Option Pricing – Pricing Exotic Options using Monte Carlo simulators

This is our third post in the Exotic Option pricing using Monte Carlo Simulation series. We walk through the minor tweaks required in our Monte Carlo Simulation model to price Asian, Lookback, Barrier & Chooser Options.

Our assumption is that you have been following our prior posts on Monte Carlo Simulation presented earlier. Please see the two earlier posts in this series if you are not familiar with the material presented below. The term sheet used in pricing exotics is shared in the weekend pricing challenge.

Option Pricing – Using Monte Carlo Simulation to price Exotic Options – Introduction

Option Pricing – Pricing Ladder Options

Option Pricing – Weekend Pricing challenge

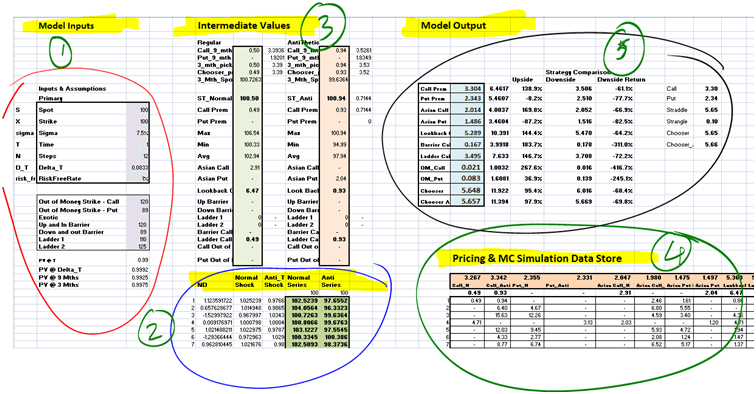

Earlier on we presented a sample snap shot of our Excel model end state.

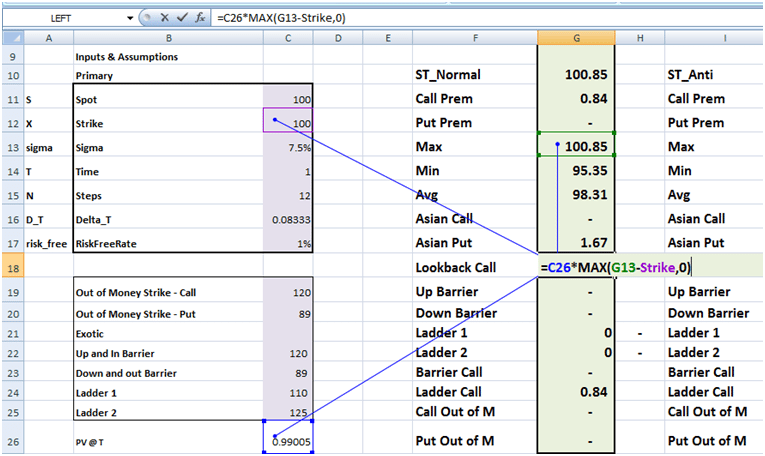

In this post we will focus solely on the Intermediate value section (Section 3, Intermediate values) where we estimate the payoff values for vanilla options, Asian, Barrier, Look back and Chooser Option. The process will remain the same as the one we have used earlier for pricing Ladder options. We will simulate a price series, evaluate intermediate values, calculate option payoffs and store the payoff results for a single iteration in an Excel data table. In our final step, we will calculate the average across all iterations (simulations runs) to estimate the true value of the option in question.

Some options will only need a single step calculations. Others such as Barriers and Choosers will require a multi step calculation. The multi step logic has been covered earlier on this blog. This post will simply share the marked up Excel snap shots from the Monte Carlo Simulator to show how the same principals used for pricing vanilla call options can be applied to price more exotic option contracts.

A quick note on the Anti-Thetic column. We use the Anti-Thetic technique to speed up convergence. Anti-Thetic sampling is covered in a separate note under the Monte Carlo Simulation how to reference.

Option pricing – Vanilla Call and Put Options and their exotic Asian and Look back cousins.

