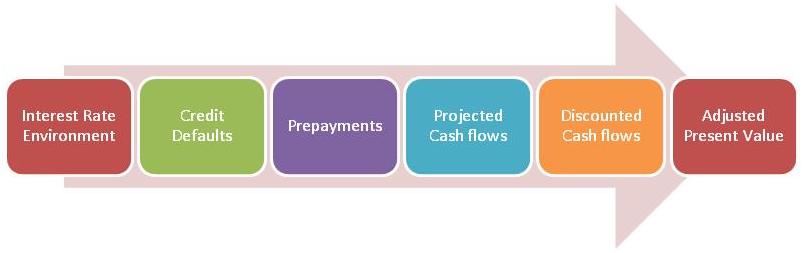

Mortgage-backed securities (MBS) are complex instruments with just as complex valuation models. A valuation model develops a pricing mechanism for a mortgage backed security using multiple classes of assumptions across a range of scenarios. These assumptions are themselves generated by sub-models and include:

- An interest rates model to project interest rates in the economy and the applicable rate for the loans in the portfolio.

- A prepayments model to project prepayments for the loans in the portfolio.

- A model for projecting credit related default for the loans in the portfolio.

- Combining the three models above to project cash flows over the life of the portfolio. Allocating them to the relevant and appropriate investor packages.

- Discounting these cash flows at the appropriate discount rate to determine the present value of future cash flows for a given investor package.

- More sophisticated approaches adjust these cash flows and present values for the options embedded in the underlying loan product.

Below is a review of the three assumptions that have to be modeled for the mortgage backed securities valuation model:

1. The interest rate model for the economy

On the interest rate modeling side there are two primary families of models.

a. Equilibrium model

An equilibrium model is based on a simplified macro model of interest rate drivers. For instance, the Cox Ingersoll Ross (CIR) model assumes a mean reverting process. If rates go up, they must come down, if they come down they must go up. It includes a long term average rate and an adjustment process that pulls interest rates back to the long term mean.

b. Arbitrage free model

An arbitrage free model calibrates the output of the model on day one to the existing interest rate environment. This ensures that there are no opportunities for mis-pricing or arbitrage on day one between the real world and the interest rate model. For example, the Black Derman and Toy (BDT) model calibrates the existing interest rate environment as represented by zero curves and the volatility at each point in the term structure with the model to project the entire forward rate term structure.

2. The credit default model for the economy and a given MBS pool

A default model for the mortgage back securities valuation model projects multiple factors dealing with the economy in general as well as the underlying portfolio of loans in specific. The economic model forecasts interest rates, the impact of a change in rates on housing prices and purchase and sale activity in the housing market as well as unsold inventory at the broader level. At the loan level, it looks at the loan to value ratio and the value of the option for the homeowner to default.

3. The prepayment model for the economy and a given MBS pool

A prepayment model projects the amount and likelihood of prepayment and its impact on the life of the mortgage as well as the overall timing of cash flows for the portfolio of loans.

When a borrower exercises the pre-payment option, the borrower pays down either a portion of the outstanding principal or the entire outstanding principal. Prepayments can occur for a number of reasons:

- Sells home: If a homeowner chooses to relocate to another home, the mortgage property will get sold and trigger a prepayment.

- Refinances: When interest rates fall, a homeowner can benefit from refinancing at lower rates to reduce his monthly mortgage payment.

- Defaults: The buyer defaults & the property is foreclosed and sold.

The prepayment model uses multiple factors to simulate the prepayment behavior of homeowners. These factors may include:

- The yield curve at origination. The difference between the yield curve at the point of origination and the point of re-financing accurately reflects the true monetary incentive for a homeowner to re-finance.

- The spread at origination represents any non-standard features of the loan. These may lead to higher margins, fees and premiums as well as effect re-financing and closing costs.

- The loan size (amount of loan) factor.

- The home appreciation factor and the equity cash out incentive for a homeowner.

- The housing turnover factor.

Comments are closed.