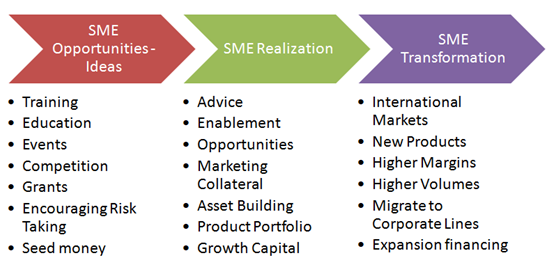

Small and Medium Enterprise (SME) Financing is classified as Retail, Middle Market and SME lending under a specialized product or program lending initiative within a commercial bank. A typical SME policy driven program has multiple components and products based on the position of the SME client within the typical SME lifecycle. While a program lending initiative at a commercial bank may only focus on one specific stage within the SME life cycle, supporting components within the program and from external partners provide what are typically referred to as non-financial component for the growth of the SME sector. These non-financial components deal with the idea generation, idea selection and startup phase of an SME client with the objective of creating client and deal flow for later life cycle stage partners in the SME chain.

For instance a business plan competition may provide the initial mentoring, training and grant based funding for an entrepreneur to test launch his product, idea or service based business. While such funding is not sufficient to sustain the business, it may be enough to help get the business to its first customer. While funding and financing sources may be limited for early stage companies, there is no shortage of training programs, business acceleration initiatives and free mentoring services for new entrepreneurs and startup businesses.

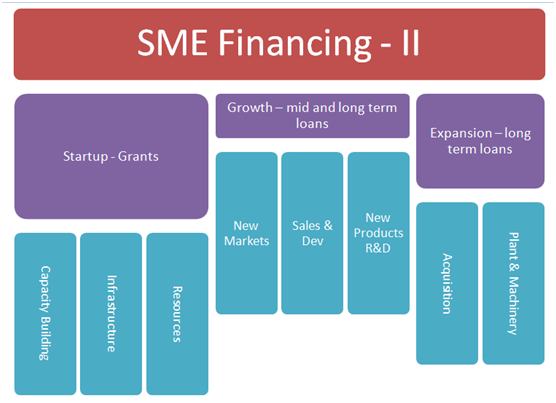

Two to three years later, after the SME has established itself and is in a position to survive on its own, it typically reaches the first scaling challenge. This generally involves investment in infrastructure, facilities, products or new markets. Again depending on the early success of the business, the SME entity in most cases can only apply for cash flow based loans that require no commitment of collateral and are primarily based on the cash or asset conversion cycle. Over a period of years as the underlying business grows the SME migrates to higher funding and financing requirements that can now be secured by balance sheet assets the enterprise has acquired by reinvesting in the business over the last few years.

This is the last stage of financing before the SME grows, matures and transforms itself into a conventional corporate customer and credit relationship which is now underwritten and serviced as part of main stream corporate line of business

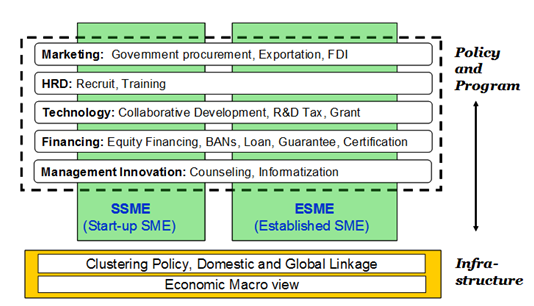

A successful SME framework combines the best of policy initiatives, program lending and infrastructure support to create a collaborative environment for SME business to succeed. These include

- Policy and program initiatives for activities that a typical SME may not budget for. Marketing, business development, training, certification, R&D and product development. A matching grant program subsidizes the cost of creating marketing collateral, industry and key customer event participation, hiring and training the right resources, quality, markets and standards certification as well as research and product development grants.

- Clustering, technology and industrial park initiatives that reduce the cost of infrastructure investments for a small business

- Domestic and International marketing initiatives that promote national linkages between complimenting sectors across geographic boundaries to bring trade opportunities closer to SMEbusinesses.

While equity financing opportunities are rare and difficult to come by they sometimes exist for strategic and critical industry segments. And where federal or sovereign grant programs are missing, an active entrepreneurial community self generates its now Business Angel Network within a single generation that then become a source of core seed capital to the next layer of entrepreneurs.

The most common model adopted by a national SME policy initiative is a credit guarantee program with the objective of facilitating lending to SME businesses. The effectiveness of such a program is debatable in emerging markets or in markets where retail banks or banks focused on the middle market segments are in short supply. The credit guarantee program can only be successful if an active distribution and reach mechanism exists for SME customers. In the absence of such a network, awareness, underwriting and disbursement may all remain a challenge. Having said that the US Small Business Administration runs possibly the most successful instance of a credit guarantee program for SME financing in terms of product limits, distribution and reach.

A sector specific direct lending program for a strategic sectors sometimes is more successful in reaching a cluster of SME customers operating in a given industry. Primarily because a credit guarantee program can take years to setup starting with the setup of the guarantee agency, the successful rating of the guarantee agency, the seeding of agency lines, the distribution and guarantee arrangements with partnership network, creation of program lending business lines at downstream banking partners, followed by the launch of the product across a national market and its eventual adoption by SME customers.

If the objective is to simply lend to a strategic sector to finance its growth so that it can take advantage of a current market opportunity, a direct program is the only option for by the time the credit guarantee program is setup and launched, the opportunity being targeted would have long faded away.