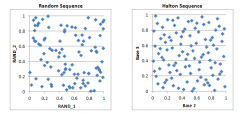

Variance Reduction: Quasi Monte Carlo & Antithetic technique

5 mins read Speeding up convergence. Using Quasi Monte Carlo & Antithetic techniques In the past we have looked at Monte Carlo Simulation:

5 mins read Speeding up convergence. Using Quasi Monte Carlo & Antithetic techniques In the past we have looked at Monte Carlo Simulation:

< 1 min read Before you begin there are two Black Scholes background posts that you will find useful in deciphering the logic behind

3 mins read Ladder options are options where the strike is reset whenever the price of the underlying asset reaches certain trigger levels

5 mins read Simulating Commodity Prices Our course on Building Monte Carlo Simulators in Excel and related available-for-sale excel examples for Commodities, Currencies

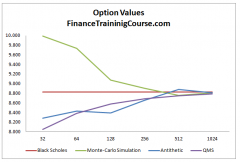

4 mins read Variance Reduction tools for Monte Carlo Simulation. Monte Carlo simulation techniques are a useful tool in finance for pricing options

2 mins read If you want to go ahead and build your own Value at Risk (VaR) model for equities, currencies, commodities and bond, check out the Calculating Value at Risk Course below. Within the calculating VaR course we walk through VCV (Variance CoVariance) and Historical Simulation, Portfolio Value at Risk and VaR for Fixed Income securities.