When was the last time you built a financial risk model in EXCEL? Do you remember wishing for a step by step guide? A model template? A translation of the differential equation from continuous to discrete spreadsheet friendly implementation? A risk spreadsheet that you could actually follow? From Option pricing to Value at risk; from Asset Liability Management to Treasury profitability analysis financial risk modeling EXCEL spreadsheets simplify our lives and make it possible for us to generate and test answers and analysis.

We do this by providing high level views of spreadsheet models; discrete spreadsheet friendly implementations and quite frequently a step by step guide to building a financial risk model.

The financial risk modelling spreadsheet guide is for do it yourself (DIY) types. If you enjoy building and testing models in Excel, you will find quite a few quick reference posts. If you don’t this is probably the last page you would want to spend time on.

Various Applications of Financial Risk Modeling

The collection below represents a comprehensive listing of what we have written on building risk, portfolio and banking spreadsheet models. The content is structured and organized based on topic popularity. The posts are generally short on text and words and long on content and value. Enjoy!

A financial risk modeling guide to calculating trailing volatility and correlation followed by a short post that tries to tackle the Gold bubble question? Is Gold overvalued? What can the relative pricing model tell us?

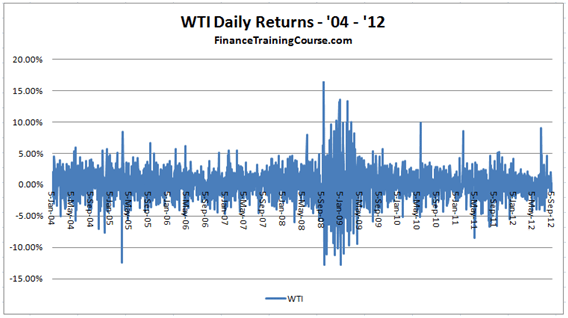

- Crude Oil Mispricing Model – Commodity Prices and a study in Trailing Correlations

- Relative Gold Price Model – Forecasting the price of gold

A short financial risk modelling guide to Asset Liability Management reporting templates, assumptions and conventions including a review of building Maturity and Liquidity gaps.

- Asset Liability Management – Earnings at Risk

- Asset Liability Management – Fall in Market Value of Equity

- Convexity & Duration calculator for US Treasuries

- Fixed Income Investment Portfolio Management & Optimization Case Study

- Asset Liability Management Case Study: Understanding ALM using simple training cases

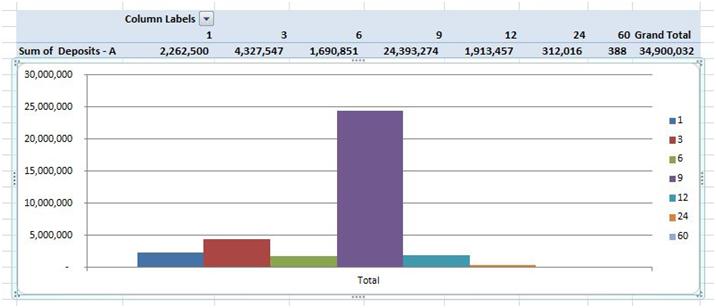

- Building Maturity Liquidity profiles for Deposits and Advances book for ALCO (ALM), ICAAP IAS 30 reporting

Interest Rate Models in EXCEL

Financial risk modeling may be used to forecast interest rates using one and multi-factor models in EXCEL

Cox Ingersoll Ross (CIR) model

Black Derman Toy (BDT) model

- Define Input Cells

- Define Output Cells

- Construct a short rate binomial tree

- Construct State Price Lattices

- Calculate Prices from Lattice

- Calculate Yields & Yield volatility from Lattice

- Define & Set Solver Function & Results

Heath Jarrow Merton (HJM) model

- How to conduct a Principal Component Analysis in Excel

- How to construct an HJM Interest Rate Model in Excel

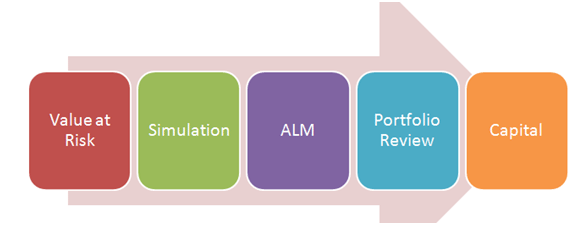

We use financial risk modeling to calculate VaR and other market risk measures.

