Good Data and a first look at models

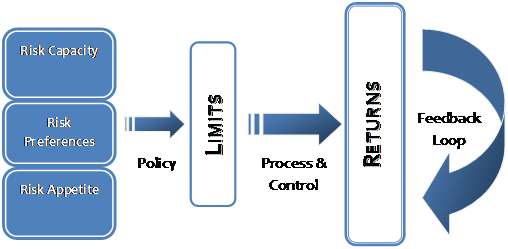

The second element in our list deals with data and models. While it is not directly visible in the risk mindset diagram above, when it comes to calculation of exposures, estimation of capital losses and allocation of capital, and using these to define risk preferences, capacity and risk appetite, data and models have the central stage.

Risk and transaction systems differ in many ways. But they both suffer from a common ailment – Good data and working models. On a risk platform the integrity of the data set is dependent on the underlying transaction platform and the quality of data feeds. Keeping the incoming stream of information clean and ensuring that the historical data set remains pure is a full time job. The resources allocated to this problem show how committed and reliant an organization is to its risk systems.

In organizations still ruled by the compliance driven check list mindset, you will find that it is sufficient to simply generate risk reports. It is sufficient because no one really looks at the results and when they do in most cases they may not have any idea about how to interpret them. Or even worse, work with the numbers to understand the challenges they represent for that organization’s future.

The same problem haunts the modeling domain. It is not sufficient to have a model in place. It is just as important to understand how it works and how it will fail. But once again as long as a model exists and as long as it produces something on a periodic basis, most Boards in the region feel they have met the necessary and sufficient condition for risk management.

Is there anything that we can do to change this mindset and fix this problem?

One could start with the confusion at Board level between Risk and the underlying transaction. A market risk platform is a very different animal from the underlying treasury transaction. The common ground however is the pricing model and market behavior, the uncommon factor is the trader’s instinct and his gut. Where risk and the transaction systems clash is on the uncommon ground. Instincts versus statistics!

The instinct and gut effect is far more prominent within business lines where prices and decisions are not just determined by market forces. Relationships and strategic imperatives drive the domain driven business. The credit and lending equation in the banking system is a great example. Analytics and models drive the credit risk side. The credit business is “name” based, dominated by subjective factors that asses relationship, one at a time. There is some weight assigned to sector exposure and concentration limits at the portfolio level but the primary “lend”, “no lend” call is still relationship based. The credit risk side on the other hand is scoring, behavior and portfolio based. A payment delay is a payment delay, a default is a default. While the softer side can protect the underlying relationship and possibly increase the chances of recovery and help attain “current” status more quickly, the job of a risk system is to document and highlight exceptions and project their impact on the portfolio. A risk system focuses on the trend. While it is interested in the cause of the underlying event, the interest is purely mathematical; there is no human side.

I asked earlier if there is anything we can do to change. To begin with Boards need to spend more time and allocate more resources to the risk debate. Data, models and reports are not enough. They need to be poked, challenged, stressed, understood, grown and invested in. Two hours once a quarter for a Board Risk Committee meeting is not sufficient time to dissect the effectiveness of your risk function. You may as well close your eyes and ignore it.

But before you do that remember hell hath no fury like a risk scorned.

This course is based on the material presented in earlier editions of Pakistan Risk Review, the soon to be released Understanding Commodity Risk textbook and the work done by Alchemy Technologies in the region in the area of financial risk management and Basel II reporting for the banking industry in Pakistan and the Middle East. It presents an extension of well accepted risk models in the financial services space to the risk management needs of the oil, gas and petrochemical industry in the region.