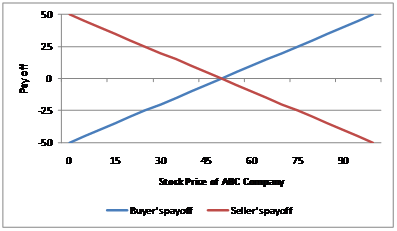

These are contracts where the buyer/ holder of the contract agrees to purchase while the seller / writer of the contract agrees to deliver a specified asset at some future specified time (the maturity date) for an exercise/ delivery price that is fixed today. Both parties to the contract are obligated to perform on the transaction.

These are not standardized contracts and are not traded on exchanges. They are over the counter contracts that can be customized to the specific needs of the parties involved. These parties are generally institutions.

Unlike the option contract however the buyer of the forward contract is not protected from prices move against his position. As he is obligated to perform on his transaction, the payoffs for buyer and seller of the contract are symmetrical, i.e. when the value of underlying assets changes in favor of one party to the contract the other party suffers and vice versa. That is it is a “zero sum” game.

Forward contracts are exposed to credit risk as either party can default on their obligation.

The payoffs are illustrated below:

Designated asset: 1 share of ABC company

Exercise price: 50 per share

In effect the seller of the contract “holds” the asset on behalf of the buyer during the period of the forward contract. This means that the buyer benefits from not having his money tied up in the asset so that he can invest it elsewhere. Additionally he does not have to incur storage cost (for physical goods). On the other hand by not holding the asset, he may lose out on some of the cash payouts on the underlying assets (e.g. cash dividend on stock) during the period of the contract and on convenience yields. Convenience yields are the value associated with holding the actual asset and therefore being able to bring it to use whenever the need arises, such as holding crude oil inventories that can be used in times of supply disruptions. Together these are known as the asset’s carrying cost.

Forward Price

At the inception of the forward contract the exercise/ delivery price is equal to the forward price and hence the initial value of the forward contract is zero. As the contract approaches maturity the delivery price remains unchanged but the forward price changes as the time to maturity shortens.

Forward price of a security with no income:

Where S0 is the spot price of the asset today

T is the time to maturity (in years)

r is the annual risk free rate of interest

Forward price of a security with known cash income:

(Securities such as stocks paying known dividends or coupon bearing bonds)

Where I is the present value of the cash income during the tenor of the contract discounted at the risk free rate.

Forward price of a security with known dividend yield:

(Securities such as currencies and stock indices)

Where q is the dividend yield rate. For a foreign currency q will be the foreign risk free rate.

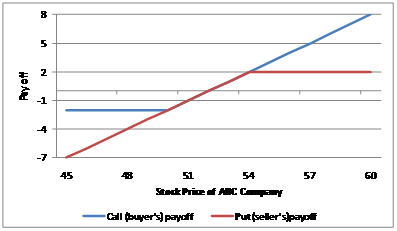

Synthetic Forward Contract

A forward contract can synthetically be created by writing/ selling a put contract and holding/ buying a call contract. The call and put are structured in such a way that the net cost is zero, where the net cost is the put option price less the call option price. The payoffs for the synthetic forward contract are given below:

Designated asset: 1 share of ABC company

Exercise price for call option: 50 per share

Exercise price for put option: 54 per share

Call and put option price: 2 per share

Forward Rate Agreement

This an over the counter agreement where by the interest amount that is paid (or received) during a specified future time period, on a principal amount borrowed (lent) is based on a predetermined interest rate. The FRA is generally settled at the beginning of the specified future time period, by discounting the present value of the settlement amount to the beginning of the period.

Comments are closed.