Corporations use FAS 157 Term B syndicated loan as a source of funding for capital purposes. The loans usually are subject to a number of covenants such as

- performance criteria e.g. maintenance of minimum coverage ratios,

- restrictions on the distribution of profits and taking on additional indebtedness, etc.

We price loans with reference to one or more reference rates (e.g. US LIBOR, Federal Funds Effective Rates, prime rates of the administering bank in the syndicate) and applicable margins. Besides the amortization schedules for repayment of the principal loan amounts, entities may also need to make mandatory prepayments. These are based on their performance or may be voluntary prepayments, subject to the payment of penalty fees.

Term B Loans are subject to the risk of default of the borrower.

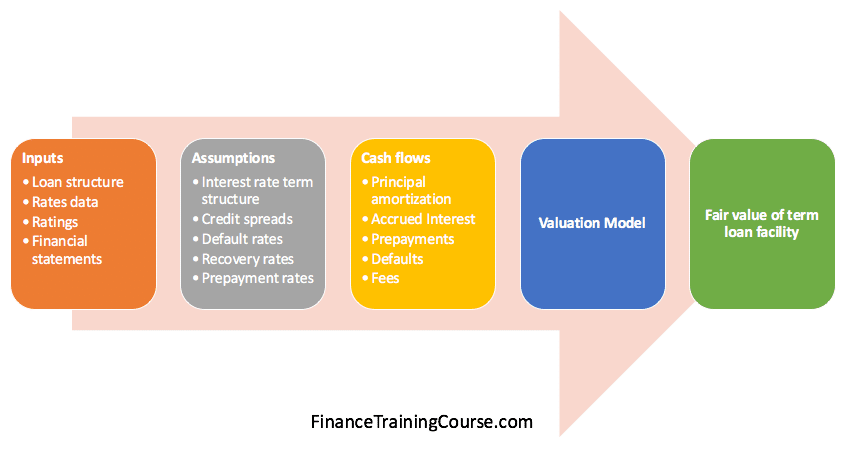

1. Inputs to value FAS 157 Term B loans

Loan structure

The credit agreement will contain:

- details of the aggregate credit amount,

- start and maturity dates,

- types of loans offered (e.g. base rate or Eurodollar rate loans),

- the frequency of interest payments,

- fees payable if any,

- applicable margins applied to variable interest rates, etc.

Rates data

Use a risk free term structure, such as the US Treasury Daily yield rates both for determining discount rates and for calculating future cash flows.

Also, obtain the historical series for the other reference rates mentioned in the agreement. Data may be available from a number of public domain sources or obtain the same from the client. This data will provide an estimate of the average spread of these rates over the US Treasury rates.

Market yield and credit spread information on loans or bonds of similar credit standing would also be of use.

Ratings

Recent ratings action reports by eligible ratings agencies (e.g. Moody’s, S&P, A.M. Best, NAIC) will inform of the current level of creditworthiness of the company as well as its debt. Also obtain Information on loss severities (LGDs) and/ or recovery rates, default rates, transitions and credit migrations, if available.

Financial statements

Certain loan structures may link the applicable margins or fees to performance or leverage ratios of the company. We require financial statements to calculate these ratios. These statements may be publicly available or you may obtain them from the borrowing entity.

2. Assumptions

Interest rate term structure

As mentioned above the risk free term structure is obtained to determine the discounted rates used for the present valuing future cash flows. Bootstrap the par term structure to obtain zero coupon and forward rates as of the valuation date. Use the rates as is and/or as inputs to an interest rates model to obtain short rates (BDT) or forward rates (HJM) for future time steps.

Under Method 2 of the expected present value valuation technique which is the approach we will be focusing on in this post, use zero coupon rates with the assumed credit spread to discount future cash flows.

Use the forward rates determined with appropriate spreads over the risk free rate and applicable margins to project future cash flows.

Credit Spreads

The credit spread represents what the market expects for the additional risk of the loan over the risk free instruments. In other words, it is the systemic risk associated with the loan. Market yield data for loans or bonds of similar credit rating will give an estimate of the credit spread as of the valuation date. We may make an assumption that the spread will remain constant over the life of the loan. An implication that the underlying credit worthiness of the company and/or indebtedness will remain unchanged. This may be a simplistic assumption. However, depending on the time constraints and resources available, we may enhance it by modelling future defaults and associated spreads.

Default rates

Assess default rates from data gathered on the most recent rating action as of the valuation date. Once again, we may assume the default rate remains static over the life of the loan. Or, we may model it depending on the resources and time available. The modelling could project future rating transitions and migrations over the remaining life of the loan based on historical transition data available for similar instruments. We may fit the model to actual default data of similar companies or issues . As a result we can account for idiosyncratic or firm specific risk in the default probabilities together with market or systemic default rates and probabilities published in studies by rating agencies and other institutions. Also, we may assume that default rates vary by the residual time left till maturity.

In line with the projected migrations, credit spreads may also be varied accordingly.

Recovery rates

Obtain data for recovery rates from market sources. For example, in addition to assigned lettered grades, Moody’s Investor Services also assesses LGD ratings to individual loan, bond, and preferred stock issues and firm-wide or enterprise expected LGD rate. Recent research studies on loss severities and recoveries in the event of default for the relevant market may also be useful sources of information.

Prepayment rates

We make a static flat prepayment rate assumption based on management’s assumptions of the same. Alternatively, mandatory prepayments may require a projection of the company’s performance, e.g. excess free cash flows, for each year (or reporting period) over the remaining life of the loan. This would require a projection of the company’s balance sheet and income statement based on a number of company-specific as well as economic factors.

