Gamma Correction, Delta Hedging P&L & Rebalancing Frequency

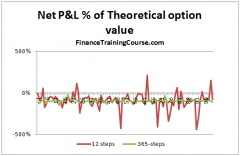

3 mins read A simple case study Theoretically speaking in the Black Scholes world the cost of the hedge should be close to

3 mins read A simple case study Theoretically speaking in the Black Scholes world the cost of the hedge should be close to

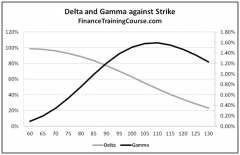

6 mins read We use a simple example to illustrate the calculation of Shadow Gamma as describe by Taleb in Dynamic Hedging. Gamma

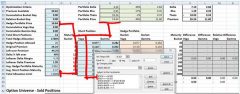

2 mins read We build a simple Excel spreadsheet that allows us to hedge Gamma and Vega exposure for a single short position

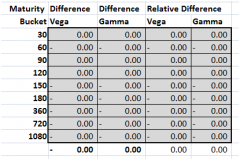

6 mins read For our portfolio model we need an objective function that allows us to minimize the cumulative Greek gap across maturity

3 mins read Lesson Four – Hedging higher order Greeks for a book of short call options We are now ready to move

3 mins read In earlier posts we have set the foundation for hedging in practice. We did this by calculating Option Price Sensitivities