Option Trading Strategies refer to a combination of trades that can be used to reduce premiums, reduce downside, reduce upside, increase leverage, reduce leverage or a combination of one or more of the above elements. We start off with a review of the simplest of option trades and then use them as building blocks for other more complex combinations.

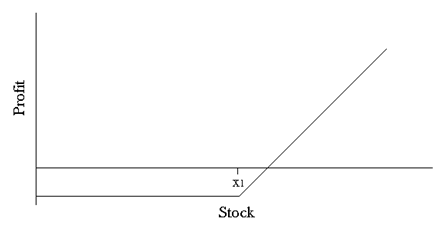

Long Call

A call option is suitable when your outlook for the market is bullish. Since you are purchasing the call option, you need to allow enough time to expiration for the stock to move and reduce the effect of time decay.

The potential gain in this strategy is unlimited, whereas, the maximum loss is limited to the initial premium paid.

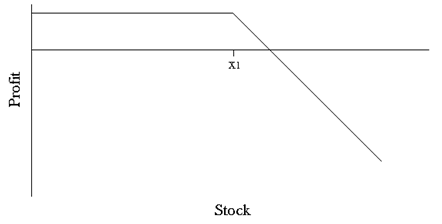

Short Call

Selling a call option is suitable when you anticipate the stock to move lower, sideways or stay below the strike price. This will have the call option expire worthless and you will be able to keep the entire premium. Since you are selling the call option, you need to use short time to expiration to take advantage of time decay and give the stock less time to move against you.

However, this strategy is very risky, as the maximum gain is only limited to the premium collected, whereas, the potential loss is unlimited.

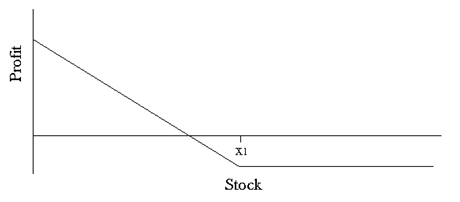

Long Put

A put option and is suitable when your outlook for the market is bearish. Since you are purchasing the put option, you need to allow enough time to expiration for the stock to move and reduce the effect of time decay.

The potential gain in this strategy is limited by the amount the stock has to fall before it touches zero. The maximum loss is limited to the initial premium paid.

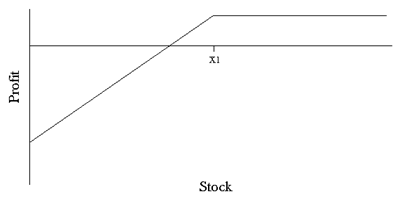

Short Put

This strategy requires you to sell a put option and is suitable when you anticipate the stock to move higher, sideways, or stay above the strike price. This will have the put option expire worthless and you will be able to keep the entire premium. Since you are selling the put option, you need to use short time to expiration to take advantage of time decay and give the stock less time to move against you.

However, this strategy is very risky as the potential loss is substantial, but limited by the amount the stock can fall before it hits zero. Maximum gain is only limited to the premium collected.

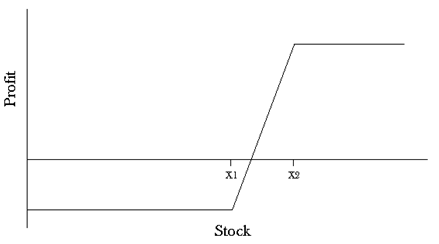

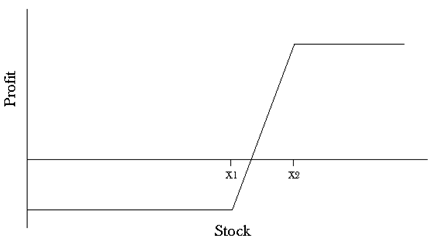

Bull Call Spread

This strategy is suitable when your outlook for the market is bullish. It requires you to purchase a call option and sell another call option at a higher strike price with the same expiration date. This limits your profit when compared to a long call, but also reduces the risk as it reduces your cost to purchase the call option.

The maximum loss, in this case, is limited to the difference of initial premiums (paid and received), whereas the gain is limited to the difference between the two strike prices less the initial premium paid.

Bull Put Spread

This strategy is suitable when your outlook for the market is bullish. It requires you to purchase a put option and sell another put option at a higher strike price with the same expiration date. This will lead the put options to expire worthless and you will be able to keep the entire premium collected. Since you are selling the put option, you need to use short time to expiration to take advantage of time decay and give the stock less time to move against you.

The maximum gain in this case is limited to the difference of initial premiums (paid and received) whereas the loss is limited to the difference between the two strike prices less the initial premium collected.