The complexity of this process countered by the limitations on time and resources may suggest a more generalized approach. One that approximates the overall absolute prepayment rate that takes into account both mandatory and voluntary prepayments. In general, prepayments will occur when the company’s situation improves, making it more likely that it will have cheaper funding sources available to it in the market.

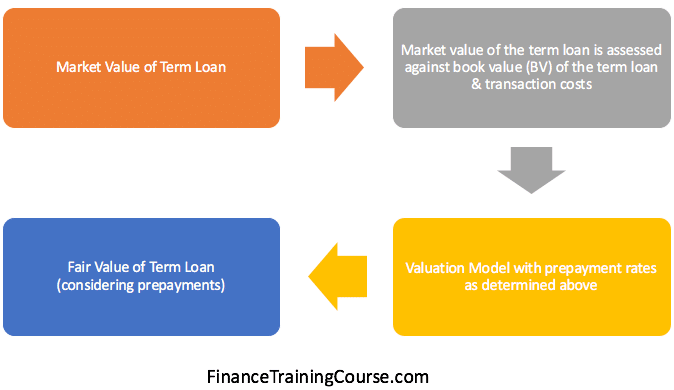

One way of modelling prepayments, therefore, is to assess the market value of the loan against the outstanding loan balance, the prepayment penalty and the refinancing and origination costs of taking out a new loan. If the former exceeds the sum of the latter, we assume a prepayment will occur as the new loan value will be sufficient to pay of the existing loan, otherwise there will be no prepayment. Costs mentioned here may be implied from the difference between observed market prices (option adjusted spreads) of loans and bonds of similar creditworthiness. The series of charts below illustrates an example of a prepayment modelling process.

Modelling prepayments walk through

In the first stage, bootstrap the risk free rates to obtain zero coupon rates and forward rate term structures. Carry out a principal component analysis (PCA) on the forward rates term structure to determine factors that best explain the volatility of the structure. Use these factors (which we scale so that they calibrate to the volatility of the term structure as of the valuation date) and the zero coupon rates in a Heath Jarrow Merton (HJM) interest rate model to determine forward rate term structures for the current period as well as for each time step going forward. Based on the derived future forward rate term structures, projected zero rate term structures are also calculated.

Next, plug the estimated forward rates and zero rate term structures into the valuation model with the cash flow structure of the term loan and other assumptions on default and loss severities. At this stage, the valuation model assumes a prepayment rate of 0%. Determine future market values of the loan for each time step going forward including the valuation date and each amortization/ interest payment date.

At each time step, assess the future market value against the sum of the outstanding loan balance (book value) and the costs mentioned above. If the Market value exceeds the Book value + costs assume a 100% prepayment rate. If the Market value is less than the Book value + costs, assume a 0% prepayment rate. The higher the transaction costs, all other factors remaining constant, the less likely there will be a prepayment. Then use the prepayment rates (the first instance of prepayment is sufficient as the prepayment rate is 100%) are in the valuation model and the resulting value derived from the model is the fair value of the term loan considering prepayments.

3. Cash flows for FAS 157 Term B syndicated loans

FAS 157 term B loan cash flows include repayment of principal amount and interest accrued. Principal amount may be payable in full at maturity or amortized over the life of the loan. If amortized, the schedule or repayment structure is defined in the credit agreement. Accrued interest on the outstanding principal balance is due at the end of the interest payment period.

While the principal amortizations are pre-determined based on the loan agreement, the accrued interest, particularly if the loan is a variable interest rate loan, depends on a number of factors. Including the assumed risk free forward rate term structure, average spread of the reference rate over the risk free rate, and applicable margin as defined in the loan agreement.

If defaults and prepayments did not occur the cash flows would be limited to these amounts, plus any costs payable to the lender. However, defaults and prepayments add a degree of complexity to the model. Account for them in the calculation of fair value because the FAS 157 standard specifically states that fair value should reflect the risk of the liability.

The amount and timing of cash flows are important elements in any valuation exercise. Defaults and prepayments effect the contractual flow of the instrument and introduce uncertainty into the mix. Therefore in addition to default and prepayment rates, we make assumptions as to the timing and amount of these contingent cash flows.

For example, we may assume defaults occur at the end of the period, consisting of a repayment of the full outstanding loan balance and accrued interest, adjusted for the proportion that will remain unrecovered because of the default event. Also, we may assume that prepayments occur at the beginning of an interest period, for the full outstanding loan balance plus the prepayment penalty, if any.

4. Valuation Model for a FAS 157 Term B syndicated loan

The valuation model for the FAS 157 Term B syndicated Loan is primarily a two-step model. First project the cash flows for each future time step, including the valuation date and the maturity date of the loan. Then discount the cash flows to derive a single value on the valuation date. The discount factor considers not only the time value of money, i.e. interest (zero coupon rate plus credit spread) but also the probabilities of default and prepayment.

5. Results & Stress Testing

The calculated results are fair values measured with significant unobservable Level 3 inputs as of the valuation date. Stress and sensitivity test the results for the major assumptions. The ones we use in the model include the interest rate, credit spread, default rates, prepayment rates, transaction costs, etc.

References

- Building a credit risk valuation framework for loan instruments – Scott Aguais, Larry Forest and Dan Rosen – Algo Research Quarterly, Vol. 3, No. 3, December 2000, pp. 21–46.

- Statement of financial accounting standards No. 157 – Fair Value measurements – FASB – 2010

- Credit exposure and valuation of revolving credit lines – Robert A Jones & Yan Wendy Wu – 19 July 2009

- Questions you should be asking about Senior Secured Loans – Joe Lemanowicz – May 2011

- A one-parameter representation of credit risk and transition matrices – CreditMetrics Monitor Third Quarter 1998 (pp.46 -58)

- Ratings symbols and definitions – Moody’s Investor services – May 2016