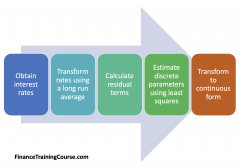

CIR Model Parameter Estimation

2 mins read In this post, we explore CIR Model parameter estimation. In other words, we consider how to calibrate the Cox Ingersoll

2 mins read In this post, we explore CIR Model parameter estimation. In other words, we consider how to calibrate the Cox Ingersoll

2 mins read We review the one-factor equilibrium Cox Ingersoll Ross (CIR) model and its primary features. The short-term interest rate is one of the

2 mins read In the second stage of the construction of the Black-Derman-Toy (BDT) one factor interest rate model in EXCEL we will

2 mins read This is the first of seven posts where we will be considering the step- by- step process of building the

2 mins read The Black Derman Toy model Excel implementation guide. A one factor interest rate model and some simplifying assumptions made in its

2 mins read Duration is a measure of how rapidly the prices of interest sensitive securities change as the rate of interest changes (see application example in the ALM section). For example, if the duration of a security works out to 2 this means that for a 1% increase in interest rates the price of the instrument will decrease by 2%. Similarly, if the interest rates were to decrease by 1% the price of the security would increase by 2%.