Basel Gap Analysis

For a Treasury Middle Office gap analysis exercise roadmap is defined by the market risk capital amendments (1996) and the Basel II guidelines that specify a number of qualitative and quantitative criteria required before supervisory approval for an internal model is granted.

Even though the guidelines may not be applicable to domestic commercial banks at this point, with the implementation of Basel II they would represent the benchmark used locally and internationally. We use the qualitative and quantitative criteria as an independent benchmark for ranking and rating risk management functions. The qualitative criteria specifies general benchmarks while the quantitative criteria specifies a checklist with respect to the Value at Risk (VaR) calculation methodology. Value at Risk in the context of this section implies a portfolio VaR including the combined risk effects of Equity, FX and Money Market securities.

The tables in the next two sections present the result of this evaluation for Client Bank. For benchmarking purposes the last column in each table also provides the score of a comparative exercise based on a survey of eleven Banks and DFI’s covering one third of banking assets in Pakistan (more than one trillion rupees in balance sheet assets). Criteria used for assessment include:

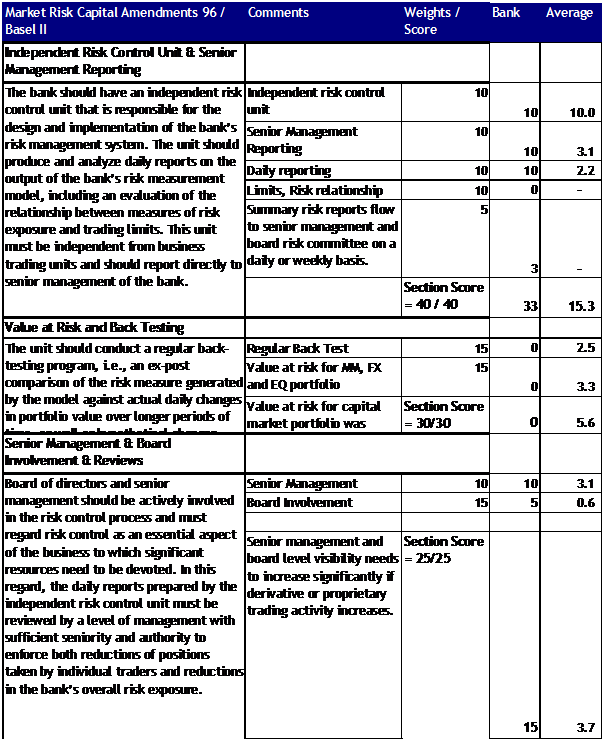

a. Independent Risk Unit and Senior Management Reporting

b. Value at Risk and Back Testing

c. Senior Management and Board involvement and reviews

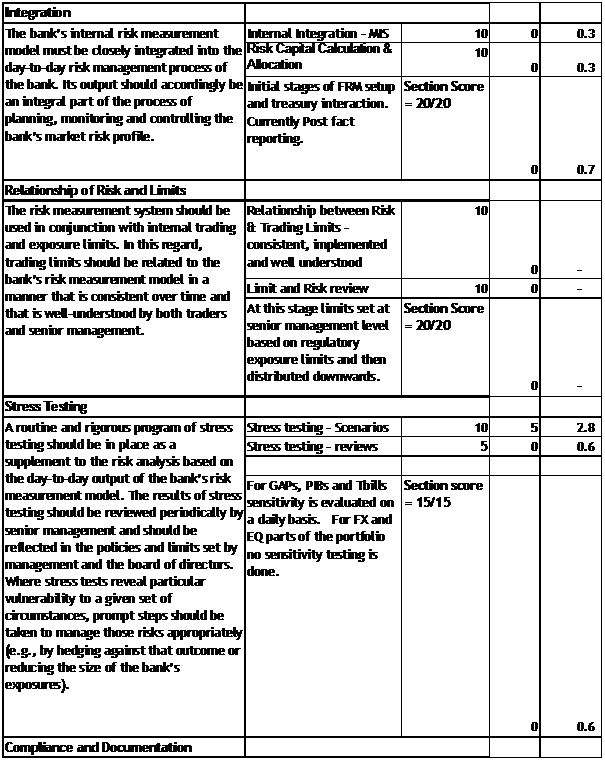

d. Integration

e. Relationship between Risks and Limits

f. Stress testing

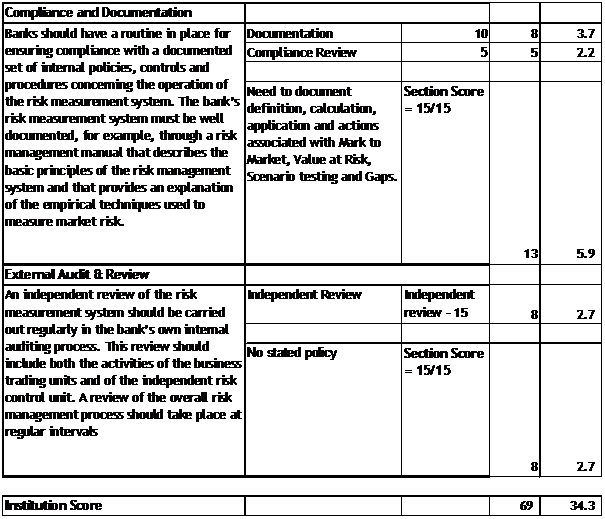

g. Compliance and Documentation

h. External Audit and Review

Of these (c), (d), and (e) above (Senior Management and Board involvement, Integration and relationship between risks and limits) are the most difficult and will require the most effort at any institution. (a), (f) and (g) above (Independent Risk Unit and Senior Management Reporting, Stress Testing and Compliance and Documentation) are primarily in place at a large percentage of surveyed institutions while (b) and (h) above (Value at Risk and Back Testing, External Audit and Review) are either being explored or in the process of being setup. The maximum possible score on the evaluation was 180 and of the eleven institutions benchmarked Client bank was grouped in the first four institutions (top 30%) that have set up processes, allocated resources and completed documentation and compliance requirements.

The work that now needs to be accomplished deals with senior management involvement, the risk management mindset, integration of the middle office function in day to day reporting and decision making and rolling out value at risk and back testing models. Once the models are in place an additional requirement is calculation of a daily capital charge for the trading book as defined under the quantitative criteria. Depending on market conditions and the risk profile of the trading book this capital charge may be substantially less than the capital requirements imposed under the standardized approaches. Deployment of this capital charge calculation is also the first step towards more risk sensitive limits, the integration of middle office analysis in risk taking and decision making behavior and the evolution of the middle office function to a higher stage.

