Computational Finance: Simulating Interest Rates using trees and Monte Carlo Simulation

2 mins read Simulating Interest rates using CIR and HJM While we can club equity, commodity and currency simulators in one category, interest

2 mins read Simulating Interest rates using CIR and HJM While we can club equity, commodity and currency simulators in one category, interest

2 mins read Linking Monte Carlo Simulation with Binomial Trees and the Black Scholes model A binomial tree uses the same process to

2 mins read My first interaction with a Monte Carlo simulation was not a very pleasant experience. It was an exam problem based

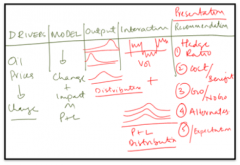

2 mins read We have introduced our friend mu (u) as drift and sigma as diffusion (or standard deviation or volatility or vol).

< 1 min read Extending MC simulation models to Currencies & Commodities Extending the original Monte Carlo (MC) Simulator for Equities to Currencies and

4 mins read Here is a slightly revised model for calculating the change in price of an equity security. We now add one more component to our generator function. While the first term works off expected return the second term will help us model uncertainty. Since in our world we drive and link uncertainly with volatility, our model also uses a factor proportional to volatility.