As I teach Treasury risk management across Middle East and Far East, there is one question that I really dread being asked. In most cases it is asked by an earnest young student with stars in his eyes. And without fail they all share the same profile – they are bright, young, a few years of relevant experience under their belts, strong in financial modeling, well read with a few risk or finance related charters completed. And the common question they ask with some variation is..

Would you recommend a role in treasury risk management? What is the future of treasury risk management? Should I take that offer in treasury risk management?

Unfortunately, after spending more than a decade practicing the subject, my simple answer is no. Sometimes I feel that I am too harsh so an explanation is in order.

Treasury Risk Management, today more than at any time in the recent past suffers from a serious credibility challenge. While the push to Basel II has created all sorts of expectations, roles, divisions and budgetary allocation, the reality still remains that most treasurers have a real problem with respect when it comes to middle office teams.

This challenge in credibility exists because:

Figure 1 Treasury Risk Challenges

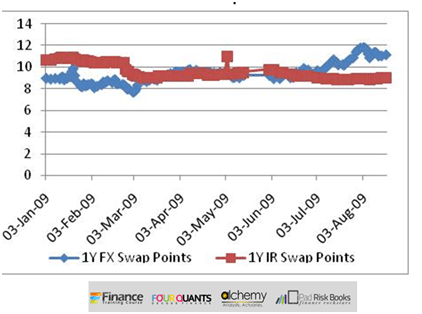

1. Treasury Risk teams routinely fail to link models to market prices and market behavior – a large part of this is driven by the fact that when it comes to data we are often forced to work with implied or indicative prices rather than real trade transactions. More often than note we divorce ourselves from the impact of trade on markets or ignore the real reason why model prices diverge or converge to market prices. For example, why do FX swap points converge at higher maturity to model prices but diverge at shorter maturities? In figure 2 below, the thick blue line is the market price, the thick red line is the model price.

Figure 2 Treasury Risk – Convergence of model and market price – the real reasons

The answer is liquidity and the difference between binding trade quotes and indicative quotes.

2. Treasury Risk teams are reliant on models that work primarily with historical data and don’t have the bandwidth, the resources or the mindset to incorporate forward looking price projections. They can drive the treasury bus by sitting in the back seat or looking out of the rearview mirror.

Figure 3 Treasury Risk – The rearview mirror syndrome

3. More importantly, Treasury Risk teams face a serious disconnect from daily trading activity. In one way this disconnect is necessary to stay emotionally un-involved from a trade. But in a different perspective, it furthers the divide between traders and risk managers. A trader will not respect you till he respects you as a trader. May God have mercy on your soul if you come across as a disconnected risk manager on a trading desk.

So the only risk roles that actually make sense or have some sort of a future associated with them are roles where:

a) You are part of an embedded risk function reporting directly to the head of trading/business – not the head of risk. These positions are not that uncommon and you have to search for them – you will generally find them with the ambit of the head of ALM or head of structuring – go forth, seek and accept without a thought if you get an offer in this area. They are more common in the big 5 (London, New York, Tokyo, Hong Kong, maybe Singapore) money centers of the world, less common in the Middle East and North Africa.

b) You are part of a risk function that is lead by a risk head who came from business and is in effect the second most powerful person in the bank. He has direct access to the board, has a track record, a mile long whip and is not afraid to use it. I see this structure once in a while and the common thread is the absence of a dotted reporting line to the President and a direct reporting line to the board or the board risk committee.

c) You are part of a team where the risk reporting unit is created and sponsored by the business side – not by corporate governance, compliance or regulatory reporting teams. Where the risk team works hand in hand with the business team. Once again this is the rarest of animals and if you are lucky enough to find it, please say yes when they offer.

The other choice is to pick between market and credit risk. Market risk has certainly become more exciting and sexier in the last twenty years but the unfortunate fact remains that more than 70% of a bank’s balance sheet is invested in credit assets. While liquidity may drive some treasuries to have larger than normal treasury asset portfolios, the real money is still in credit risk. Also at a junior analyst level, there is more work, possibly boring, but still work at the credit underwriting function and the skill is transferable from one employer to the next.

Please don’t get me wrong. There are great treasury risk teams out there with a bright sunny future ahead of them. There are certainly enough of them around given the number of banks that exist today in this world. But there are more treasury risk teams out there are that are simply miserable and often clueless on how to deal with disrespectful traders that they would classify as rude or obnoxious.

The holy grail for a treasury risk team member is to think like a trader but act like a risk manager in such a fashion that treasury teams ask for your input not because you are risk manager but because you add real value by your analysis. The trick, however, is to remember that there is a fine line that cannot be crossed between being a risk advisor and being a risk taker.