Qualitative Criteria

Quantitative Criteria

| Market Risk Capital Amendments / Basel II | Client Bank MO Unit |

| “Value-at-risk” must be computed on a daily basis. |

Daily VaR – No. PortfolioPortfolio VaR here implies a Var that includes FX, Equities & Money Market securities. |

| In calculating the value-at-risk, a 99th percentile, one-tailed confidence interval is to be used | 99% – NoNo VaR calculated as yet |

| In calculating value-at-risk, an instantaneous price shock equivalent to a 10-day movement in price is to be used, i.e., the minimum “holding period” will be ten trading days. Banks may use value-at-risk numbers calculated according to shorter holding periods scaled up to ten days by the square root of time | Holding period – NoNo VaR calculated as yet |

| The choice of historical observation period (sample period) for calculating value-at-risk will be constrained to a minimum length of one year. For banks that use a weighting scheme or other methods for the historical observation period, the “effective” observation period must be at least one year (that is, the weighted average time lag of the individual observations cannot be less than 6 months) | Observation period – NoNo VaR calculated as yet. |

| Banks should update their data sets no less frequently than once every three months and should also reassess them whenever market prices are subject to material changes. The supervisory authority may also require a bank to calculate its value-at-risk using a shorter observation period if, in the supervisor’s judgment; this is justified by a significant upsurge in price volatility | Data review – NoNo VaR calculated as yet. |

| Banks will have discretion to recognize empirical correlations within broad risk categories (e.g., interest rates, exchange rates, equity prices and commodity prices, including related options volatilities in each risk factor category) | Empirical correlation – No.Recognized between similar asset types (equities) but not across markets (Equities, money markets & FX) |

| Each bank must meet, on a daily basis, a capital requirement expressed as the higher of (i) its previous day’s value-at-risk number measured according to the parameters specified in this section and (ii) an average of the daily value-at-risk measures on each of the preceding sixty business days, multiplied by a multiplication factor | Daily capital requirement – NoAverage daily value at risk calculation – NoNeed to integrate and compared market risk capital charge as calculated by Finance Division with Value at Risk based capital charge. |