Asset Liability Management (ALM) includes effective Liquidity Management. One way of assessing a bank’s exposure to liquidity risk is to consider the gaps that exist between its assets and liabilities for pre-defined time buckets, and then calculate the cost incurred to close out those gaps. We describe the Cost-to-Close Liquidity Gap methodology in the post below.

Assets represent outflows of cash whereas liabilities represent inflows of cash. When assets exceed liabilities there is a deficit of funds which could expose the financial institution to liquidity risk. To fill the gap (net cash outflow) and remain liquid the bank will seek funding from the market.

Let us take a simple example to illustrate this situation. Today, Alan deposits an amount of USD 300 with Bank Big for a period of 3 months. Bank Big then lends this USD 300 to Clint for 6 months. Let us assume that there are no further transactions. Bank Big’s liquidity gap report as of today will look as follows:

| Duration | Up to 3 months | 3 – 6 months |

| Assets | 0 | 300 |

| Liabilities | 300 | 0 |

| Liquidity Gap | -300 | 300 |

For the time bucket ‘Up to 3 months’, there is a negative liquidity gap, where liabilities exceed assets. This represents an excess of funds. Bank Big has a net cash inflow, therefore, it has no exposure to liquidity risk.

However in the next time bucket, Bank Big has a positive liquidity gap. This indicates that Bank Big has liquidity risk exposure. It is deficient in funds due to cash outflows exceeding cash inflows during this period. In order to compensate for this lack of liquidity the bank would need to fund the gap from the market either by decreasing its assets e.g. by selling off assets and/ or increasing its liabilities e.g. by borrowing from the market.

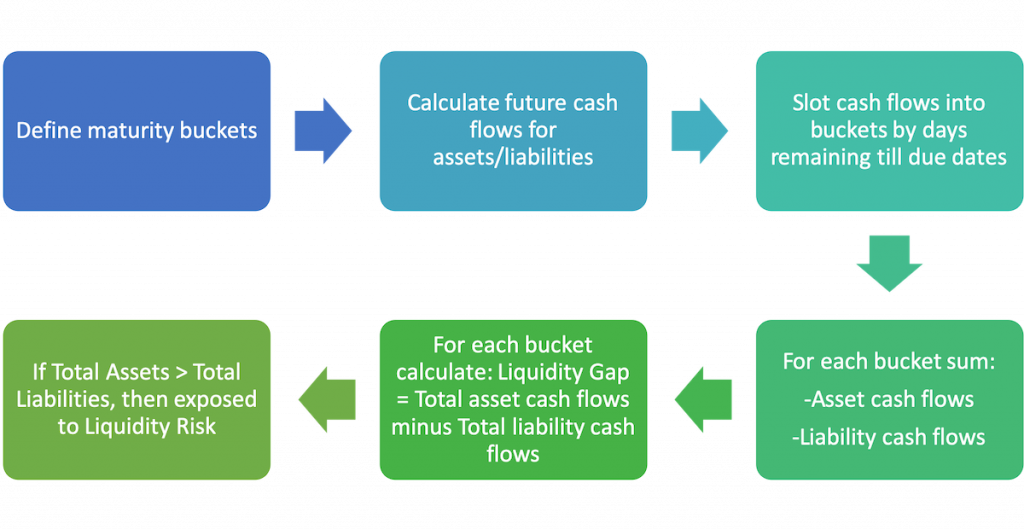

One measure of liquidity risk is the cost to close gap analysis. This analysis assumes that we do this by filling the positive gaps by borrowing from the market. The first step in this analysis is the definition of time buckets. Let us assume that the following time buckets have been defined:

- Up to 1 month (0.83 years)

- 1 month -3 months (0.25 years)

- 3 months – 6 months (0.50 years)

- 6 months – 9 months (0.75 years)

- 9 months -12 months (1 year)

- 1- 3 years (3 years)

- 3- 5 years (5 years)

The figures in brackets represent the upper bounds of the time intervals expressed in years. They are used in calculating the cost to close measure as explained later.

After this, we group all of the bank’s assets and liabilities into these time buckets according to the receipt or payment day of the cash flow, i.e. we consider the asset’s or liability’s maturity or due date as opposed to its re-pricing date. This involves first calculating each future cash flow/ installment going forward for each individual asset/ liability and then slotting each of these amounts into the relevant time buckets depending on when their expected payment or received dates. The same process, depending on the extent of the analysis, also applies to off-balance sheet items and non-funded exposures.

After slotting each individual asset and liability future cash flow into the appropriate bucket, we sum the asset values for each bucket first across each asset category (e.g. advances) and second across the asset portfolio. In the same manner, we sum the liabilities values for each bucket first across each asset category (e.g. deposits) and second across the liability portfolio.

We then calculate the difference between the total assets and liabilities for each time bucket. This difference represents the liquidity gap. A negative difference i.e. liabilities exceed assets indicate an excess of funds and could potentially be a source of interest rate risk to the bank as interest revenues (from the investment of these excess funds) could be adversely affected by movements in the interest rates. A positive difference, i.e. assets exceed liabilities indicates deficient funds which are a source of liquidity risk for the bank as the bank has a net cash outflow for that time bucket.

In this post, we reviewed a measure for assessing a bank’s liquidity risk, namely the Cost-to-Close Liquidity Gap technique. In the following post, we will present a simple example illustrating this methodology.

Comments are closed.