ALM Modeling – Assumptions, Conventions & Hacks

5 mins read ALM Banking models – Assumptions review In a recent class on Asset Liability Management Models, my MBA students asked a

5 mins read ALM Banking models – Assumptions review In a recent class on Asset Liability Management Models, my MBA students asked a

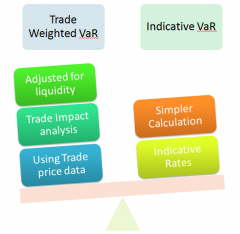

5 mins read Imagine a board meeting. You have just presented your Value at Risk (VaR) analysis and a board member asks a

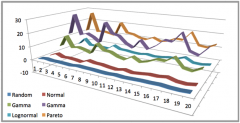

3 mins read Since we have a model for simulating oil prices, we are now ready to link our oil price model to

3 mins read How do you manage liquidity risk for a fixed income portfolio. How do you stress test liquidity risk for the

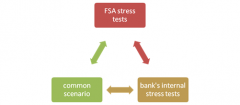

9 mins read A short review of stress testing regulatory frameworks. Stress testing is evaluating the impact of large, expected as well as

5 mins read Stress testing refers to a process through we which we try and assess the impact of abnormal and extreme conditions on our processes, control systems and organizations.

Within financial services stress testing takes a second dimension where the focus shifts from assessing impact to identifying breaking points; the maximum amount of stress a financial institution would be able to bear before it breaks down and fails. The level of interconnectivity between financial markets and institutions has made this threshold of failure even more important since a since the failure of a single institution can trigger a deep and painful system wide crisis that can very easily turn into a regional or global contagion.