Earnings at Risk – Asset Liability Management reporting

5 mins read Calculating EAR Earnings-at-Risk (EAR) is computed in order to evaluate the impact of interest rate change on earnings. The approach

5 mins read Calculating EAR Earnings-at-Risk (EAR) is computed in order to evaluate the impact of interest rate change on earnings. The approach

2 mins read Duration is a measure of how rapidly the prices of interest sensitive securities change as the rate of interest changes (see application example in the ALM section). For example, if the duration of a security works out to 2 this means that for a 1% increase in interest rates the price of the instrument will decrease by 2%. Similarly, if the interest rates were to decrease by 1% the price of the security would increase by 2%.

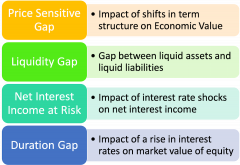

6 mins read This section reviews the following Asset Liability Management (ALM) tools: Price Sensitive Gap Liquidity Gap Net Interest Income (NII) at

4 mins read ALM reports – a short review A quick review of a number of Asset Liability Management (ALM) reports used by