Calculating Treasury profitability for FX deals.

Calculating Treasury profitability for deals on the treasury FX desk involves five simple steps:

- Separating treasury deals by deal types

- Separating treasury deals by currencies

- Comparing deal rates with closing rates or squared rates for the day

- Applying revaluation rates to calculate revaluation gain loss

- Calculating treasury profitability by bringing all four of these pieces together

Identifying Treasury Deal types:

Primary FX products and trades include:

- FX Ready: FX ready trades are usually used for hedging and speculation in foreign exchange. These are the simplest and most common foreign exchange transaction widely used by corporates to cover their receivables and payables. It involves the prompt exchange of one currency against another on the international or local market with settlement within two business days after the transaction.

- FX Forward: FX Forward trades are usually used for hedging and speculation in foreign exchange. These involve the exchange of different currencies with the exchange rate set at the present date and the maturity at some future date. Forward agreements guarantee the fixed exchange rate agreed at the inception of the agreement for a purchase or sale of a currency at a future date.

- FX Swap: A transaction in which two contractual parties agree to exchange a specified amount of one currency for another currency on future dates at a fixed price. Cash flows that can be exchanged are principal and interest (cross-currency swap), interest only (coupon-only swap) and principal only (principal-only swap).

- FX Placements/ Borrowings: Similar to the MM Call lending / borrowing transaction (given below), the only difference is that it is denominated in Foreign Currency. Mark-up calculations depend upon the day count of the currency of placement/borrowing.

- FX TMU – Import/ Export/ Remittance/ Encashment: Encashment are spot deals with Value dates equal to the deal date. FX TMU Imports, exports and remittance transactions can either be spot deals or forward transactions. The data that will be captured for this deal include:

- FX TMU – Foreign Bill Purchase (Bill Discounting): A Bill Discounting transaction is generally associated with an Import or Export payment. The customer will approach the bank’s treasury and request them to provide him with the local currency equivalent of the amount due now against the foreign currency that he will receive on the settlement date. On the settlement date whenever the FX currency amount comes in it is converted and sold to cover and discharge the liability of the customer.

- FX TMU – Close Out/ Take Up: A TMU transaction where a foreign bill purchased may be closed out (read matured) prior to its schedule maturity if the amount due comes in earlier.

Foreign exchange deals are typically categorized as either READY, SPOT, TOM or FORWARD where READY is defined as a deal that is executed on the day of the transaction (commonly referred to as settlement T+0) and forward means that the tenor and settlement is beyond T+2 where T is the date or day of the transaction.

| Deal type: | Definition: |

| Ready or Value Date Today (T or Transaction date) | This is an outright deal. The deal is completed on the day of the transaction |

| TOM (Settlement is T+1) | TOM deals have a one day tenor |

| SPOT (Settlement is T+2) | SPOT deals have a two day tenor |

| Forward (Settlement is beyond T+2) | FORWARD deals have a three or higher day tenor |

Identifying Treasury Deals by FX Currencies:

All foreign exchange deals can be classified as either a single currency deal (involves buying or selling a foreign currency in exchange for the domestic currency) or a third currency deal (involves buying or selling a foreign currency in exchange for another foreign currency).

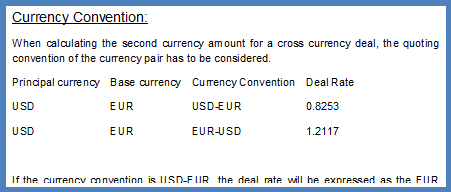

The main currency being exchanged is referred to as the primary currency and the currency used for the exchange is referred to as the base currency. All FX transaction use this convention.

| Deal | Buy Currency | Sell Currency | Primary Currency | Base Currency |

| USD-EUR (buy) | USD | EUR | USD | EUR |

| USD-EUR (sell) | EUR | USD | USD | EUR |

| EUR-USD (buy) | EUR | USD | EUR | USD |

| EUR-USD (sell) | USD | EUR | EUR | USD |

| USD-INR (buy) | USD | INR | USD | INR |

| USD-INR (sell) | INR | USD | USD | INR |

Irrespective of whether a deal is READY or FORWARD, identification of the components (buy currency, sell currency, primary currency and base currency) as shown in the table above is a required step in calculating profitability.

