There are three major categories of derivative instruments- options, forwards and futures, and swaps. A quick comparison of their characteristics is given in the table below:

| Option | Forward | Future | Swap | |

| Downside Protection | ü | ü | ü | ü |

| Upside Potential | ü | |||

| Initial Cost | ü | |||

| Credit Risk | ü | ü | ü | |

| Customizable | ü | ü | ü | |

| Exchange Traded | ü |

Each category is described in more detail below:

Options

An option is a contract between the buyer / holder of the option and the seller / writer of the option that grants the buyer the right to purchase from, or sell to, the option seller a designated asset at a specified price (exercise / strike price) within a specified period of time. The buyer of the option pays the contract seller an option price or option premium for this right. Options are used for (1) Speculation or investment (2) Hedging or risk management.

The maturity date, or expiration date, is the date after which the option in no longer valid. American options are options that can be exercised at any time up to and including the expiration date. European options are options that can only be exercised on the maturity date.

A call option is one that gives the buyer the right to buy the instrument from the option seller at a specified price within a specified period of time.

A put option is one that gives the buyer the right to sell the instrument to the option seller at a specified price within a specified period of time.

While the buyer has the right to exercise the option, the seller of the option has the obligation to perform on the contract. This characteristic means that the buyer will only exercise the option when it is advantageous to him and will let it expire if conditions are not in his favor. However, the seller must deliver or receive the asset, whenever the option is exercised, even if this means he will make a substantial loss. This makes the risk/ reward relationship one sided or asymmetrical where the payoff in the contract tends to favor the option buyer.

In other words, the most the option buyer, i.e. the long position, can lose is the option premium in the event that he never exercises the option. However, if price of the underlying instrument moves in his favor, he has all the upside potential where his gains will only be reduced by the premium that he paid when he purchased the contract.

On the other hand, the maximum amount that the contract seller, i.e. the short position, can realize is the price he receives for the option contract. However, he is exposed to substantial downside risk as the option will only be exercised to the advantage of the option buyer or conversely the disadvantage of the contract seller.

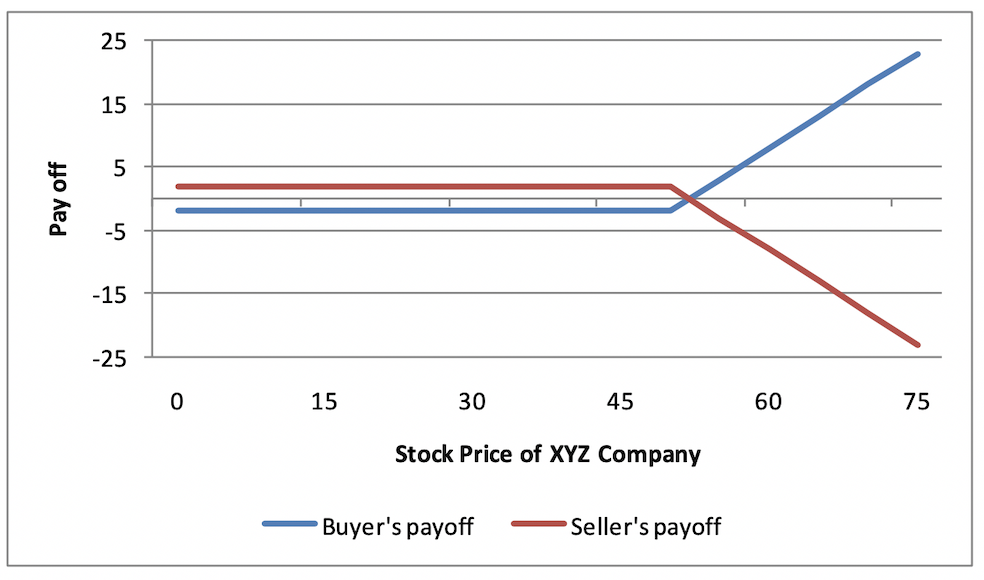

This is illustrated below for a call option:

Designated asset: 100 shares of XYZ Company

Exercise price: 50 per share

Option price: 2 per share

If the price of the shares rise to 55 and the buyer exercises his right, he will realize a profit of 300 [= (55-50-2) × 100]. The seller of the option will only receive 5,000 for shares worth 5,500 in the market. His total loss will be 300 [= (50-55+2) × 100].

On the other hand if the share price falls to 46, the buyer of the option will not exercise the option. The most that he will lose is 200, i.e. the option price. The seller of the option will only realize 200.

Per share payoff to the buyer and seller of the call option is depicted below:

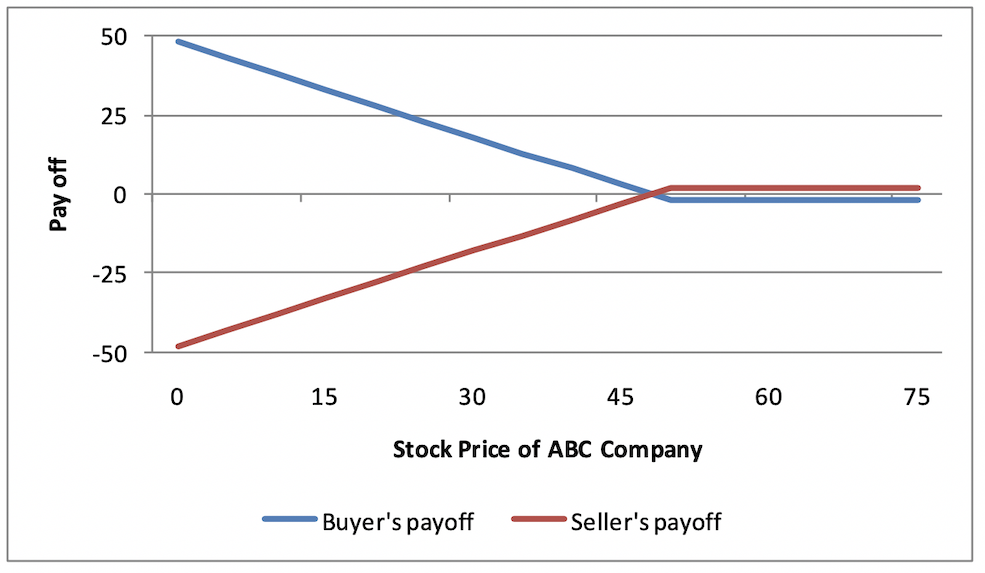

Payoffs for the put option are illustrated below:

Designated asset: 100 shares of ABC Company

Exercise price: 50 per share

Option price: 2 per share

If the price of the shares falls to 45 and the buyer exercises his right, he will realize a profit of 300 [= (50-45-2) ×100]. The seller of the option will be purchasing shares for 5,000 whereas if he were to go to the market for them he would have only to pay 4,500 in the market. There his total loss will be 300 [= (45-50+2) ×100].

On the other hand if the share price falls to 56, the buyer of the option will not exercise the option. The most that he will lose is 200, i.e. the option price. The seller of the option will only realize 200.

Per share payoff to the buyer and seller of the put option is depicted below:

Comments are closed.