The post that follows is a transcript of the “Introducing the Bank Treasury Function” lecture. The lecture is part of the “Option Pricing and Risk Management” course at the SP Jain School of Management, Singapore.

Introduction

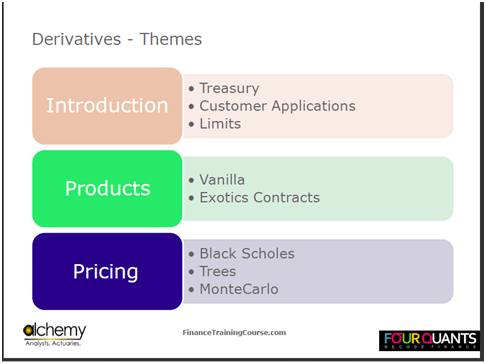

Our course on Derivatives and Options pricing has three themes:

- A brief introduction to the bank treasury function, and the sales and trading environment.

- An introduction to the universe of derivatives products, and

- A hands on review of model building and derivatives and option pricing techniques and tools.

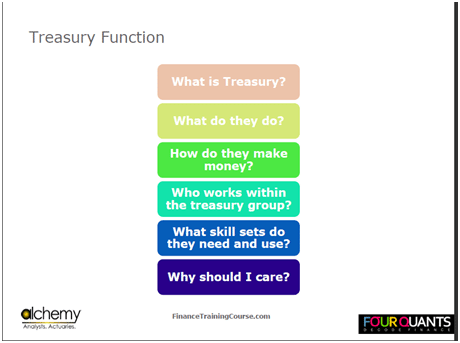

The primary challenge is to understand who uses derivative products and how exactly are they used. In most cases, you would go to a treasury department which is a part of a bank or an investment bank, and you do not represent an individual investor, but rather, an institutional investor. We, therefore, need to understand the terminology used within the bank’s treasury function and the operating environment in which these products are sold.

It is one thing to say that one understands exotics, compound options, forward rate agreements. It’s completely different to price them, to figure out how to manage their risk, and to explain them to clients.

When you deal with corporate customers, especially with large corporate clients, you do not want to talk to them in buzzwords. Rather, you want to explain the terminology to them in a language that they can easily understand. Therefore, the important thing is to build a list, where you have difficult terms on one side and their equivalent words in simple English on the other.

The best way for achieving an understanding of derivatives is by pricing the structure in EXCEL. Till you do this with your own hands, it will be difficult for to you fully appreciate how a structure actually works.

When I teach this course, I do it from two orientations. The first is the product market orientation. Most of the bank treasury function workshops that I run have no pricing elements in them. The second is pricing.

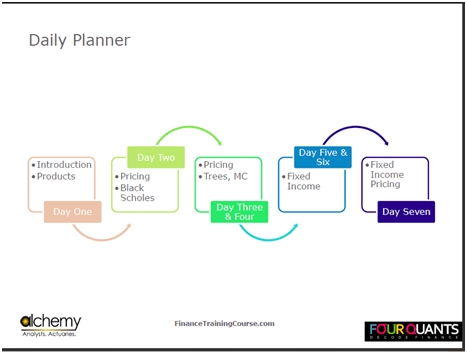

The following is the daily planner for the next seven days.

Introducing the treasury department, and sales & trading

When you work for a bank, the treasury department is the function that is responsible for ensuring that the bank has enough liquidity and presence in the market in which it operates. When you work for a corporate entity, a treasury department has more or less the same role. The difference between a treasury department at a bank and one at a corporate is that a treasury at a bank works primarily for the bank, but it also provides services for the bank’s customers. On the other hand, a corporate treasury department works only for the corporate entity.

If there is a corporate entity that borrows substantial amounts, the treasury department is responsible for ensuring that the interest costs of borrowing are managed well and there is no liquidity crunch. For instance, you should not have a $10 billion line maturing 4 days before the next $20 billion issue is coming through.

