Conditional Value at Risk (CVaR)

5 mins read Imagine a board meeting. You have just presented your Value at Risk (VaR) analysis and a board member asks a

5 mins read Imagine a board meeting. You have just presented your Value at Risk (VaR) analysis and a board member asks a

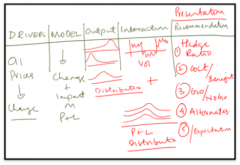

3 mins read Since we have a model for simulating oil prices, we are now ready to link our oil price model to

4 mins read While we have shared a great deal about Simulation Modeling and Analysis on this blog, over the years, I felt

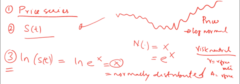

5 mins read My love affair with Monte Carlo Simulation Let’s start with the honest truth. I had a torrid long distance love

4 mins read Of all the intimidating equations and formulas (PDE’s and otherwise) out there, the derivation of the Black Scholes Model formula

2 mins read Option Greeks. Dissecting Delta, Gamma, Vega, Theta & Rho It doesn’t matter if you took the FRM, CFA, PRMIA, CERA,