Derivative Pricing – Interest Rate Swaps and Futures – Calculation reference

< 1 min read 1. Interest Rate Swap a. Net Cash Flow The net cash flow for the buyer of the contract (receiver of

< 1 min read 1. Interest Rate Swap a. Net Cash Flow The net cash flow for the buyer of the contract (receiver of

< 1 min read Black Formula’s and valuing Interest Rate Caps and Floors Value of a caplet The value of a caplet which resets

< 1 min read Here is the second course on Advance Interest Rate Products. The perquisite for this course is the first course on

3 mins read In this post, we look at how to price interest rate caps and floors using caplets and floorlets and Black’s

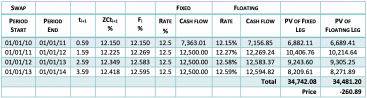

< 1 min read Amortizing Floating for Floating Currency Swap In an amortizing swap, the principal reduces in a predetermined way. For our illustration

< 1 min read Floating for Floating Currency Swap For our pricing example most of the assumptions will be the same as that used