Variance Reduction: Quasi Monte Carlo & Antithetic technique

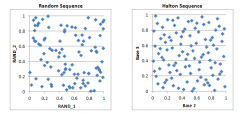

5 mins read Speeding up convergence. Using Quasi Monte Carlo & Antithetic techniques In the past we have looked at Monte Carlo Simulation:

5 mins read Speeding up convergence. Using Quasi Monte Carlo & Antithetic techniques In the past we have looked at Monte Carlo Simulation:

3 mins read Ladder options are options where the strike is reset whenever the price of the underlying asset reaches certain trigger levels

2 mins read a. Value of a long forward contract (continuous) The value of a long forward contract with no known income and

2 mins read We are valuing an FRA for someone who is receiving fixed interest rate payments and who is paying floating interest

< 1 min read a. Forward Price of a security with no income Forward Price of a security with no income is given by

2 mins read In our Derivatives Crash Course for Dummies, Master Class: Options and Derivatives Crash Course: Session Five: Synthetics we had discussed