Dubai Islamic Bank’s (DIB) acquisition of Tamweel PJSC serves as our second case study for the upcoming Bank valuation course. The case study serves as a basis for discussion for the acquisition of a single product business line under distressed conditions and market uncertainty.

A new business model for mortgage lending in the Middle East.

Tamweel’s original investment thesis was based on a simple question. Within the UAE market, could a dedicated mortgage lender focused on linking international capital markets with demand for Dubai real estate, function and succeed? In play was the opportunity represented by the red hot residential real estate prices and the Dubai success story. On the investor front there was a great deal of demand for publicly traded long dated sharia compliant debt instruments. The demand arose within the Islamic finance world, especially Islamic insurers, as they wrote long term liabilities and invested the proceeds into short term assets. Tamweel planned on exploring that connection by linking the two opportunities as quickly as possible.

To improve odds of success, Tamweel started off with higher capitalization geared to generate higher credit ratings. Tamweel’s primary sponsors included one of the oldest brands in the Islamic finance world and a tested team of retail banking professionals. They hit the securitization and sukuk markets with two issues within the first two years of launching operations. By 2007 Tamweel had already tapped Sukuk markets for USD 560 million by using securitization as a means of financing.

By the time 2008 arrived, Tamweel was writing between AED 500 – 700 million of business every month. There were some concerns about the overheating of residential real estate in Dubai but there was no shortage of either liquidity or buyers. On the back of rising oil prices and increasing political instability elsewhere in the region, in January 2008, Dubai and Tawmeel both looked set to rise.

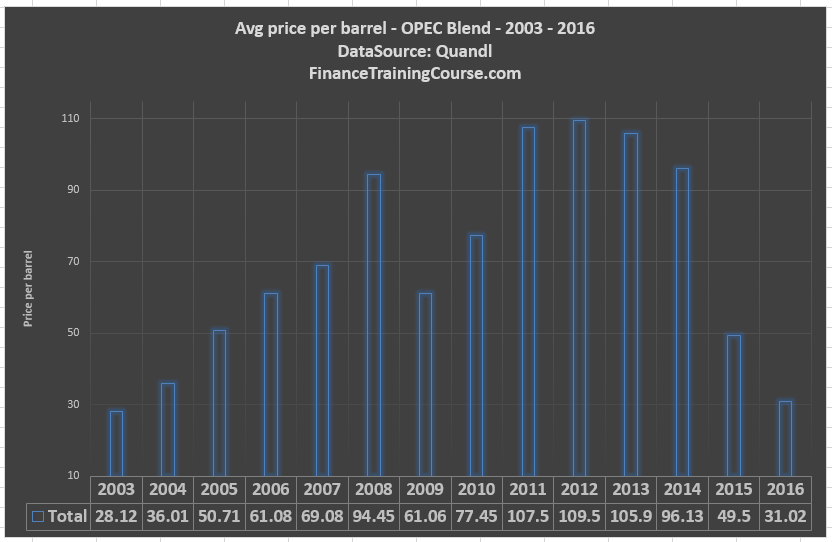

All that changed with the collapse of Bear Stearns and its eventual acquisition by J P Morgan Chase in March 2008. While there were plenty of warning signs leading up to the summer of 2008, all was still well with oil markets. Prices for OPEC blend, the average price charged per barrel by OPEC members, were flirting with USD 140 per barrel barrier in July after maintaining a yearlong bullish streak. If prices maintained that trend, there wouldn’t be any shortage of regional liquidity.

DIB Tamweel case study. Dark clouds on the horizon.

The first sign of real trouble arrived with the tepid response noted at the much promoted, Dubai focused, annual real estate event in July 2008. While a number of new high profile projects where announced, buyers were missing. By the time August rolled in, regional lenders were moving into defensive postures and there signs of trouble on the horizon for the real estate market.

