Exotic Derivatives & Option pricing weekend challenge

This week exotic option pricing challenge focuses on chooser and compound option pricing using Monte Carlo Simulation in Excel. Hints to the solution will be posted separately within the next 12 hours. Let’s see if you can crack this first before I go ahead and post the solved solution. We use Apple computer to illustrate the pricing case. Enjoy.

The first set of three questions are easy and do not involve any serious rocket science. The second set (Question 4 and 5), will require you to deploy a simple option pricing hack. Do not trust and believe the obvious. And if you do, atleast check the boundary conditions that should apply to chooser option pricing compared to a similarly priced vanilla options.

For the next set of questions please use the following data and assumptions:

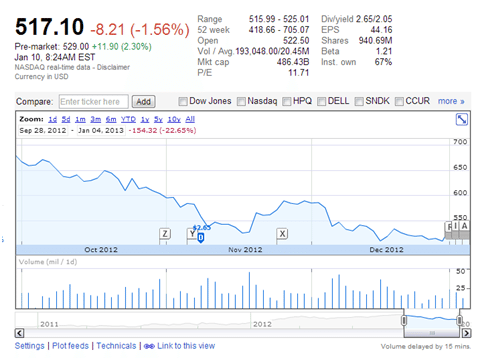

| Ticker | AAPL | Apple Computers |

| Spot Price | 517 | 52 week range is USD 418 – 715 per share |

| Strike Price | 550 | |

| Volatility – Annualized | 20% | Ranges between 9% – 40% |

| Riskfree Interest Rate | 1% | |

| Time to Maturity | 1 year | |

| Trading days in a year | 250 | |

| Expected Dividend | 0 |

Use the Black Scholes closed form formula for answering the next three option pricing questions

1. A straddle is a long position in a call option and a put option both struck at the same price. What is the cost of a long straddle issued on Apple with a maturity of 1 year and the same spot and strike price shared in the table above? Please refer to this strategy as Strategy A. (20 Points)

2. What is the cost of an out of money put struck at a strike price of 400 and a out of money call struck at 650. Lets refer to a long position in this strategy as Strategy B. (20 Points)

3. Using data tables plot a graph in excel that shows the relative return of Strategy A and Strategy B against changing volatility levels. Use the range of 5% – 40% for projected annual volatility. At what volatility level does one Strategy out performs the other? (15 points).

Use Monte Carlo Simulation to answer question # 4 & 5 on Exotic option pricing

4. The client in question has requested for a reduction in premium for Strategy A. Your structuring team suggests a chooser option. Use a Monte Carlo simulator in Excel to price a chooser option (a option to purchase a call or put option at a predefined time interval in the future on a price agreed upon today) with the same input parameters as Strategy A. Except that the client has the right buy a call or a put at exactly the same strike price 3 months from now. The strike price for the (second) option in the chooser contrat is the same as the premium calculated for a regular call with a 9 month expiry. Use 500 iterations to calculate your results. (35 points)

5. The client has also requested a comparison of the original straddle with your recommended chooser option. Using the same Monte Carlo Simulator and a data table calculate the probability that the chooser option will outperform the original straddle? Also show the total cash outlay if the chooser option is exercised versus the straddle and the out of money calls and put suggested above. (35 points)

Exotic Option pricing using Monte Carlo Simulation Excel Sheet is now available for sale

Comments are closed.