Ideally, the issue should come first and the maturity later. In addition to this, the treasury department is also responsible for ensuring that the corporate accounts have sufficient cash to make payments. If there is an entity that generates a lot of cash, then the corporate treasury is responsible for managing that cash and earning a decent return on it.

On the banking side, the treasury department is responsible for running a large part of the cash hoard of the bank. A treasury team is not a very big team, usually comprising of not more than 6 people. A group of 6 to 7 traders can very easily run a book of $10 to $15 billion.

The people managing the treasury are usually very smart people. They have a low tolerance for wasting time, especially during trading hours. The way that they make money is very simple. Irrespective of whichever market they operate in, they are able to understand the real price of a given security at a given point in time.

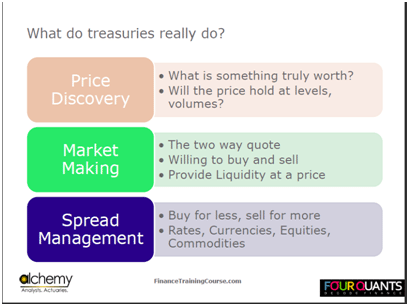

A ‘true price” can have several meanings. In the context of our discussion, it refers to the right market price. There is a term around this which is known as price discovery. Price discovery refers to the process of constantly buying and selling securities until you are able to figure out the right price for it. Treasurers and traders are very good at discovering what the right price for a trade is.

Consider the example of a mid-sized bank in the US. This bank would generate anywhere between 6,000 to 10,000 tickets in a day. A mid-sized treasury department in Karachi, Dubai or Mumbai generates between 100 to 150 tickets in a day.

Let’s say that the treasury department has four operating hours during which the bulk of its transactions take place. The treasurers have a good idea about the thresholds, the highs and the lows of the prices. This price discovery process comes from trading and assimilating information, as well as by building intuition about how things are put together. Thus, the people working in the treasury department have quick reflexes for anticipating how a market would react after a certain news item. Their mindset is always set upon figuring out ways to make money off trades.

Although investment banking, trading and treasury are primarily different fields, the primary problem in getting a treasury role is that the guys in the treasury department have no time to sit down with you and explain how their transactions work.

The reason why this course is important is that if you work hard and apply yourself, you will at least be able to start and maintain an intelligent conversation. Think about it as if you are working for Goldman Sachs for the next seven days and you are trying to impress the Managing Director(MD) who in this case is me, by asking me difficult questions which I cannot answer.

Also, think about ways of breaking this model, questioning the assumptions made and making money from this model.

Bank Treasury Function Business Model

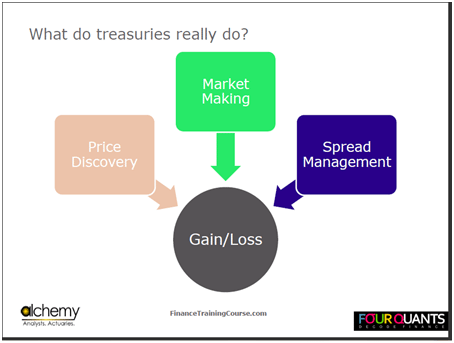

There are three ways through which treasuries make money.

The first is price discovery, i.e. figuring out how much a security is really worth, and then figuring out how to make money by trading it.

The second is to find out how to give a two-way quote, meaning that the treasury is in the market both to buy as well as to sell. Normally, when we think in terms of a transaction or a trade, we only think in terms of one step: us and the buyers or the sellers. However, in terms of derivative as well as treasury products, you need to become comfortable with the idea of multiple parties and figuring out where you stand and the price level. Depending on this price level, you would then need to decide what price you will need to quote.

The second way is also known as market making.

