Loan officer skill sets.

Between a credit analyst and a relationship manager.

A successful loan officer (credit analyst and/or relationship manager) wears many hats.

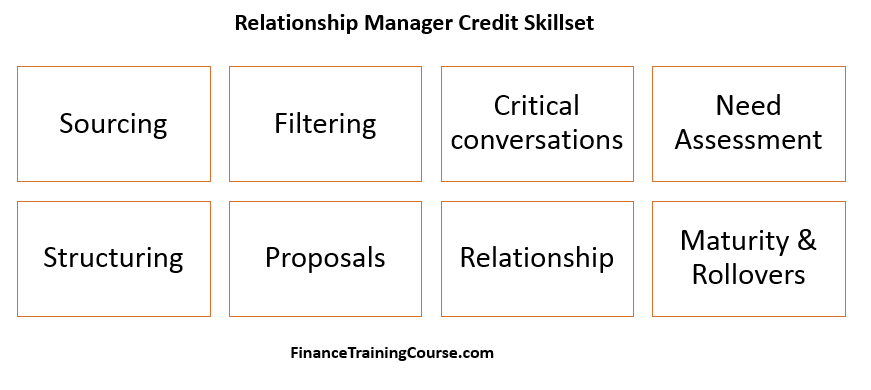

Sourcing is his first hat. To be on the lookout for customers with the right profile and numbers who are looking for an extension in credit. The challenge here is that qualified customers are generally spoken for and banking relationships, especially those associated with an existing credit facility are not that easy to break or move. Especially if the original bank is still interested and keen in retaining that customer. Sourcing requires prospecting, lead generation, client visits and multiple conversations. stuff that can only happen if you hit the road. Then comes the filtering hat. No one in their right mind declines free or easy money. Identifying customers who fit the criteria specified for a relationship, where the intent and sources for repayment are clear and the objective of the transaction being conducted using the credit facility acceptable to the bank, requires effort, consistency and diligence.

Being on the ground a loan officer / relationship manager is possibly the best judge of intent, transaction and usage. Which also puts him in the right position to determine if the structure and product being proposed are the best fit for the transaction being financed. In comes the need assessment hat. Will the proposed limits be sufficient? Would they need to grow or shrink over the next few years based on the original requirement of the business? Will the business be able to bear the additional burden? If the market heads south and liquidity disappears will the customer be able to repay and settle using current sources? Is there sufficient margin for a forced sale haircut if we end up going the collateral route? In growing economies with ample liquidity chasing too few customers, getting customers to understand and agree to the rationale for covenants in a term sheet is difficult. In recessions finding customers or getting the credit approvals to approve the same customers is difficult. The relationship manager essentially plays the role of a facilitator; representing the point of view of both sides to the other. Customers on one side; Credit approvals on the other side. Running interference till the transaction closes to mutual satisfaction. But this ground work has to be done before the credit proposal is finalized for submission so that the acceptable range for a decision for clients as well as approvals is known well in advance.

Great relationship managers understand that a one off is not a relationship, that business needs grow and change over a period of time and there is a reason why ATM machines have not been able to replace loan officers.

Building up the credit proposal

We have already discussed the requisite mindset for both lending and borrowing earlier on this site. Now comes the question that drives everything? Can you support and justify your recommendations with actual numbers and facts? Enter the credit proposal.

A good credit proposal can only be built from the ground up. Once again the relationship manager / loan officer is one of the few individual in the equation who has the complete picture and can represent the point of view of both sides. If in his judgement the client transaction is worth of an effort, he has to put on his credit committee hat to figure out how to tell this side of the story.

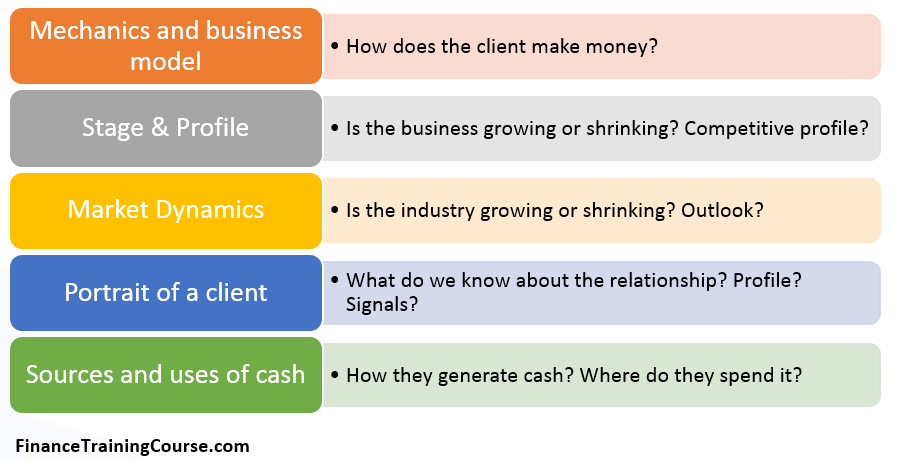

First comes the context for the business and the client.

