Before the 2008 financial crisis the incentive for investors to buy mortgage backed securities was simple. For roughly the same implied credit risk as US sovereign risk you had the option to earn excess returns. It was somewhat like buying a 30 year US Treasury mortgage bond guaranteed by US treasury with a coupon higher than what the benchmark rate for 30 year treasury debt was.

Payments on specific mortgage backed security issuances were backed and guaranteed by government entities or agencies with either an implicit or explicit federal government line of support. For some the assurance was assumed given the importance of the housing market to the US economy. For others it was explicitly backed by a line of credit with the US Treasury.

Obviously the comparison wasn’t accurate because securitized mortgage backed securities did come with an additional prepayment risk and there were issues with the implied US government guarantee.

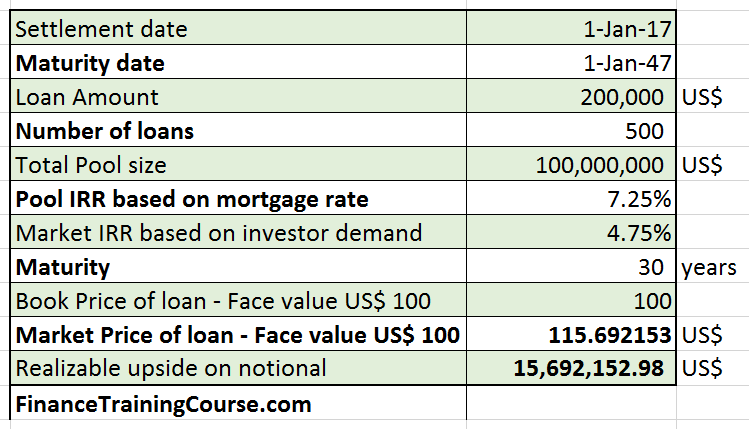

For banks the incentive to sell and securitize their pool of loans into a residential mortgage backed security (RMBS) structure was also simple. As long as banks carried the loans on their balance sheet they carried them at book value. But as investor demand drove yield on RMBS paper down, they had an opportunity to sell their loans at a premium and book that premium as a onetime gain. For example on a US$ 100 million pool originally booked at 7.25% for 30 years a bank could potentially book a gain of US$ 15 million if the benchmark RMBS paper was trading at 4.75%. This was more than sufficient to cover structuring, listing and transaction fees and leave the bank with a tidy gain. The gain was booked as a result of monetizing the difference between the actual yield on the loans and the yield at which investors were willing to purchase them.

This was a win-win situation for everyone. The banks could originate loans and then repackage and sell them. For investors there was a new type of a secured product that gave them access to investing indirectly in the housing markets. As more loans were securitized at market rates actual mortgage rates had an incentive to move south.

The only challenge was that with the pace of issuances we were quickly running out of inventory to securitize. Not every mortgage qualified for the government repayment guarantee. If it didn’t quality if was eligible to be pooled and sold through the government agencies operating in the securitization space. This was not necessarily a function of credit risk – part of the guarantee process was a desire to make housing accessible – so jumbo loans – large loans on large properties would not necessarily qualify.

Because the concept had worked in principle for federal housing agencies for the last two decades it was easy to replicate the model within the private sector. Players like AIG FP were willing to pick up the slack where the agencies were not willing to step in and participate. Between the insurers and the rating agencies the market figured out a model that would work for the banks as well as the investors.

However as the ineligible reasonable quality inventory dried up the race was on to relax underwriting quality by a notch and allow incrementally lower quality credit into the pools till either the rating agencies or the insurers noticed and yelled stop.

AIG FP and the rating agencies never woke up or rather never yelled stop.

And here is where the biggest transition happened.

As Mike Burry did his first trade with Goldman and wrote and bought his first Credit Default Swap (CDS) Goldman figured out a way to make money on both side of the transaction.

The transaction gave Mike the right to deliver to Goldman the reference security in question in the event of a default or a defined credit event. Mike didn’t own the security. He wanted someone to pay him the difference between what the securities were worth at the point of the trade and what they would be worth when they defaulted.

Goldman also didn’t own the security. Goldman had a synthetic claim on the underlying asset courtesy of Mike Burry. In case of default Burry would deliver the reference security to them. As the seller of the CDS Goldman would pay Mike Burry the notional amount and take possession of the underlying asset. Goldman could then deliver the underlying asset to a buyer who was interested in creating exposure to that asset class.

Mike burry was willing to pay a fee to someone to hold that asset for him till it fell. Goldman found buyers who were willing to take the other side of the trade. Investor who wanted exposure to the underlying CDO asset or security but couldn’t find physical inventory in the market. In return for taking the other side of the bet they could share in the fee Goldman was charging Mike Burry for the trade.

Enter the synthetic CDO. Nobody had to buy or hold or short sell the actual physical security. They just had to agree to exchange a notional payoff based on the actual realized return on the reference security. A paper trade without a real asset but a real market based payoff.

According to a post crisis Bloomberg interview Goldman did about $32 billion dollars of conventional and synthetic CDO’s. But we don’t have a breakdown of the synthetic figures in the article.