After learning how to post entries in sales journal and sales ledger you should now feel comfortable if you are asked to post a transaction including credit sales.

Before we present you with an example, there is something important that you need to know. Businesses usually offer discount to their customers. There are two types of discounts that are offered by a business, trade discount and cash discount. Some businesses offer different discounts to different types of customers, e.g. 10% off to regular customers and 20% off to wholesalers etc. This is called the trade discount. Remember trade discount is never recorded in the books. Always record the transaction after deducting the trade discount.

The only discount that gets recorded in the books is the cash discount. It is the discount that is offered by businesses to their customers to act as an incentive to pay quickly. We will deal with this later when we will learn how to draw a cash book. For the moment just remember that trade discount is never recorded while cash discount is always recorded.

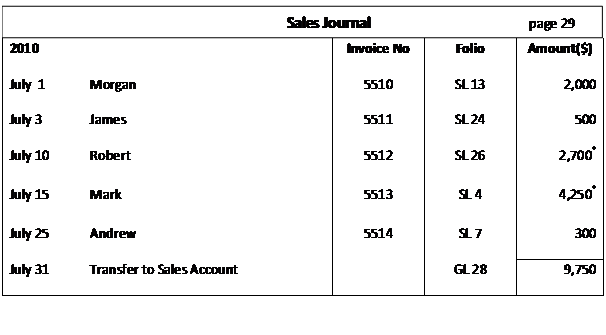

Let us consider an example. Rebecca runs a sporting equipment wholesaler. Following are all the credit sales she made during the month of July 2010. You are required to post these transactions in the Sales Journal, Sales Ledger and then at the end of the month post the total of sales in the General Ledger.

July 1 Invoice no 5510, credit sales to Morgan for $2000.

July 3 Invoice no 5511, sold $500 worth of inventory to James.

July 10 Invoice no 5512, sold $3,000 worth of goods to Robert. The amount includes 10% trade discount.

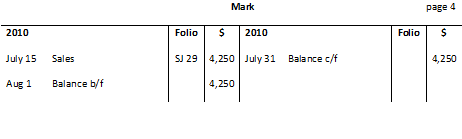

July 15 Invoice no 5513, sold $5,000 worth of goods to Mark, including 15% trade discount.

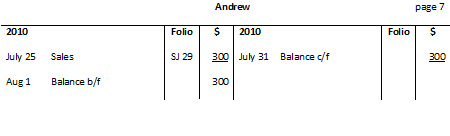

July 25 Invoice no 5514, sold $300 worth of goods to Andrew.

Let’s record these transactions, first in the sales journal and then in the sales ledger.

Sales journal

Note that the amount for the sales to Robert and Mark are different from the actual sales, this is because the amounts recorded in the sales journal do not include the trade discounts.

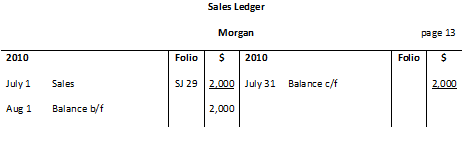

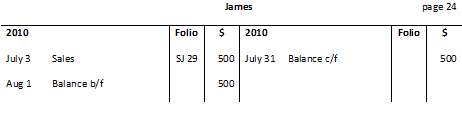

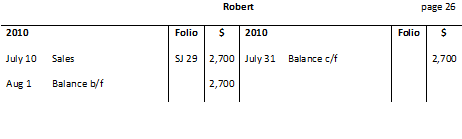

Next, we will make the personal accounts in the sales ledger.

Sales ledger for Morgan

Sales ledger for James

Sales ledger for Robert

Sales ledger for Mark

Sales ledger for Andrew

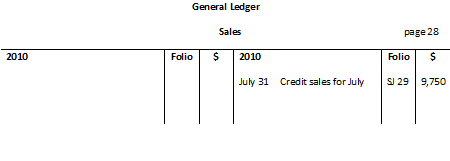

Finally, let’s transfer the total sales figure in to the Sales account in the general ledger.

Sales account in general ledger

This is all you need to know about the sale journal and sales ledger. In the next section we are going to examine the purchases journal and purchases ledger.

Comments are closed.