Then comes the cash.

Once the business, industry and transaction context is over the core foundation of the credit proposal is the analysis of cash. How does the business generate and consume cash? How does this ability to generate cash compares with others in the same field? Is this likely to change over coming years? What factors would drive this change? Are these factors predictable and controllable? Are they static, slow moving or dynamic? How dramatically would they impact revenues when they change tomorrow?

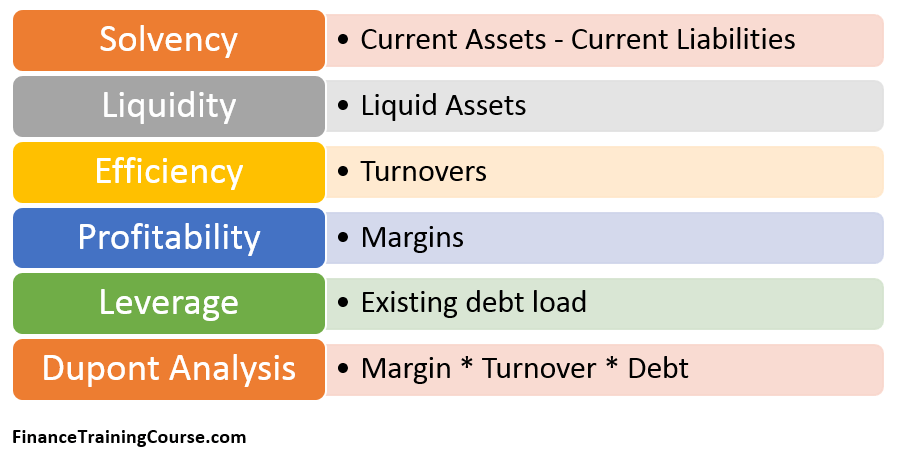

We use many tools to answer these questions. Using a combination of financial ratio analysis, balance sheet and P&L review we run numbers to estimate the debt servicing load a business can bear. Using competitive positioning and strengths, market history and repute and bench marking against industry, sector and segment databases a portrait of a client is painstakingly put together. We don’t do it just for the current year, we run it for anywhere between three to five years. The objective is to look at trends and history to see how we got here and if we can discern where we are going. Questions come up that can only be answered by additional client conversations. Some of these queries are awkward and difficult but we want to rule out elements of potential fraud as well as divergence of cash from business to owners structured as legit commercial transactions. And if indicators suggest that this may indeed be the case, we reset and start all over again.

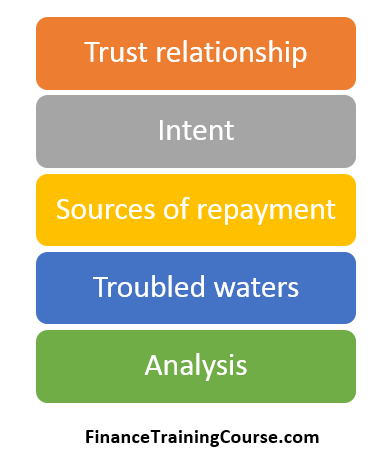

Finally when our proposal makes it all the way to the credit committee, we have to be prepared to answer the core questions. How strongly do we rate the trust factor in this relationship? Have we been able to read the intent behind the transaction correctly? Do we have at least two secured sourced of repayment? How will this transaction sail in troubled waters? Do we understand the drivers that impact cashflows as well as their outlook? Are we getting any conflicting signals from our financial and non financial analysis? How did we get here?

Remember as loan officers and relationship managers we are the closest to the ground. Our input shades the light used by the credit committee to review the proposal. We can only answer the questions if we have asked them before. We can only satisfy the challenges if we are satisfied with our analysis. That preparation shows in the confidence with which we pitch. The committee certainly looks at the numbers and the structure. But it looks much more closely at how well thought out and deep your answers are and the confidence with which they are presented.