On 19th August the salvo of bad news arrived triggering what would later be known as the global financial crisis. Lehman Brothers’ stock fell by 13% on earnings related news and stayed in free fall till the eventual failure of the bank on 10th September 2008. The liquidity pressure wave created by Lehman’s collapse made its way around the globe.

The two years that followed were the hardest in Tamweel’s history. Without a book of stable retail deposits, it was at the mercy of wholesale lenders. Given what was happening with the rest of the world, especially with mortgages and real estate, with counterparty exposures and with securitization tranches, that source of funding dried up overnight for all borrowers, not just Tamweel. While Tamweel wasn’t alone in its suffering, one significant fact was abundantly clear. Financial markets were giving a clear signal. The model of borrowing whole sale and lending retail was no longer viable business. By the time the dust would settle, something would have to give.

In the first few months after the crisis, the focus was on survival. The hope was that once the wave passed and markets normalized Dubai would be open for business again. But by 2010 when that hope didn’t materialize, the primary solution on the table was a merger or an acquisition. There were a number of potential options. A merger of equals or an acquisition by a much larger player? A merger equal wouldn’t solve the liquidity issue. It would only create a significantly bigger mess and a potentially larger hole in the ground.

The question being asked internally as well as by buyers was how to value an entity perceived as distressed in distressed markets? The chosen model would depend on who the buyer was and what they planned to do with Tamweel post-acquisition? A second choice was to do a partial sale of the mortgage book, splitting the exposure in the evergreen good bank – bad bank configuration. But the most important question dealt with the business model. Was there a scenario where Tamweel or Tamweel’s buyer would be able to go back and tap securitization markets in the future?

Timeline of Tamweel acquisition by Dubai Islamic Bank (DIB)

March 2004: Tamweel is established by Dubai Islamic Bank and another Dubai based entity.

Tamweel quickly becomes a leading provider of mortgages in the UAE financing property worth over AED 10 billion between 2004 and 2008.

May 2005: The Emirates National Securitisation Corporation issues a US$350 million rated securitisation of domestic mortgages originated by Tamweel PJSC (Tamweel) in Shari’a compliant manner.

3rd June 2006: Tamweel is registered as a Public Joint Stock Company as a result of an Initial Public Offering (IPO). The IPO is subscribed 485 times in excess of the required amount.

September 2006: Tamweel posts a Dh798 million profit for the first nine months of 2006:

Source: http://www.gulfbase.com/quarterly-financial-charts-tamweel-co-tamweel-559-15-186

2007: Tamweel, through Tamweel Residential ABS CI(1) Ltd, issues US$210 million asset-backed certificates, the first true sale securitisation in both the UAE and the GCC region as a whole.

2008: Tamweel lends between AED 500 – 700 million a month to build its retail book.

November 2008: Market value of shares fall by 85%. Tamweel side-lines it loan origination business in light of the financial crisis.

November 2008 – September 2010: Conversations underway for a merger of Amlak Finance, Tamweel under the umbrella of Abu Dhabi’s state owned Real Estate Bank. Trading in Tamweel shares are halted on the Dubai Financial Market.

September 2010: DIB acquires a majority stake in Tamweel by buying out stakes of other large institutional stakeholders (Dubai World’s Istithmar, Dubai Investment Group and Dubai Holding’s Dubai Capital Group, and others). Its stake increases from 20% [21%] to 57.33% [58.2%].

There were speculations that the buy-out would be at a discount to Tamweel’s book value (or to the last traded price of Dh. 0.99 on 20 November 2008)[1] based on severe stress to its mortgage book on account of significantly reduced property prices (30% -40%) as compared to 2008 prices. However, Dubai Islamic Bank paid 374.7 million dirhams ($102 million), or 1 dirham a share, in cash and stock to raise its ownership.[2] Dubai Islamic paid 318.6 million dirhams in cash and 56.1 million dirhams in treasury shares for the stake.[3]

November 2010: With funding from DIB (DIB is putting in Dh100 million every month to finance home purchases), Tamweel resumes its loan origination business offering mortgages up to 80 percent of property values.

