Deriving the Forward Curve

Step 9: Deriving forward rates

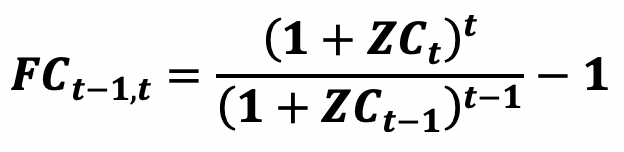

In order to derive forward rates from the zero coupon rates for successive interest rate periods, the bootstrapping methodology has been employed. In particular, the following formula has been used:

Where t is the tenor in years, ZCt is the zero coupon rate for a tenor of t years and FCt-1,t is the forward rate for the period (t-1,t).

For example, the forward rate for the interest rate period 3 years to 4 years using zero coupon rates is

The forward rates are as follows is our example:

| t | FCt-1,t |

| 1 | 12.150% |

| 2 | 12.405% |

| 3 | 12.643% |

| 4 | 12.525% |

Comments are closed.