Review of Financial Statements

Description: Builds on Key concepts explained in the previous session and explains the financial statements in detail

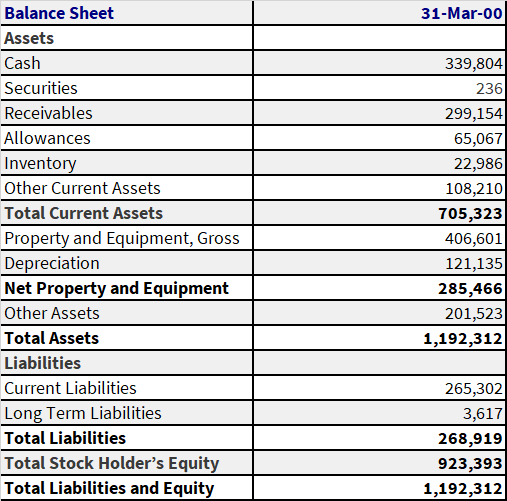

We present a sample balance sheet (format) below. An explanation follows of the various heads of accounts in the balance sheet.

Concept Title: Balance Sheet – Assets

Description: Defines and explains different types of assets.

Think of assets as anything & everything that a firm owns. Office space, furniture, vehicles, electronic equipment, printers, paper, cash… as long as they belong to a firm (not rented, not leased, not borrowed… the key word here is “owned”) they are assets.

There are two classes of assets on the balance sheet.

i. Current assets

This is a sub-class of assets, given special treatment in financial analysis. For reasons discussed below, current assets and their day-to-day management is an important factor in credit decisions by investors, lenders & suppliers. Four rules to remember current assets by

- Their life cycle or turnover (average life) is generally less than the operating cycle of the firm. For example, the average time that the same dollar of cash stays in the bank account is 15 days. This is the life cycle, average life or turnover for the cash at bank current asset. On a relative basis, they are easier to convert into cash compared to other classes of assets

- Again on a relative basis if the firm decided to close down and sell off everything, current assets are the most liquid assets.

- Current Assets also have sub-categories. The most common ones that you would see in financial statements are:

a) Cash and cash equivalents

Cash comes in many shapes and forms. The first is plain old cash. Dollar bills that you hold in your wallet or hands or under your mattress. Next in line is cash in bank, sitting either in your checking or your saving accounts. Further down the line are Marketable Securities, which are financial instruments (short term bank deposits, bonds, shares) that can be converted for their full value into cash within three to six months. Not all forms of cash are equal. Some are more accessible and more convertible than others.

b) Accounts receivable & Inventory

The other most common categories of current assets are Inventory & Receivables.

Inventory could be raw material, work in process (in the case of a manufacturing concern) or finished goods that are ready for production or sale. Accounts receivables are amounts that external parties owe you. For a Finance manager both of these assets come from a different bloodline than cash.

Unlike purebred cash, it takes time to liquidate these assets. Furthermore, under troubled conditions, it is not possible to realize the full value of receivables and assets. Although we generally perceive receivables to be more liquid than inventories, this depends on the nature of the business and the clientele of a firm. On occasion, what the firm carries in its inventory is more liquid than its receivables. This can happen when inventory has an easily determinable fair market value and is in demand. It can also happen if a firm followed ‘sloppy’ credit procedures resulting in an above average percentage of un-collectable accounts.

ii. Property Plant & Equipment

Also popularly known as Fixed Assets and PP&E (short form of Property, Plant and Equipment). How can you identify fixed assets?

- Unlike current assets, average life of fixed assets is beyond the operating cycle of the firm. Good examples are land, buildings, factory plants, motor vehicles, computer equipment, software, office furniture, etc. All of these assets have an average life greater than one year.

- If you know the firm’s accountant, here is a guaranteed way to impress him or her with your accounting knowledge. Ask if the item in question was expensed or capitalized. If it was capitalized it’s a fixed asset, if it was expensed there is a good chance that it is not.

The expensed or capitalized question asks if the cost of the asset was charged to a single year or spread over multiple years. If the it was spread over multiple years then it means that the asset in question will be or was used for more than one year. Traditional operating cycles of firms are less than one year implying that the asset’s life was greater than the operating cycle of the firm. Hence it’s a fixed asset. We show operating expenses in the income statement while we show capital expenditure in the balance sheet.

Concept Title: Depreciation

Description: Explains Depreciation and impact of different types of depreciation techniques on the Balance Sheet

An important concept related to Fixed Assets is Depreciation. We have touched above on distributing costs fairly over the life of a fixed asset. Depreciation is the mechanism that allows us to do just that in the case of Fixed Assets. It is an annual charge applied against the book value of the asset in question. It flows through as an expense on the income statement and is recorded as a negative asset on the balance sheet. You may have heard the term contra asset(s). A contra asset is an asset whose value is negative. It also refers to any amount that is shown on the balance sheet as decreasing the value of an asset. Depreciation is one example of a contra asset. Allowance for doubtful accounts is another.

Impact of Depreciation examples

The following example should help clear this point. Imagine a firm that buys a laptop for business use. The machine has a life of two years and costs the firm $3,000. The firm has two options: it can charge the whole amount in the first year or it can charge two equal installments for each of the years the machine is in use. Assume that the firm generated $6,000 in revenues each year and the laptop was the only expense. The Profit & Loss account for the two years for the first option looks like this:

Year One – without depreciation

Income 6,000

Expense 3,000

Net Profit 3,000

Year Two – without depreciation

Income 6,000

Expenses –

Net Profit 6,000

The P&L account under the second option looks like:

Year One – with depreciation

Income 6,000

Expense 1,500

Net Profit 4,500

Year Two – with depreciation

Income 6,000

Expenses 1,500

Net Profit 4,500

The actual profit for both the years is 4,500. With depreciation we get an accurate estimate of the actual profits. Without depreciation, we have depressed profits in the year of purchase, while inflated numbers in the following years.

Why is this important? Since actual earning drive the valuation of firms, reporting fair and accurate earnings is part of most accounting standards.

Test Problem:

1) Tweety, Inc. purchases a delivery van for $35000. It is decided that the life of the delivery van will be 7 years. What is the depreciation rate applied to the van?

- $0

- $5000

- $7000

- $35000

Basic Accounting Short Course for small business – Course Guide

Comments are closed.