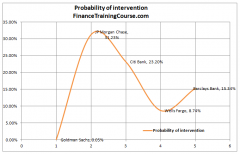

Calculating economic capital – Using volatility

4 mins read In our first method presented earlier for calculating economic capital we used the historical worst case shift. In method two

4 mins read In our first method presented earlier for calculating economic capital we used the historical worst case shift. In method two

4 mins read Our alternate model for calculating Economic Capital comes in multiple variations. We do a detailed presentation for Method One, followed

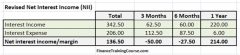

6 mins read The two elements used within bank ALM analysis are Economic Value (EVE) and earnings as given by Net Interest Income

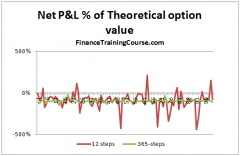

3 mins read A simple case study Theoretically speaking in the Black Scholes world the cost of the hedge should be close to

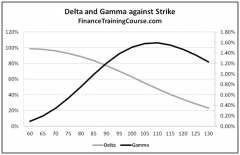

6 mins read We use a simple example to illustrate the calculation of Shadow Gamma as describe by Taleb in Dynamic Hedging. Gamma

2 mins read We build a simple Excel spreadsheet that allows us to hedge Gamma and Vega exposure for a single short position