Risk Models, Option pricing & Bank Regulation training – 2013 guide

3 mins read Risk Models, Option Pricing & Bank Regulation training for practitioners A typical MBA program allows a candidate to take a

3 mins read Risk Models, Option Pricing & Bank Regulation training for practitioners A typical MBA program allows a candidate to take a

3 mins read Option pricing using Monte Carlo Simulation In our post on Option Pricing using Monte Carlo Simulation, we walk through a

2 mins read Exotic Derivatives & Option pricing weekend challenge This week exotic option pricing challenge focuses on chooser and compound option pricing

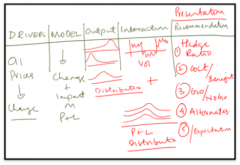

3 mins read Since we have a model for simulating oil prices, we are now ready to link our oil price model to

4 mins read While we have shared a great deal about Simulation Modeling and Analysis on this blog, over the years, I felt

3 mins read Monte Carlo Simulation Model – How To – Simulating Crude Oil Prices To simulate crude oil prices we will follow