decade later so let me be upfront. We will be modeling noise. Nothing earth shattering or important, just noise.

And if you think the signal is sophisticated and important, we have got even better news for you on that account.

It is constant. Simply because in the Black Scholes world, expected return is the primary signal, while volatility serves as a proxy for noise. And expected return in our simulation world is the risk free rate less one half variance (if that doesn’t make any sense to you, don’t worry, by the time we are done, it will sound like sheer poetry).

Here are the whiteboard notes/scratchpad from my lecture on Simulation Modeling – Monte Carlo Simulation for Finance, if you have had enough.

Putting Monte Carlo Simulation Models to work

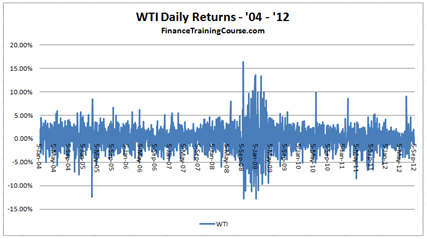

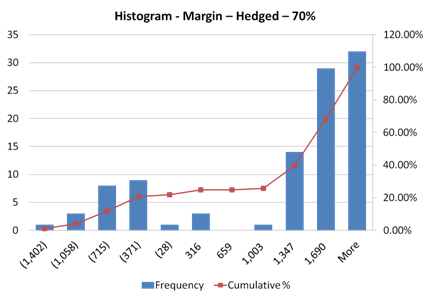

Despite that simplicity, Monte Carlo Models can take something as basic and chaotic as a return series for crude oil and

produce something as powerful and elegant as a profitability distribution for the fuel hedging strategy for a leading airline. Which becomes useful when you have a board presentation and need something intuitive, relevant and powerful to show.

It’s not always easy. It takes a bit of effort and we hope we can show you how to get it right. Welcome to our brand new resource page on Monte Carlo Simulation Methods.

Simulation Models – Monte Carlo Simulation Objectives

Like all analysis tools, simulation allows us to understand problems we are trying to analyze. Sometimes we can use this tool to help our audiences better understand solution and recommendations. Sometimes the primary beneficiary is the person building the model, because by definition structuring and sculpting the model brings us closer to the problem and its probable solution.

For example, there are two primary uses of Monte Carlo Simulation that we cover on this blog. The most popular one is option pricing, the second (unpopular by a notch), is risk management.

Within risk management, we have appeared to have fallen in love with the fuel hedging case. This is a challenge for transportation, logistics, supply chain providers but the highest visibility this problem receives is within the airline industry. We have learnt a great deal about crude oil, the airline industry and variable ticket pricing by trying to forecast fuel expenses by simulating crude oil prices.

Simulation Models – What do we cover

We thought it would be useful to build two separate detailed step by step case studies for our primary applications. First fuel hedging and then using the output generated by the fuel hedging case study, a second one on pricing and comparing options used to hedge crude oil. There is some advance materials on tweaking Monte Carlo Simulation and hacking convergence as well as our all time favorite series on using Monte Carlo Simulation to decode Option price sensitivities, or Greeks.

But before all of this comes the theory:

The very first post is the series is our old Monte Carlo Simulation page, which is still very popular. If you are ready to move beyond where we were with Simulation Modeling a year ago, read on. If you have already seen the old page, feel free to skip to the next section.

Monte Carlo Simulation – Cases, Context, Analysis

- Simulation Modeling – The Refinery Case study – Session Transcript

- Simulation Modeling – Aviation – Airline Hedging Case Study – Context & Data

- Simulation Modeling – Aviation – Airline Hedging Simulation Model

- Simulation Modeling – Hedge Effectiveness Calculation – Presenting Results to Board members

Monte Carlo Simulation Models – How To

- Simulation Model – Fuel Hedge – Model Ground work

- Simulation Models – Fuel Hedge – Model Building – First Pass

- Simulation Models – Fuel Hedge – Linking Simulator & Financials

Option Pricing using Monte Carlo Simulation

- Pricing Exotic Option – Asian, Lookback, Barrier, Chooser

- Simulation Models – Pricing Ladder Options using Monte Carlo Simulations

- Pricing Exotic Options using Monte Carlo Simulations

Simulation Models – Advance Topics & Applications

- Simulation Models – Hacks – Switching distribution the original post

- Simulation Models – Hacks – Results from switching Normal with the historical distribution

- Simulation Models – Hacks – Quasi Monte Carlo

- Simulation Models – Risk – Delta Hedging Applications

- Simulation Models – Applications – Value at Risk for Swaps

- Simulation Models – Lessons – Understanding N(d1) and N(d2) – Video Course

- Monte Carlo – Hacks – Convergence