Duration Convexity and Asset Liability Management

What is the relationship between Duration, Convexity and Asset Liability management. Let’s take a quick look

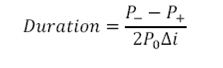

Duration

Duration is defined as interest rate sensitivity. For the purpose of this post modified duration is calculated by estimating the price change per unit of interest rate change.

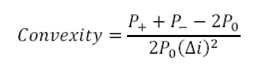

Convexity

Convexity is a second order change that estimates the error within our duration estimates. It is also viewed as that property of an asset or liability that allows it to rise by more and fall by less when interest rates change.

Where,

Δi= change in yield (in decimals)

P0= Initial Price

P+= Price if yields increase by Δi

P–= Price if yields decline by Δi

Approximate Price Change

Total estimated percentage price change= -Duration×Δi×100+Convexity×(Δi)2×100

Surplus Immunization using duration convexity

If we view asset liability management (ALM) as a process that focuses on protecting economic value of equity or share holder value then an ALM framework should focus on insuring interest rate changes should have minimal impact on share holder value (surplus).

To protect surplus or immunize it against interest rate changes two conditions must be met.

Weighted average duration of assets = weighted average duration of liabilities

Weighed average convexity of assets > weighted average convexity of liabilities

Duration Gap estimation

To estimate the impact of interest rate changes on economic value of equity or shareholders value we use a neat approximation tool called duration gap. Duration gap allows us to bucket asset and liabilities based on days to maturity (DTM) and then used a combination of bucket gaps (the difference between assets and liabilities across that maturity bucket) and cummulative gap to estimate the net impact of interest changes on both side of the balance sheet.

The duration gap report uses effective or modified duration and produces an estimate for the shift in economic value of equity for a unit of interest rate change (generally 100 basis point shift).

These are the two primary usage of duration and convexity within the asset liability management framework.

Comments are closed.