Accounting short course: Introducing the Trial Balance

Until now, we have been reviewing how to record business transactions. Given the volume and details involved in recording accounting transactions tedious work and there are chances of making mistakes. Accounting systems and accounting process realizes this limitation and has a control process in place to identify, highlight and rectify such errors. The tool we use for this purpose is called a trial balance.

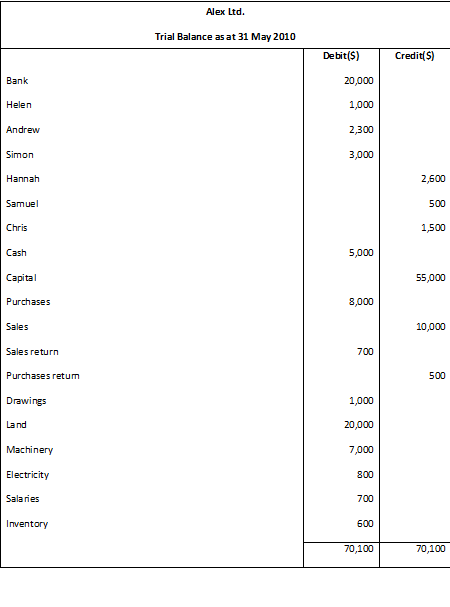

Trial balance lists down balances of all the accounts in one statement. Accounts with debit balances are listed on the debit side of the trial balance and then added together, while accounts with credit balances are listed on the credit side and added together. If everything is right and there are no mistakes then both balances (debit and credit) should balance as we expect every debit to have a offsetting credit. If the balances don’t match then there is some problem in the accounts and we have to go through our accounts again to find the errors. We have drawn a sample trial balance on the next page.

Sample trial balance

In the trial balance above, you may notice that there is a new term that has not been introduced as yet i.e. ‘Drawings’. Drawings is the withdrawal of cash or goods by the owner of the business from the business for their private use. Please note that the business and the owner of the business are two separate entities and any withdrawal made by the employer has to be recorded in the business accounts under the head of drawings. If the owner withdraws cash from the business, we will debit the drawings account and credit the cash account. On the other hand, if he withdraws inventory we will debit the drawings account and credit the purchases account in the general ledger. Drawings account is found in the general ledger.

Comments are closed.