For business school students taking the treasury product exam or preparing for a trading desk interview, the USD JPY pair is particularly troublesome. Here is a list of common errors and challenges side by side with four simple examples for options on the USD JPY pair that we hope would clear the frustration around this pair.

1. Currency convention and intrinsic value

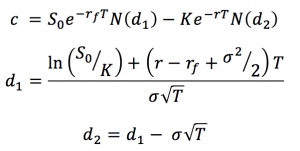

In general, the intrinsic value of a call option is max (ST-K, 0) while that of a put option is max (K- ST, 0)

For example when the call option is on USD (see example # 1), i.e. the buyer of the option will exercise the right to buy US dollars, and in return sell Japanese Yen when the spot exchange rate at maturity is greater than or equal to the strike or exercise exchange rate. But what is the appropriate convention for Spot and Strike exchange rates?

- If the exchange rate is expressed as the number of Japanese Yen per US Dollar the spot and strike exchange rates in intrinsic value and call option formulae should be used as is. The option will only be exercised if the value of the US Dollar appreciates against the Japanese Yen (or the Japanese Yen depreciates against the US Dollar) in relation to the strike exchange rate.

- For a call option on USD, the mistake is normally made when the exchange rate is expressed as the number of US Dollars per Japanese Yen, e.g. the strike rate = 0.009091 and the terminal spot =0.009174. Using the rates as is in the call option pricing formula without considering the logic behind the transaction or the appropriateness of the convention will result in an error. Simple application of max (ST-K, 0) would result in a positive payoff which would be incorrect. Logically, a rational buyer would not sell Japanese Yen (buy US Dollar) at a rate lower (higher) than the market rate. Convention wise, the exchange rates would need to be inverted first before application to the call option formula.

In like manner for the equivalent put option on JPY (see example # 2), i.e. the buyer of the option will exercise the right to sell Japanese Yen, and in return buy US dollars when the Spot exchange rate at maturity is less than or equal to the strike or exercise exchange rate. Again what is the appropriate Spot and Strike rate conventions?

- If the exchange rate is expressed as the number of Japanese Yen per US Dollar, the rates will need to be inverted before application in the put formulae.

- If the exchange rate is expressed as the number of US Dollar per Japanese Yen, the rates can be used as is.

For a put option on USD (see example # 3):

- If the exchange rate is expressed as the number of Japanese Yen per US Dollar, the rates will need to be used as is in the put formulae.

- If the exchange rate is expressed as the number of US Dollar per Japanese Yen, the rates will need to be inverted before application in the formulae.

For an equivalent call option on JPY (see example # 4):

- If the exchange rate is expressed as the number of Japanese Yen per US Dollar, the rates will need to be inverted before application in the call formulae.

- If the exchange rate is expressed as the number of US Dollar per Japanese Yen, the rates can be used as is.

In summary,

- For a call or put option on USD the currency convention that should be used in the option pricing formula is “the number of Japanese Yen per US Dollar”.

- For a call or put option on Yen the correct convention to use in the option pricing formula is “the number of US Dollars per Japanese Yen”.

2. Currency convention and risk free rates

After determining the appropriate currency convention to use in the option pricing formula, another point of confusion is with regard to the risk free rates. In particular, which currency’s risk free rate in the exchange rate pair is to be considered the domestic currency risk free rate, r, and which the foreign currency risk free rate, rf.

- When the currency convention used in the call and put formula is “the number of Japanese Yen per US Dollar”, the USD risk free rate is the foreign risk free rate while the JPY risk free rate is the domestic risk free rate. This is true for examples # 1 and # 3 below.

- When the currency convention is inverted in the call and put formula, i.e. “the number of US Dollars per Japanese Yen”, the JPY risk free rate is the foreign risk free rate while the USD risk free rate is the domestic risk free rate. This is true for the put & call options on Yen illustrated in examples # 2 & 4 below.

3. Calculating option premiums

After calculating the premium a common confusion is wrt the currency in which the premium is expressed. Again we look at the currency convention used in the call and put formulae.

