Simulation tools. Variance reduction techniques for option pricing models

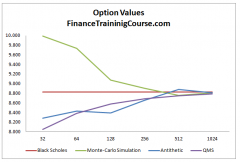

4 mins read Variance Reduction tools for Monte Carlo Simulation. Monte Carlo simulation techniques are a useful tool in finance for pricing options

4 mins read Variance Reduction tools for Monte Carlo Simulation. Monte Carlo simulation techniques are a useful tool in finance for pricing options

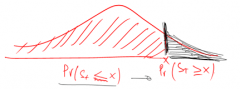

3 mins read On the other hand N(d1) will always be greater than N(d2) because in linking it with the contingent receipt of stock in the Black Scholes equation, N(d1) must not only account for the probability of exercise as given by N(d2) but must also account for the fact that exercise or rather receipt of stock on exercise is dependent on future value