In preparation for Basel III and the requirements for banks to hold higher (and better quality) minimum amounts of tier-1 capital, various responses/ reactions to the regulatory regime changes are being witnessed in different countries.

Here is a quick summary of significant changes and comparisons as of November 2014.

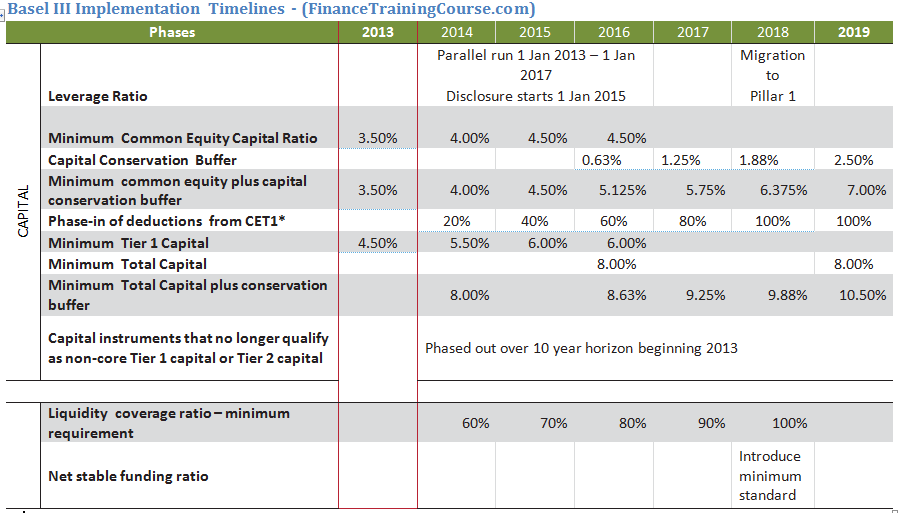

Basel III – Implementation Timelines

i. Convertible Preferred Shares

Issuing new equity is an expensive source of capital for an entity. According to the Australian Prudential regulation authority, banks and insurance companies have devised a way to increase funding that qualifies as equity but at a lower cost of capital than equity. Convertible Preferred Shares (CPS) pays an interest rate which tracks the price of debt instruments and is converted to ordinary shares after a set period of time.

However, in order for the CPS to qualify as Residual Tier 1 capital they must have the following characteristics:

- Non-cumulative dividends- i.e. if not paid at designated time then they will not be paid in the future

- Dividend payments are based on the entity’s discretion and whether or not the issuing entity passes a profitability test and a minimum capital requirements test.

- Will convert forcibly to ordinary shares in the event that the entity needs to raise capital when a non-viability trigger event occurs. This will usually happen when the entity’s share price is depressed leading to large losses for the investor.

Analysts believe that this exposes CPS investors to risk (pricing risk because on conversion converts to ordinary shares not cash) for which they are inadequately compensated. They feel that a position in a CPS is at least as risky as purchasing ordinary shares of the company but investors will receive a return less than the return on equity.

These shares tend to rank just above ordinary shares where in the event of a winding up of the company the investors would be paid after subordinated unsecured note-holders and preferred and secured debtors have been paid but before ordinary shareholders.

ii. More expensive hedge fund trading strategies

In the US the impact of the BASEL III regulatory changes will most probably lead to an increased cost of trading. Brokerages have already stated that they will pass any increase in their costs due to the implementation of Basel III rules through to their hedge fund clients in the form of higher trading and financing costs. These are likely to increase the cost for plain vanilla strategies such as trading equities (which are fairly liquid) as well as for more complex strategies that trade relatively illiquid securities such as mortgage backed securities. It is also feared that the latter may be priced to such an extent that it could reverse any recovery in MBS markets and subsequently also hamper the recovery in the property markets.

The fear is that these new liquidity and capital requirements would by increasing the cost of trading further hamper and slow trading which could exacerbate the liquidity situation of the market. Hard to value niche global markets could shut down as they become more and more expensive to finance in the market.

iii. Increased pace of infrastructure funds trades

In the UK, banks and insurance companies have been reducing their investments in infrastructure because under the regulatory capital changes of Basel III and Solvency II, these investments will be more expensive to maintain on their books requiring a higher level of minimum regulatory capital.

The increased supply in the market of these investments has been absorbed by Pension funds who have a need for long term inflation protected return assets, as well as asset managers who have clients with long term liabilities (such as insurance companies who will be able to bear the higher cost of holding such assets), large fund of funds, private equity funds, etc. So much so that the demand for direct investment in infrastructure is on the rise.

The rate at which these infrastructure funds transactions are occurring is beyond what is usually witnessed in these normally highly illiquid markets. Recent sales have cumulatively exceeded over 300 million pounds with more such transactions in the pipeline.

iv. Divestment of financial institution shares

The Basel III changes to the capital rules discourage banks and financial institutions from holding large investments in other banks/ financial institutions. As a result we have recently witnessed Citigroup cut its investments in the Turkish bank, Akbank from 20% to 10%.

v. Increased repo volume and Shadow banking risk

Stricter bank regulation without accompanying regulation for market-based financing could increase the volume of trades, particular high risk activity, in the repo market and hence encourage a greater involvement of the shadow banking sector (structured investment vehicles, money market mutual funds, hedge funds) in these market, usually the lenders in these repo deals.

This would be the result of banks being assessed higher capital charges for holding or trading riskier securities. On the other hand as it currently stands, the shadow banking industry would not be impacted by these regulatory regime changes. There would be an incentive therefore to shift higher risk (and hence higher reward) trading activity from the banking sector to the not as strictly regulated shadow banking sector thus defeating the purpose of regulators to discourage excessive risk taking in the financial sector.

Analysts fear that a great involvement of the shadow banks in these high risk markets could lead to a potential increase in liquidity risk as witnessed during the US credit crisis. In the crisis repo markets played their part in the increased price volatility seen for illiquid assets and securities which were no longer eligible to be posted as collateral as well as the funding problems of dealers with reduced access to the market.

vi. Other changes

Expected Positive Exposure will address general Wrong-Way Risk and counter party credit risk.

Financial institutions will complete trade captures for all counter party credit risk for stress testing.

Introduction of multiplier for Asset Value Correlation.

Additional capital for illiquid exposures.

100% risk weight for Trade finance.

Additional Reporting requirements

- Report on contractual maturity mismatch

- Report on funding sources & concentration

- Available liquid assets

- Market-related monitoring tools

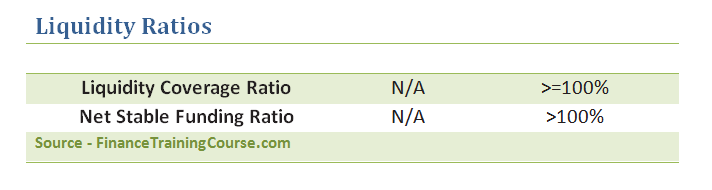

- Liquidity Coverage Ratio by currency

- Results of stress tests should be integrated into regular reporting to senior management

- Lower reliance on External Rating Agencies

References:

- IAG’s CPS: Rotten tomatoes with Basel (Nathan Bell – March 26, 2012)

- Investors have issues with hybrid shares (Eric Johnston – March 28,2012)

- Hedge funds face higher trading costs (Sam Jones – March 26, 2012)

- Demand for infrastructure takes off (Kiel Porter and Mark Cobley – March 26, 2012)

- Akbank says Citi’s stake trim driven by Basel III (Simon Cameron-Moore- March 24, 2012)

- Basel III Measures May Heighten Repo Volume, Risks, Fitch (Liz Capo McCormick – March 19, 2012)