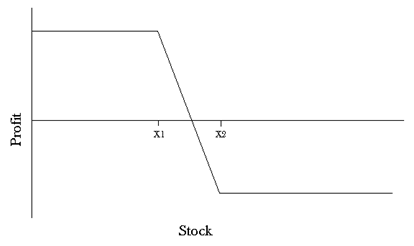

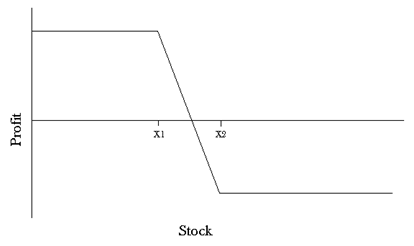

Bear Put Spread

This strategy is suitable when your outlook for the market is bearish. It requires you to purchase a put option and sell another put option at a lower strike price with the same expiration date. This limits your profit as compared to a long put, but also reduces the risk as it reduces your cost to purchase the put option.

The maximum loss in this case is limited to the difference between initial premiums (paid and received), whereas the gain is limited to the difference between the two strike prices less the initial premium paid.

Bear Call Spread

This strategy is suitable when your outlook for the market is bearish. It requires you to purchase a call option and sell another call option at a lower strike price with the same expiration date. This will lead the call options to expire worthless and you will be able to keep the entire premium collected. Since you are selling the call option, you need to use short time to expiration to take advantage of time decay and give the stock less time to move against you.

The maximum gain in this case is limited to difference between the initial premiums whereas the loss is limited to the difference between the two strike prices less the initial premium collected.

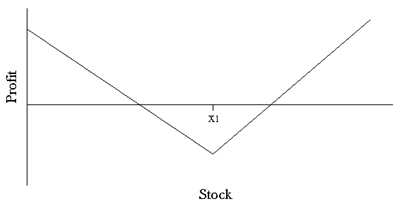

Long Straddle

This is a non-directional strategy, suitable for when you expect a price breakout, but are not sure about the direction. This requires you to purchase a call and a put option at the same strike price and expiration month. Since you are purchasing the options, you need to allow as much time as possible to expiration for the stock to move and reduce the effect of time decay.

The maximum loss in this case is limited to the premiums paid for both the options. On the other hand, the maximum gain due to the call option is unlimited; whereas, that due to the put option is limited to the strike price less the initial premiums paid.

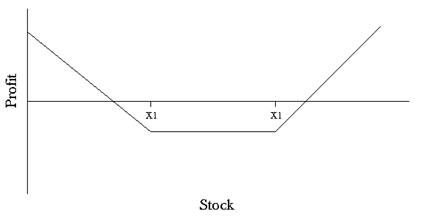

Long Strangle

This strategy is somewhat similar to the “Long Straddle” and is also suitable for when you expect a price breakout, but are not sure about the direction. However, this requires the purchase of out of-the-money call and put options at the same strike price and expiration month. The out of-the-money options reduce your overall cost, but the stock will have to make a greater move for this strategy to be profitable. Hence, you need to allow as much time as possible to expiration to give the stock enough time to move and reduce the effect of time decay.

The maximum loss in this case is limited to the premiums paid for both the options. On the other hand, the maximum gain due to the call option is unlimited; whereas, that due to the put option is limited to the strike price less the initial premiums paid.

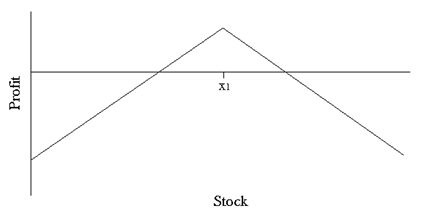

Short Straddle

This is also a non-directional strategy suitable for when you expect the stock to move sideways. This requires you to sell a call and a put option at the same strike price and expiration month. It is a very risky strategy since you are selling two naked options, hence you should allow as little time as possible to expiration for the stock to move against you, so that the options expire worthless.

The maximum gain in this case is limited to the premiums collected for both the options. On the other hand, the maximum loss due to the call option is unlimited; whereas, that due to the put option is limited to the strike price less the initial premiums collected.

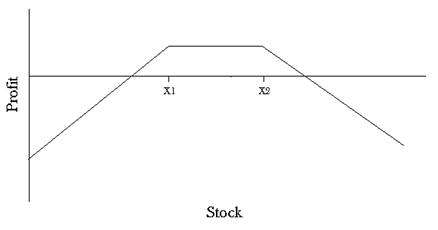

Short Strangle

This strategy is somewhat similar to the “Short Straddle” and is suitable for when you expect the stock to move sideways. However, this requires you to sell an out of-the-money call and put options at the same strike price and expiration month. It is a very risky strategy since you are selling two naked options, hence you should allow as little time as possible to expiration for the stock to move against you, so that the options expire worthless.

The maximum gain in this case is limited to the premiums collected for both the options. On the other hand, the maximum loss due to the call option is unlimited; whereas, that due to the put option is limited to the strike price less the initial premiums collected.

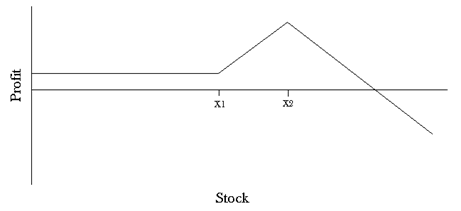

Call Ratio Spread

This strategy is suitable for when you expect the stock to move either sideways or slightly higher. This requires you to purchase a call option, while simultaneously selling more call options at a higher strike price in a ratio of 1:2 or 1:3. Hence, it is a combination of a “Bull Call Spread” and naked calls. Selling naked calls makes the strategy very risky, so you need to allow as little time as possible for the stock to move against you, so that the short options expire worthless.

