Liquidity Coverage Ratio – The Numerator

3 mins read Value of Stock of High Quality Liquid Assets In our previous post on the reforms being brought to the liquidity

3 mins read Value of Stock of High Quality Liquid Assets In our previous post on the reforms being brought to the liquidity

2 mins read According to the reforms to the capital and liquidity framework, Basel III would require the banking sector to maintain and

2 mins read I recently ran a presentation for a client where I had to justify setting risk limits at a pre-defined threshold

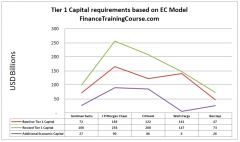

< 1 min read Ever since we started preparing ICAAP (Internal Capital Adequacy Assessment Process) submission reports the two areas where clients had the

4 mins read Why is modeling strategic risk for ICAAP so difficult? Perhaps one reason is that unlike Value at Risk (VaR) or Credit Risk, there is no agreed upon, accepted, unified framework or tool to measure, report or track the capital required to recover from a strategic misstep. What further complicates the capital estimation exercise is the fact that strategic initiatives and resulting challenges at each bank are different

3 mins read Basel III seeks to enhance the Basel II framework by addressing both firm-specific risk as well as system-specific systemic risk factors. Here, we will discuss some of major improvements being made to the Basel II framework on a macro-prudential system-wide basis as well as the greater role that stress testing will play in the process.