Interest Rate Options

The payoffs under these options are dependent of the level of interest rates.

Bond Options

This is an option to buy/sell a specified bond for a predetermined price within a specified period of time. Most bond options tend to be European.

Embedded Bond Options

Callable bonds give the issuer of the bond the right to buy back the bond for a predetermined price at a specified time or times in the future. Other features of callable bonds are:

- The issuer usually cannot call the bond in the initial years of the bond

- The call or strike price decreases with time

- Callable bonds tend to have higher yields as compared to those which do not have any call option features

Puttable bonds give buyer of the bond the right to redeem the bond at certain specified times before the maturity date for a predetermined price. Other features include:

- Lower bond yields as compared to bonds without out option features

Interest Rate Caps/ Floors/ Collars

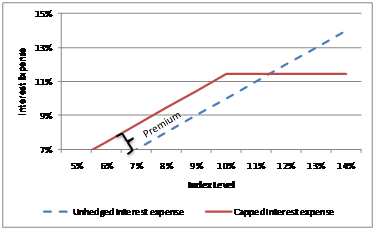

An interest rate cap provides a payoff when the interest rate at reset on the underlying floating rate note exceeds a specified maximum known as the cap rate. The payoff is the difference between the actual interest rate payment at reset and the interest rate payment based on the cap rate adjusted for the appropriate day count convention. This pay off is not made on the reset date when this excess interest rate was observed but at the end of the following tenor (i.e. reset period).

The following graph depicts how an interest rate cap caps the interest expense of an institution that purchases this derivative to hedge their LIBOR-indexed liabilities.

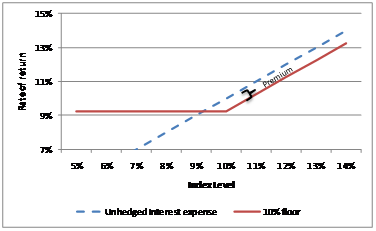

An interest rate floor provides a payoff when the interest rate at reset on the underlying floating rate note is below a specified minimum.

The following graph depicts how the interest rate floor is used by an institution to protect the return on its floating rate assets:

An interest rate collar or floor-ceiling agreement provides a payoff when the interest rate at reset on the underlying floating rate note is either below or above a specified range. It can be consider as having a long position in an interest rate cap and a short position in an interest rate floor. The net cost of the collar is therefore zero.

European Swap Options

This is an option on an interest rate swap, also known as a swaption. The contract buyer has the right to enter into an interest rate swap at a predetermined time in the future. This is usually done to ensure that the fixed rate payments that they will commence making in the future in exchange for receiving floating rate payments will not exceed a certain level. They will not exercise their right if they can enter a more favorable interest rate swap that offers a lower fixed rate as compared to that offered in the swaption.

Comments are closed.