- When the currency convention used in the call and put formula is “the number of Japanese Yen per US Dollar”, the resulting option premium will be expressed in Japanese Yen.

- When the currency convention used in the call and put formula is “the number of US Dollars per Japanese Yen”, the option premium is in US Dollars.

4. Total option contract value

Following on point 3 above, another error lies in calculating the total contract value of the option.

Given that the product term sheet uses the currency convention “the number of Japanese Yen per US Dollar” and that the notional amount is in USD terms (see examples below), how is total contract value to be assessed?

- If the currency convention used in the call or put option pricing formula is “the number of Japanese Yen per US Dollar” (as in the case for an option on USD) the result is a per unit value in Japanese Yen. Let’s call this value Y – A single 1USDxJPY contract results in an option value of Y in JPY. The total contract value in JPY terms will then be equal to the USD Notional times Y. Let’s call this value Z. Conversion to USD terms will be Z divided by the initial spot rate, where the spot rate is expressed as the “the number of Japanese Yen per US Dollar”.

- If the currency convention used in the call or put option pricing formula is “the number of US Dollars per Japanese Yen” (as in the case for an option on Yen) the result is a per unit value in US Dollars. Let’s call this value P – A single 1JPY/xUSD contract results in an option value of P in USD. The total contract value in USD terms will then be equal to the JPY Notional times P. Let’s call this value Q. To convert this value to JPY terms we divide Q by the initial spot rate, where the spot rate is expressed as the “the number of US Dollars per Japanese Yen”.

(1) is straightforward – you are using the USD notional amount quoted in the term sheet as is to determine the total contract value. (2) is where the confusion lies. If the Notional is USD1000 what should be the equivalent JPY Notional amount? Will USD notional be converted using the initial spot rate or the strike rate?

One way to decipher this is to think of how you would have to rewrite the product term sheet for the inverted currency convention with notional expressed in JPY terms at the same time maintaining equivalency between the two term sheets? What JPY notional will make the two product term sheets the opposite sides of the same coin?

The original term sheet speaks of an exchange of currency at a pre-defined strike exchange rate. In particular, for a call option on USD that is exercised, the customer will buy USD 1000 at the exchange rate of 110. This means he will sell JPY 110,000. In terms of equivalency (where a call option on USD is the same as a put option on JPY), this means that an exercised put option on JPY will see him selling sell JPY 110,000 at the exchange rate of 1/110 to fund a USD 1000 purchase.

The JPY notional amount used in 4(2) is therefore determined by converting the term sheet’s USD notional amount at the strike rate.

Example No. 1: Call Option on USD

Consider a 7-day at-the-money (ATM) European call option on the US dollars, to buy USD dollars for Japanese Yen. Suppose that the current USD-YEN spot exchange rate is 109.56, the exercise price is 110, the risk free rate in the United States is 1.15111% per annum and the risk free rate in Japan is -0.00086% per annum. ATM implied volatility in the USD-YEN rate is 11.82%. The notional amount is USD 1000.

We have:

S0 = 109.56

K = 110

r = -0.0000086, i.e. the Japanese Yen is the domestic currency

rf = 0.015111, i.e. the US Dollar is the foreign currency

T = 7/365 = 0.019178

σ = 11.82%

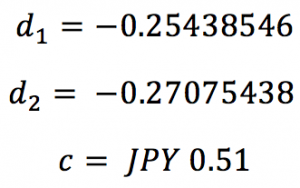

The price of the call option is:

Putting in the values we have:

Note that the call premium is denominated in Japanese Yen as the currency convention was USD-YEN (i.e. number of Japanese Yen per unit of US dollars).

The option value in US dollars for the contract = 1000*(0.505/109.56) = USD 4.614

Example No. 2: Put Option on JPY

The call option above is symmetrical and equivalent to a put option that sells Japanese Yen to buy US Dollars at the exercise price of 1/110. 110 was the strike or exercise price mentioned above for the call option.