Think of market making as a very simple concept. Let’s assume that I want to make a market in blackboard markers. In order to do this, I will have to sell or buy them depending on what the customer wants. This means that at any given point in time, I have an inventory. I need to track the cost of my inventory so that whenever I am buying and selling with the makers, I am always trying to push my average cost down by buying below the cost, and I am pushing my selling price higher by selling above my cost.

Now, take this same concept to a bond that is illiquid because there are no buyers and sellers in the market.

If you are the person who is buying and selling that bond, you are now a market maker. It is not necessary that you hold the inventory of the maker on your own books. Depending on how well you understand the market, you can make direct, on the spot deals between buyers and sellers. We call this the market making function. Most brokers do a similar function. Exchanges also perform the same function by bringing together buyers and sellers, making them interact with each other and thus enabling them to figure out the price of different securities.

Thus, the second function that a treasury department performs depending on its mandate, is specialization in one or two securities. There are traders who specialize in treasury bills, currencies, corporate bonds, commodities, etc.

The third piece is called spread management. Spread management within a bank involves restricting the cost of funding to a level reasonably below the level earned on advances and loans. In short, it involves ensuring that the costs are less than the earnings.

These skills are important for the derivatives course because with respect to spread management and market making, there is a model price. However, whether the market accepts that price is a completely separate story.

Treasury Resource

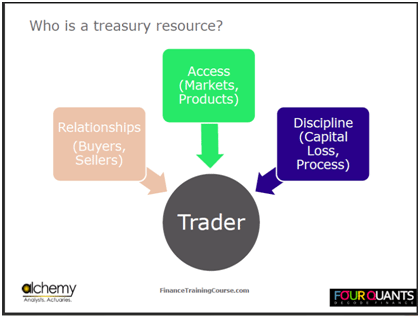

Within each treasury resource, there are three common elements:

- Relationships: A measure of the number of people who will call you when they need a specific trade done.

- Access: Whether you have the resources available in the market to buy or sell when you do get that call.

- Discipline: determining the right time for you to get out of the market.

Common Bank Treasury Trades and Products

Let’s look at the first scenario.

You are a trader on the treasury desk. A customer in Dubai tells you that he has a payment due for importing 200 BMW’s last month for his showroom. The total cost is two hundred million Dirham. Assume the exchange rate is 4.0 AED to a Euro (EUR-AED=4.0).

The Euro payment that is for 50 million Euros and this payment is due in 150 days.

The best case for the customer is if AED appreciates and Euro depreciates. The worst case is if Euro appreciates and AED depreciates.

At the current exchange rate of EUR-AED = 4.0, 50 million Euros will cost around 200 million Dirham. For an exchange rate of EUR-AED = 5.0, the cost will jump up to 250 million Dirham. At an exchange rate of EUR-AED = 3.0, the cost of 50 million Euros will fall to 150 million Dirham. The proceeds from the sale of these cars are fixed at 200 million Dirham.

Thus, the customer needs to ensure that he does not have to pay an amount more than his total proceeds. In this case, the trade will be of a currency forward contract between two parties. One of them will be the car dealer, and the other counterparty will be a bank. The dealer agrees to buy 50 million Euros at an exchange rate of EUR-AED = 4.0 in 150 days.

The risk of counterparty default or Pre-Settlement risk (PSR)

The car dealer would probably default if the AED appreciates to EUR-AED = 3.0. Its mark to market loss would be at 50 million Euros. The problem with the bank is that it does not keep these transactions on its book, but it hedges them. So, for instance, the bank made an agreement with an interbank counterparty to buy 50 million Euros at an exchange rate of EUR-AED = 3.8 in 150 days. However, if the car dealer defaults, then, the bank would be left with 50 million Euros which it has bought at a higher rate than the current market price.

We call this the risk of counterparty default. This risk is applicable to any transaction in which counterparty agrees to buy a security at a specific price at a future date, but the price of that security comes down. In risk management, this is also known as Pre Settlement Risk (PSR).

This same concept applies to oil. A customer wants to buy 10 million barrels of oil 30 days down the road. He is concerned that oil prices will rise in the future, and wants to secure himself.

