MFE 3F: Financial Economics Segment of Society of Actuaries EXAM M/ 3F of CAS

The following free courses on FinanceTrainingCourse.com cover various topics outlined in Society of Actuaries Learning Outcomes for Exam MFE, the Financial Economics Segment of Exam M and the CAS 3F exam. They provide supplementary prep materials for some of the more difficult concepts covered in the course.

As part of your preparation for your final attempt, you have been looking for anything that can provide the extra edge for your MFE / 3F attempt. While the material below was not prepared keeping the SOA curriculum in mind it takes a hands on excel based approach in illustrating the many concepts covered in the SOA MFE /CAS 3F exams. Our hope is that this extra bit will clear the final muddle about those elusive Stochastic calculus, Continuous Time Finance, Option Greeks & Delta hedging concepts that you had been struggling with.

The links below covers interest rate models (CIR and BDT), Binomial Trees, Black Scholes Model, Pricing Derivative securities, differentiating between N(d1) and N(d2), exotic product and options, interpreting Greeks, Delta Hedging, investment and portfolio management concepts and other related topics.

Please note that the material below does not include treatment for :

- Vasicek bond price model

- Ito’s Lemma

- Derivation of the Black Scholes equation

- Theoretical background around the many theorems that build the foundation for Black Scholes Analysis

SOA MFE / CAS 3F Exam Prep – Interest Rate models

SOA MFE/ CAS 3F: Cox-Ingersoll-Ross interest rate model

We discuss the simplest of interest rate models, the Cox Ingersoll Ross interest rate simulator and review the model as well as the steps required in its calibration.

Interest Rate Simulation & Forecasting: Using CIR (Cox Ingersoll Ross) Model: Introduction

SOA MFE/ CAS 3F: Black-Derman-Toy interest rate model

A slightly different application is used to illustrate the construction and calibration of the one factor no arbitrage Black, Derman and Toy (BDT) model

Interest Rate Simulation Models: Black, Derman and Toy (BDT): Building BDT in Excel: Introduction

Interest Rate Simulation Models: Building Black, Derman and Toy (BDT) in Excel: Define Output Cells

SOA MFE / CAS 3F Exam Prep- Valuation of derivative securities

SOA MFE/ CAS 3F: Derivative Products

The following courses provided a detailed introduction to Options and Derivatives/ Options pricing. This material includes discussions on the put call parity , Black-Scholes option pricing model, Greeks, Exotics, etc.

Options Crash Course for dummies

Options & Derivatives Products

Advance Options & Derivatives Crash course

SOA MFE/ CAS 3F: Calculate the value of European and American options using the binomial model.

This course focuses on an alternative method of implementing a two-dimensional binomial tree compared to the traditional method of building a binomial tree in excel presented in most option pricing textbooks. The alternate approach is based on the techniques documented by Professor Mark Broadie at Columbia Business School as part of his coursework in Security Pricing and Computational Finance courses at Columbia University and allows us to extend a simple 3 step tree to a 50 – 100 step option pricing tree in a few minutes.

The course starts with pricing European calls and put options, followed by pricing American options and closes by reviewing option pricing for Knock out and Knock in (Sudden Death). We also review the special case of a down and in option.

Options pricing – Using binomial trees to price options in a spreadsheet

Options Pricing – Pricing Call Options – Option pricing spreadsheet – Binomial trees

Options Pricing – Pricing Put Options – Option pricing spreadsheet – Binomial trees

Options pricing–Exotics Options–Pricing a Capped Call–Excel implementation – Binomial trees

Options pricing – Pricing Knockout exotic options – Sudden Death Options – Down and out call options

Options Pricing – Binomial Trees – Pricing Sudden death Options – Down and in call options

Option Pricing – Black Scholes – Probabilities Explained: Understanding N(d1) vs N(d2)

SOA MFE/ CAS 3F: Interpret option Greeks & Delta Hedging.

