Sales Journal and Sales Ledger

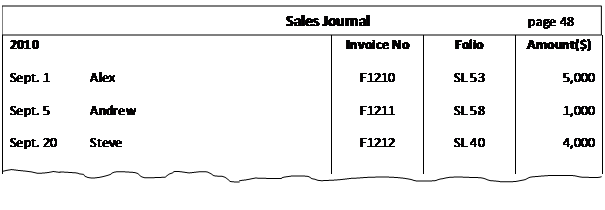

As explained above, the first point of recording all credit sales is the Sales Journal. Following is an excerpt from a Sales Journal.

Sales Journal excerpt

A sales journal typically contains date, customer’s name, invoice no, folio and amount of the sale. All the terms here, except for folio, are self-explanatory. Folio column in the sales journal is for our reference. It tells us where exactly the relevant account can be found. For example, on Sept. 1 we sold $5000 worth of inventory on credit to Alex. The folio of this entry contains ‘SL 53’ which tells us that this account can be found on page 53 of the Sales Ledger. Similarly, in the folio of the Alex’s account in the sales ledger we would expect ‘SJ 48’ written which tells us that this entry is on page 48 of the sales journal.

At the end of the each period the total of the sales journal is posted in the general ledger which contains an account for sales.

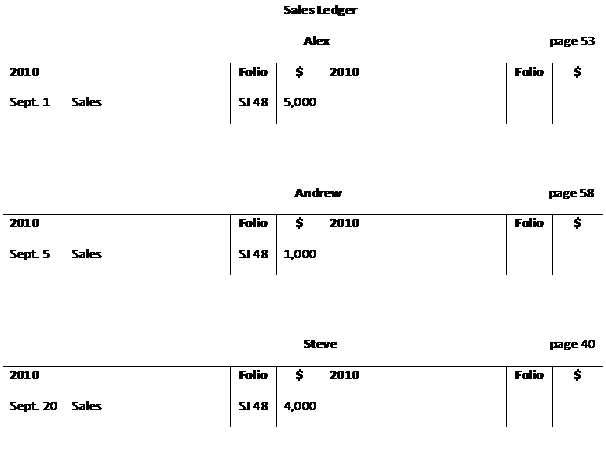

Having seen the sales journal at work, let us now see how sales ledger works as it is the next point for our credit sales transactions to go. This is where we find the T-accounts of all our account receivables. Following are the relevant accounts in the sales ledger that are mentioned above.

Sales ledger for Alex, Andrew and Steve

Note that the accounts above are the same as the T-accounts. They are looking different because of the inclusion of the folio column. Notice how easy our life becomes when we include the folio column in our accounts and also by the fact we are recording different transactions in different books.

Sorry for a non-committal answer, but the mmnageaent company will provide whatever you need them to. Do you need:Security: someone on-site 24/7 to allow access, access only during certain hours, or will you provide self-service automated access to the facility via codes or electronic means that does not require monitoring?Leasing: how will people rent storage space? On-site, on-line only, call you, call someone else? Who contacts them and negotiates lease renewals or other changes?Rent payments: Depends on whether you have on-site staff or not, but the manager will typically handle accounts receivable, cash collections, pay operating expenses, and perform general accounting and budgeting.Operations: do you want the manager to negotiate and manage maintenance contracts, procure insurance, pay real estate taxes, etc?Obviously the fee structure will depend on the amount of duties you are asking them to take on.