The JPY notional value will be 110*1000=110,000

We have:

S0 = 1/109.56 = 0.0091274

K = 1/110 = 0.0090909

r = 0.015111, i.e. the US dollar is the domestic currency

rf = -0.0000086, i.e. the Japanese Yen is the foreign currency

T = 7/365 = 0.019178

σ = 11.82%

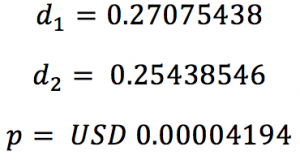

The price of the put option is:

Putting in the values we have:

Note that the put premium is denominated in US dollar as the currency convention in this case as YEN-USD.

The option value in US dollars for the contract = 110,000*0.00004194 = USD 4.614

Note that the put premium is denominated in US dollar as the currency convention in this case as YEN-USD (i.e. number of US dollars per unit of Japanese).

The option value in US dollars for the contract = 110,000*0.00004194 = USD 4.614

Summary A

| Call Option on USD | Put Option on JPY | |

| European option | Buy USD, Sell Yen | Sell Yen, Buy USD |

| Notional Value | USD 1000 | JPY 110,000 (at strike) |

| Strike | K = 110 | 1/K = 1/110 |

| Currency Convention | USD-JPY | JPY-USD |

| Domestic risk free rate | JPY | USD |

| Foreign risk free rate | USD | JPY |

| Premium in JPY | 0.505 | 0.505 |

| Contract value in $ | $4.614 | $4.614 |

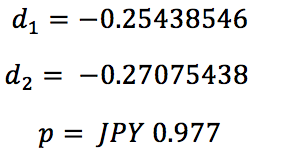

Example No. 3: Put Option on USD

Consider a 7-day at-the-money (ATM) European put option on US Dollars, to sell USD dollars for Japanese Yen. Suppose that the current USD-YEN spot exchange rate is 109.56, the exercise price is 110, the risk free rate in the United States is 1.15111% per annum and the risk free rate in Japan is -0.00086% per annum. ATM implied volatility in the USD-YEN rate is 11.82%. The notional amount is USD 1000.

We have:

S0 = 109.56

K = 110

r = -0.0000086, i.e. the Japanese Yen is the domestic currency

rf = 0.015111, i.e. the US Dollar is the foreign currency

T = 7/365 = 0.019178

σ = 11.82%

The price of the put option is:

Putting in the values we have:

Note that the put premium is denominated in Japanese Yen as the currency convention was USD-YEN.

The option value in US dollars for the contract = 1000*(0.977/109.56) = USD 8.920

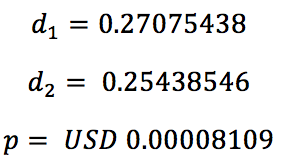

Example No. 4: Call Option on JPY

The put option above is symmetrical and equivalent to a call option that buys Japanese Yen and sells US Dollars at the exercise price of 1/110. 110 was the strike or exercise price mentioned above for the put option.

The JPY notional value will be 110*1000=110,000

We have:

S0 = 1/109.56 = 0.0091274

K = 1/110 = 0.0090909

r = 0.015111, i.e. the US dollar is the domestic currency

rf = -0.0000086, i.e. the Japanese Yen is the foreign currency

T = 7/365 = 0.019178

σ = 11.82%

The price of the call option is:

Putting in the values we have:

Note that the call premium is denominated in US dollar as the currency convention in this case as YEN-USD.

The option value in US dollars for the contract = 110,000*0.00008109 = USD 8.920

Summary B

| Call option on JPY | Put Option on USD | |

| European option | Buy Yen, Sell USD | Sell USD, Buy Yen |

| Notional Value | USD 110,000 (at strike) | USD 1000 |

| Strike | K = 1/110 | 1/K = 110 |

| Currency Convention | JPY-USD | USD-JPY |

| Domestic risk free rate | USD | JPY |

| Foreign risk free rate | JPY | USD |

| Premium in JPY | 0.977 | 0.977 |

| Contract value in $ | $8.920 | $8.920 |