The Option Pricing models 5 nights crash course

2 mins read I am often asked if there is a suggested sequence that I would recommend to finance newbie(s) when it comes

2 mins read I am often asked if there is a suggested sequence that I would recommend to finance newbie(s) when it comes

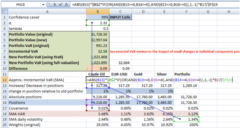

8 mins read Have you ever wondered what Value at Risk (VaR) numbers would look like across the same dataset but using the

< 1 min read Value at Risk Models – Value at Risk, Marginal VaR, Incremental VaR & Conditional VaR Our latest addition to our

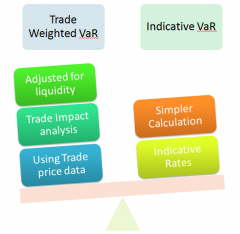

3 mins read How do you manage liquidity risk for a fixed income portfolio. How do you stress test liquidity risk for the

5 mins read Rebalancing frequency, Implied Volatility & Rho. Dynamic Delta Hedging Applications. Now that we have a Delta Hedging Model for Calls

< 1 min read If you have been playing the odds game mentally for the US Presidential election and want a resource to take