Value at Risk

- Calculating Value at Risk (VaR): Step by Step Guide & Case study

- Value at Risk, Histograms and risk management in Excel

- Comparing VaR models, metrics and methods

- Calculating Conditional Value at Risk (CVaR) or Expected Shortfall – VaR and beyond

- Solved Solution – Value at Risk (VaR) Margin Lending Prime Brokerage Case Study

- Calculating Value at Risk for Options and Futures

Correlation

- Times series data graphs –Prices & More

- Scatter Plots

- The correlation coefficient, r

- Trailing Correlations

- Relative Price Graphs

Market Risk Metrics

- Holding Period Return

- Beta with respect to market indices

- Jensen’s Alpha

- Sharpe and Treynor Ratios

- Put Premium

- Portfolio Volatility

- Volatility Trend Analysis

Financial risk models that use Monte Carlo Simulation simulate oil prices, market prices, fuel consumption and fuel hedging results.

- Building your first Monte Carlo (MC) simulator model for simulated equity prices in Excel

- Monte Carlo Simulation Model How to – First pass

- Linking financial model to the simulation

- Simulating returns by replacing the normal distribution with historical returns

- Monte Carlo simulation methods – Tweaking the distribution

- Variance Reduction procedures: Antithetic Variable Technique & Quasi Random sequences

- Jet Fuel Aviation Hedge Case Study – Hedge effectiveness calculation

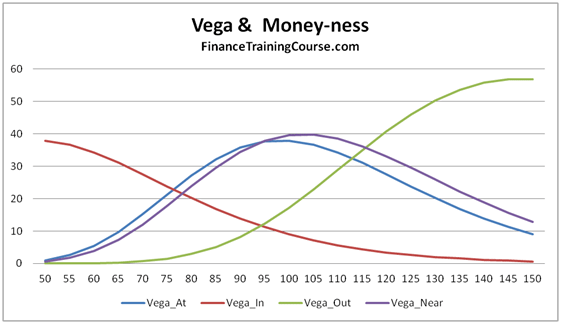

If the Greeks had you confused, we have the perfect Rosetta Stone for you. Bring Monte Carlo Simulation and good old fashioned accounting together to decode Delta, Gamma, Vega, Theta and Rho.

- Understanding Delta Hedging for options using Monte Carlo Simulation

- Dynamic Delta Hedging – Extending the Monte Carlo simulation model to Put contracts

- Dynamic Delta Hedging – Calculating Cash P&L (Profit & Loss) for a Call Option writer

- Hedging Gamma & Vega – The higher order Greeks hedge optimization Excel spreadsheet

- Delta Hedging applications for Rho, Rebalancing frequency & Implied Volatility

- Option Greeks – Dissection Theta and time premiums for call options

The big, thick, fat collection of posts on Option pricing financial risk models from pricing forwards, to exotics to swaps.

Forward prices and rates

- Computational Finance: Basics: Calculating forward prices in Excel – Part I

- More Forward Rates Lessons: How to calculate Forward Rates – Calculations walk through

- Forward lessons: Derivative pricing: How to calculate the value of a forward contract in Excel

Exotics

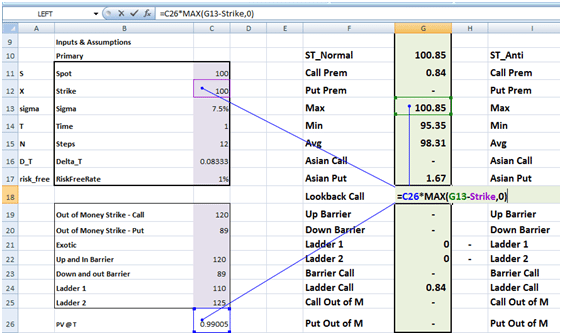

- Option Pricing – Pricing Exotic Options using Monte Carlo simulators

- Pricing Ladder Options using a Monte Carlo Simulator

Swaps

- Fixing the term structure

- Calculating the zero curve

- Calculating the forward curve Calculating the MTM of the Swap

- Pricing a Cross Currency Swap – Floating for Floating structure

- Pricing a Cross Currency Swap – Amortizing and Indexed Term sheets

- Interest Rate (IRS) & Currency Swaps (CCS) Value at Risk (VaR) with Historical Simulation – Excel Model walk through

- Practice Test Exam Question and Solution – Bootstrapping Zero and Forward Curves Case Study

- Practice Exam Test Question and Partial Solution – Pricing and MTM of Interest Rate Swaps (IRS)

- Pricing Caps and Floors