Treasury Deal rates:

Deal rate is the exchange rate at which the principal currency is bought or sold. Let’s look at a few examples.

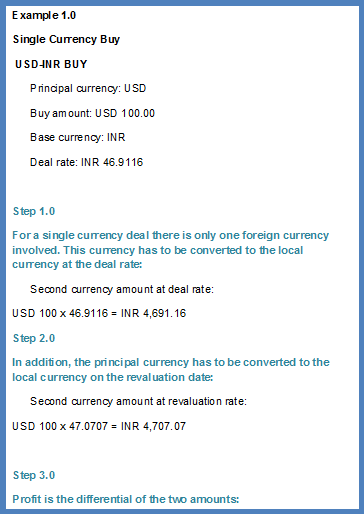

1)Single Currency Transaction – USD-INR BUY

- Principal currency: USD

- Buy amount: USD 100.00

- Base currency: INR

- Deal rate: INR 46.9116

- Second currency amount: USD 100 x 46.9116 = 4,691.16

This is a single currency deal. The deal rate is quoted in terms of the base currency, or the 1 unit equivalent of the principal currency. In this example, USD is being purchased at a deal rate of INR 46.9116.

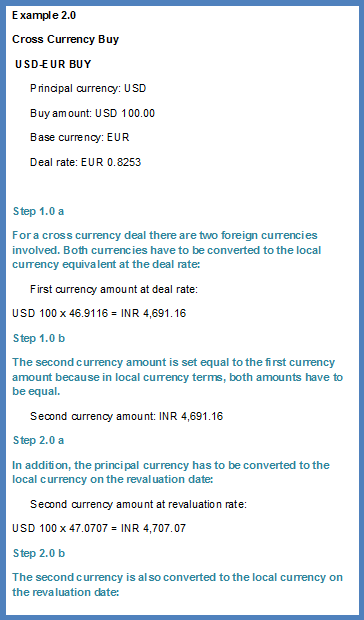

2) Single Currency Transaction – USD-EUR BUY

- Principal currency: USD

- Buy amount: USD 100.00

- Base currency: EUR

- Deal rate: EUR 0.8253

- Second currency amount: USD 100 x 0.8253 = EUR 82.53

This is a cross currency deal. The deal rate is quoted in terms of the base currency, or the 1 unit equivalent of the principal currency. In this example, USD is being purchased at a deal rate of EUR 0.8253.

Treasury Revaluation Rates:

Profitability is always calculated in terms of the local currency (Lets work with the assumption that INR is the local currency)

For a USD-INR deal, the USD-INR exchange rate is required to calculate the deal profitability.

For a USD-EUR deal, both USD-INR and EUR-INR exchange rates are required to calculate deal profitability.

For forward contracts, the relevant interpolated forward exchange rates need to be calculated based on the maturity tenor of the forward leg. These calculations are done using days to maturity and interest rate differentials across currencies.

Calculating Treasury Profitability:

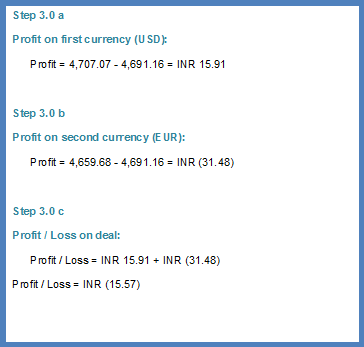

The profit on an FX deal is simply the inflow in terms of local currency minus the outflow in terms of local currency.

Profit on Buy = Revaluation Amount – Deal Amount

Profit on Sell = Deal Amount – Revaluation Amount

The revaluation amount for a buy deal is the amount that the bought currency will sell for the prevailing revaluation rate, hence considered an inflow. The opposite is true for a sell deal.

The deal amount for a buy deal is the amount that the bought currency is purchased for, hence an outflow. The opposite is true for a sell deal.

Putting it all together:

Please note that for all of the above deals the primary FX treasury profitability component is revaluation. For the multi leg swap transaction, one leg is valued as SPOT while the other is valued as a FORWARD contract.

For money market deals we also add accrual and amortization which don’t come into play for FX transactions. Accrual deals with the impact of accrued interest income on lending (or borrowing) and amortization deals with the adjustment of premiums and discounts on bonds.