For commodities, we use futures contracts instead. In this case, the counterparty is now the exchange and not the bank. The only difference between forward and futures transactions is that a futures transaction comes with margin requirements specified by the Exchange.

For instance, in the scenario described above, the current price of oil is $80 a barrel, and the total price of the customer’s order is $800 million.

The exchange would then decide a margin above this cost which the customer would also have to pay. Depending on whether the actual price of oil per barrel at the date of delivery goes up or comes down, the margin would be adjusted accordingly. This margin ensures that if the customer defaults, the exchange has sufficient depth to protect itself.

If you draw the payoff profile of either a forward or futures contract, the end result would be the same. The only difference would be the logistics of managing the margin account. On a forward contract with the bank, there is an approved credit limit which effectively serves the purpose of a margin.

Introducing the FX Swap Trade in developing markets

Let’s talk about an interesting variation of a forward contract you are likely to see in this part of the world. This transaction is very common in the developing world. It makes sense when you look at it from a high interest rate environment. Take the example of India and Pakistan.

The rate that interests us is the money market rate. Money market stands for fixed income. Within this, there are a few rates that are of interest. One is the discount window, the rate at which money can be borrowed from the central bank. Then there is an interbank rate, the rate at which banks lend and borrow money from each other. The interbank is therefore specifically limited to a financial institution.

Here’s a very simple trade. In our market in Pakistan, a bank can raise foreign currency deposits. Let us assume that:

- The bank has $10 million in deposits. It keeps it in its NOSTRO account, a counterparty account in the US because the USD settles in New York.

- The bank earns 0.25% on this deposit, which comes to around $25,000.

- It deals regularly in the interbank market. In Pakistan, let’s assume that the interbank rate is at 12%.

Thus, the bank has an asset on which it is earning only 25 basis points. Whereas if it were to borrow money, it would have to do it at a rate of 12%. To rectify this discrepancy, the bank decides to sell these dollars. The current exchange rate is PKR 100 to a dollar, which gives the bank 1 billion PKR.

Now, the bank can invest or lend this amount at a rate of 12% and earn PKR 120 million. Thus, rather than earning $25,000, the bank now earns $1.2 million. What is the risk of going for this action?

The risk would be the depreciation of the PKR. There is an interest rate differential between the USD and the PKR. The differential exists because there is an inflation differential and there is a differential between what the people anticipate the market to behave as. Due to this, there is a chance that a year or six months down the road, the Rupee would no longer be at 100 to a dollar, but may instead be at PKR 109 to a dollar. If this is the case, then, when we convert the Rupees into Dollars, the number does not add up to the initial $10 million.

The bank can, therefore, decide to structure the transaction in such a way that it does two things.

The first is that the bank sells dollars and gets PKR. At the same time, the bank also agrees to buy dollars one year from now. This effectively means that it enters into a forward contract. The forward transaction occurs at the forward rate. This is calculated as the difference between the expected inflation rate and the expected interest rate. Let’s assume that this forward rate is PKR 109 to a dollar.

At the end of the year, after paying back the customer’s share of the deposit, the bank is left with PKR 30 million.

At a rate of PKR 109 to a dollar, this amount is equivalent to 2.8% of the initial deposit of $10 million. This 2.8% is still more than the 25 basis points the bank would have made if it had only kept its money in the NOSTRO account. We call this transaction an FX swap.

The intent for doing all of this is that the bank has liquidity in one currency market and is short of liquidity in another currency market. The bank utilizes this utility in such a fashion that it is not taking any FX exposure. The bank is able to enjoy a 2% arbitrage thanks to this method. The central bank creates this arbitrage as an incentive for the dollar to remain invested in local currency terms. The central bank is paying a 2.5% premium to incentivize the investors. This trade primarily occurs in high interest rate, low hard currency developing countries because the central bank needs the dollars.