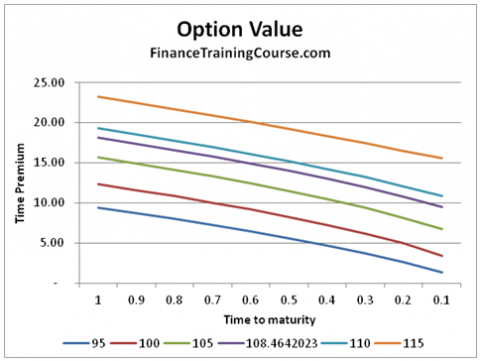

Option Greeks – Theta time premiums for call options

3 mins read Option Greeks – Theta This article is closely based on the paper “A closer look at Black–Scholes option thetas –

3 mins read Option Greeks – Theta This article is closely based on the paper “A closer look at Black–Scholes option thetas –

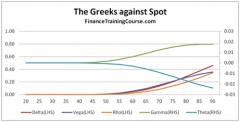

3 mins read While we have done a few posts earlier about option price sensitivities, here is a quick reference guide for the

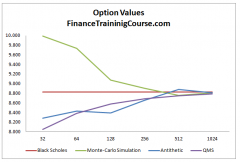

4 mins read Variance Reduction tools for Monte Carlo Simulation. Monte Carlo simulation techniques are a useful tool in finance for pricing options

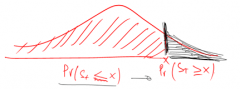

3 mins read On the other hand N(d1) will always be greater than N(d2) because in linking it with the contingent receipt of stock in the Black Scholes equation, N(d1) must not only account for the probability of exercise as given by N(d2) but must also account for the fact that exercise or rather receipt of stock on exercise is dependent on future value

2 mins read Here is the second course on Advance Interest Rate Products. The perquisite for this course is the first course on

3 mins read This road maps focuses on bootstrapping the zero curve and using the zero curve to calculate implied forward interest rates (forward curve). We then used the projected forward rates to price the swap rate for fixed to floating interest rate swap. A separate series of posts build on this material and extend its reach to pricing interest rate caps, interest rate floors, range accrual notes, commodity and equity linked notes.