10th November 2010: Wasim Saifi, the chief executive of Tamweel resigns as shareholders vote to install a new board of directors dominated by Dubai Islamic Bank (DIB) executives

31st December 2010: Full consolidation of Tamweel on DIB’s financial statements. DIB’s retail financing base grows by a third because of the inclusion of Tamweel’s mortgages.

31 Mar 2011: Tamweel’s shares acquired by DIB are revalued to AED 2.7 per share after a valuation of the company, a fair value gain of 637 million since the acquisition.

May 2011: Tamweel shares resume trading on the Dubai Financial Market. Share values fall by 10%.

January 2012: Tamweel raises AED 1.1 billion from the sale of sukuks (5.154 percent bonds due January 2017 fully guaranteed by DIB), in its first offering since 2008.

July 2012: Tamweel’s 2nd quarter profits are down by 33% compared to the prior year period. The company postpones a $235 million asset-backed securitisation following a lukewarm response from potential investors. These certificates were due to mature in 2046 and were callable in July 2017.

December 2012: U.A.E. central bank’s decides to cap mortgages for foreigners and nationals at 50 percent and 70 percent of the property values.

3 January 2013 – 16 March 2013: DIB announces a tender offer to acquire the outstanding shares of Tamweel in a share swap at the rate of 10 new DIB shares to 18 existing Tamweel shares held. The fair value of Dubai Islamic and Tamweel shares was set at 2.25 dirhams and 1.25 dirhams, respectively.

March 2013: DIB acquires 86.47% of Tamweel shares.

7th July 2013: Approval from Tamweel’s shareholders to convert the company to a Private Stock Company and delist its shares from the Dubai Financial Market, subject to regulatory approval.

17th September 2013: DIB settles all bilateral liabilities of Tamweel, amounting to over AED 4 billion, two years ahead of scheduled maturity. These outstanding obligations consisted of liabilities that were part of a five-year moratorium agreed with creditors in 2010, which were set to mature in October 2015. Early repayment was possible in the light of healthy capitalization and sufficient liquidity.

26th September 2013: Approval by the Securities and Commodities authority to suspend trading of Tamweel’s shares on the Dubai Financial Market from 1st October 2013.

27th August 2014: The company is registered as a Private Stock Company.

18th December 2014: The shares of the company are delisted from the Dubai Financial Market.

31st December 2014: Tamweel’s last available balance sheet.

April 2015: Dubai Islamic Bank makes an offer to purchase the remaining 13.5% shares to acquire the remaining stake in the company. The offer, open for a month till April 30, is for AED 1.25 per share. This would be worth 146.3 million as there are currently 864.99 million Tamweel shares in circulation. The largest remaining shareholders are Amundi Funds Equity Mena and Deka Middle East & Africa.[4]

Questions for Tamweel PJSC – Case A, Case B

Take a look at the attached Tamweel financial extract in Excel, Tamweel Case B and the Bank Valuation study note.

- Given the approaches shared in the Bank Valuation study note, which valuation model would you recommend for valuing Tamweel in September 2010? What adjustment would you make to that model?

- What is the range of valuation you would recommend to your client? How would this range change if the client was Tamweel? If the client was the buyer?

Reference and Footnotes

[1] http://mec.biz/term/uploads/DIB-01-03-2010.pdf

[2] http://www.bloomberg.com/news/articles/2011-05-10/tamweel-plunges-10-on-first-trading-day-since-november-2008-2-

[3] http://www.bloomberg.com/news/articles/2011-04-03/dubai-islamic-bank-paid-102-million-to-buy-controlling-stake-in-tamweel

[4] http://www.thenational.ae/business/banking/dubai-islamic-bank-in-offer-for-remaining-135-stake-in-tamweel