Delta Hedging – Dynamic Hedging – Option Greeks Guide

The understanding option Greeks reference resource for dummies

Understanding Greeks – Introduction

Understanding Greeks – Analyzing Delta & Gamma

Understanding Greeks – The Guide to delta hedging using Monte Carlo Simulation

Delta Hedging – Cash PnL Simulation – Excel Spreadsheet walkthrough

Understanding Greeks – The Delta Hedging Simulation extended for Put Options

Understanding Greeks – Quick Reference Guide to Delta, Gamma, Vega, Theta & Rho

Monte Carlo Simulation SOA MFE/ CAS 3F: Simulate lognormal stock prices.

Extending MC simulation for currencies and commodities

Computational Finance: Linking Monte Carlo Simulation, Binomial Trees and Black Scholes Equation

SOA MFE/ CAS 3F: Use variance reduction techniques to accelerate convergence

Monte Carlo Simulation: Convergence and Variance reduction techniques for option pricing models

Risk Management Technique MFE/ 3F: Control risk using Delta-hedging

Dynamic Delta Hedging for European Call Options

Dynamic Delta Hedging – Extending the Monte Carlo simulation model to Put contracts

SOA MFE/ CAS 3F Exam Prep Related Paid Materials

Visit our Finance Course store to purchase pdf versions of these and other courses as well as video courses and detailed EXCEL examples as mentioned below:

SOA MFE / CAS 3F: Solved EXCEL Examples and Solutions (Paid for courses)

- SOA MFE / CAS 3F Related Excel & PDF section of the store

- Delta Hedging – Dynamic Hedging – Option Greeks Guide

- Black Derman Toy Model Construction – EXCEL Example

- How to utilize results of a Black Derman Toy Model – EXCEL Example

- Derivative Pricing – Binomial Trees EXCEL Example

- Calibration of CIR Model – EXCEL Example

- Cox-Ingersoll-Ross (CIR) Interest Rate model – EXCEL example

- Monte Carlo Simulation – Equity – Example

- Monte Carlo Simulation – Commodity – Example

- Monte Carlo Simulation – Currency – Example

- Monte Carlo Simulation – Variance Reduction Procedures – EXCEL Examples

- Valuing Options – Binomial Tree – Traditional Approach – EXCEL Example

- Valuing Options – Black Scholes Example

SOA MFE/ CAS 3F: Video Courses (Paid for courses with free samples)

- Understanding N(d1) and N(d2)

- Derivative Products

- Derivatives Terminology Crash Course

- How to construct a Black Derman Toy Model in EXCEL

- How to utilize results of a Black Derman Toy Model

SOA MFE/ CAS 3F: PDF courses (Paid for courses – easy to read pdf versions of online course materials)

Interest Rate Simulation Crash Course

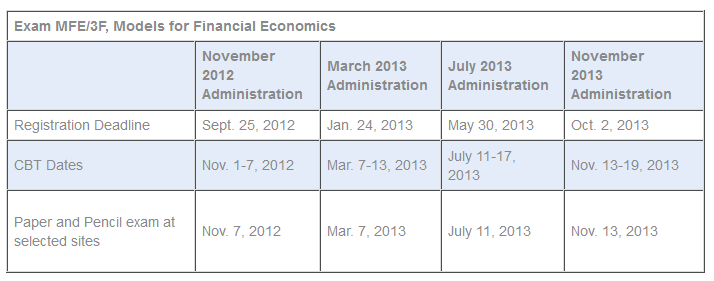

SOA MFE Exam Schedule

Understanding Delta Hedging & Greeks – Technical Interview Guide

Till November 30th, take $60 off the cover price when you order your electronic copy. The package includes a 71 page study guide and 3 supplementary Excel Spreadsheets that focus on Monte Carlo Simulation of Dynamic Delta Hedging, Calculation of Cash PnL & Dissection of Option Price Sensitivities (Greeks).

Learn more about the title through the Delta Hedging & Greeks Book launch post.

Comments are closed.