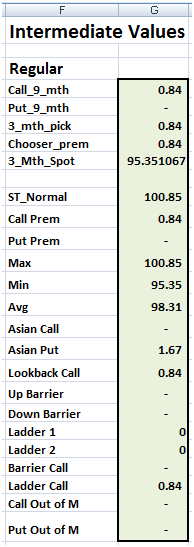

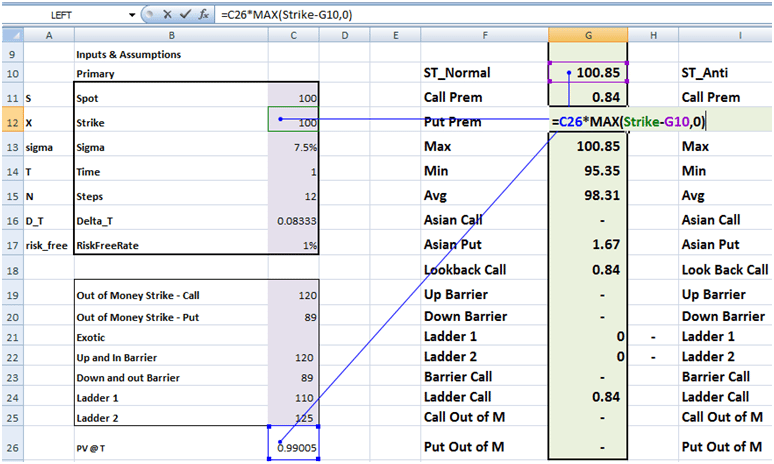

Our first step is to price a vanilla European Call or Put Option based on the simulated terminal price at the end of a single iteration. We repeat more or less the same process for Asian and Look back Options.

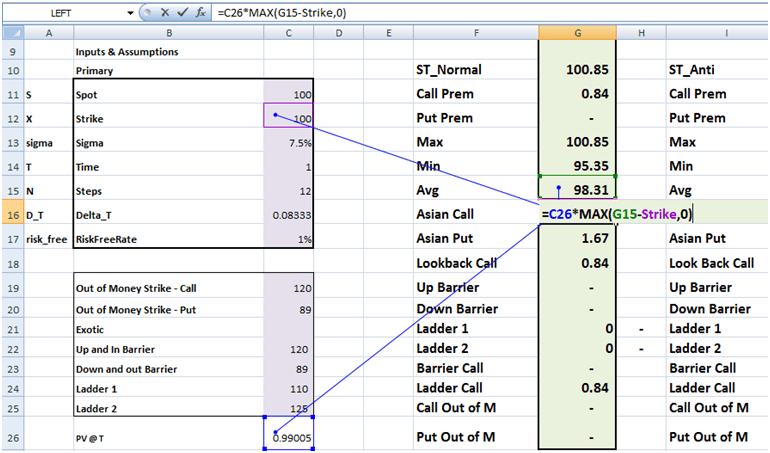

For Asian Options, the only thing that changes in the above model is that the terminal price is replaced by the average of the path simulated in that iteration.

For Look back options, the average is replaced by the maximum value touched by the path during the life of the option.

Option Pricing – Pricing Barrier & Chooser Options

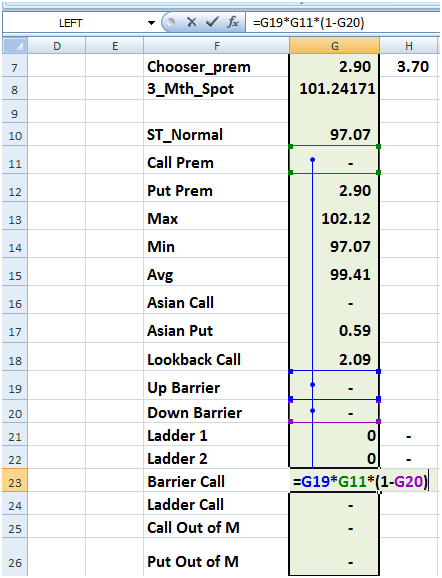

A barrier option (sudden death, knock in, knock out, single or double touch option) is a little more involved. We actually need to create and track a flag that gets turned on or off depending on if the barrier is touched during the life of the option. We then multiply the flag with the value of the regular call option. When we calculate the average the correct expected value is generated. You need a single flag for single touch and two for double touch barrier options.

Chooser and Compound options are even more involved than a barrier. Here is the sequence of steps we need to solve it

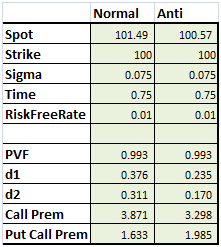

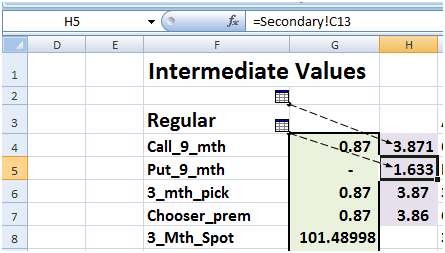

a) Create a secondary model on the side to price options at the point of exercise. The 3 month spot price for the secondary model comes from the primary simulator.

b) Plug in the values in Column H from the second pricing model at the point of exercise.

c) Use the secondary values to price the Chooser Option. We do this by first picking up the maximum of the two choices (rational choice), storing the results across iterations and then taking the average.

Comments are closed.