The maximum gain in this case is limited to the difference between the short call and the long call strike prices, add (less) the premiums collected (paid). On the other hand, the potential loss due to the short options is unlimited.

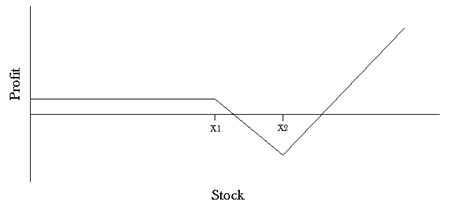

Put Ratio Spread

This strategy is suitable for when you expect the stock to move either sideways or slightly lower. This requires you to purchase a put option, while simultaneously selling more put options at a lower strike price in a ratio of 1:2 or 1:3. Hence, it is a combination of a “Bear Put Spread” and naked puts. Selling naked puts makes the strategy very risky, so you need to allow as little time as possible for the stock to move against you, so that the short options expire worthless.

The maximum gain in this case is limited to the difference between the long put and the short put strike prices, add (less) the premiums collected (paid). On the other hand, the potential loss due to the short options is substantial, but limited to the short strike price less the difference between the strikes less (add) the premiums collected (paid).

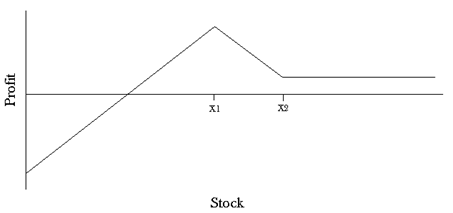

Call Ratio Back Spread

This strategy is suitable for when your outlook for the market is bullish. It requires you to purchase call options and sell fewer call options at a lower strike price, usually in a ratio of 1:2 or 2:3. The short calls finance the purchase of the long call options. Due to the selling of call options, the stock has to make a substantial move in order for you to realize a profit. Hence, you need to allow as much time as possible to expiration for the stock to move.

The potential gain in this case is unlimited. On the other hand, the maximum loss is limited to the long strike less the short strike less (add) the premiums collected (paid).

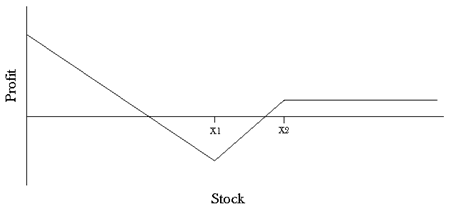

Put Ratio Back Spread

This strategy is suitable for when your outlook for the market is bearish. It requires you to purchase put options and sell fewer put options at a higher strike price, usually in a ratio of 1:2 or 2:3. The short puts finance the purchase of the long put options. Due to the selling of put options, the stock has to make a substantial move in order for you to realize a profit. Hence, you need to allow as much time as possible to expiration for the stock to move.

The maximum gain in this case is substantial, but limited to the long strike less the difference between the strikes less (add) the initial premiums paid (received). On the other hand, the maximum loss is limited to the short strike less the long strike less (add) the premiums collected (paid).

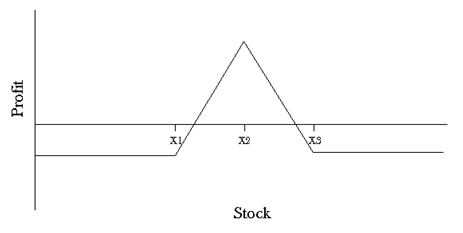

Long Butterflies

This is a non-directional strategy which requires the use of all calls or all puts. For example, a long call butterfly may be created by purchasing a call option, selling two calls at a higher strike price and purchasing another call at an even higher strike price. The key here is that the number of options purchased is equal to the number of options sold, with the strike prices evenly spaced out.

The maximum gain in this case is limited to the difference between the long and the short strike prices less the initial premium paid. On the other hand, the maximum loss is limited to the initial premium paid.

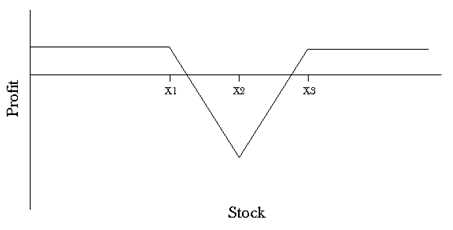

Short Butterflies

This is also a non-directional strategy which requires the use of all calls or all puts. For example, a short call butterfly may be created by selling a call option, purchasing two calls at a higher strike price and selling another call at an even higher strike price. The key here again is that the number of options purchased is equal to the number of options sold, with the strike prices evenly spaced out.

The maximum loss in this case is limited to the difference between the long and the short strike prices less the initial premium collected. On the other hand, the maximum gain is limited to the initial premium collected.

Comments are closed.