Accounting short course – Reviewing the Trial Balance

Let us consider a comprehensive example that uses everything that we have learnt up until now.

Following are the business transactions of a newly formed business setup by Andrew.

2010 Accounting transaction

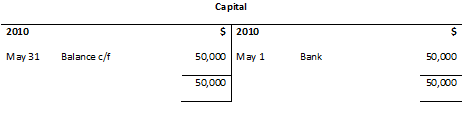

May 1 Started business with $50000 in the bank.

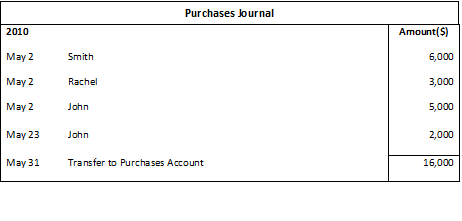

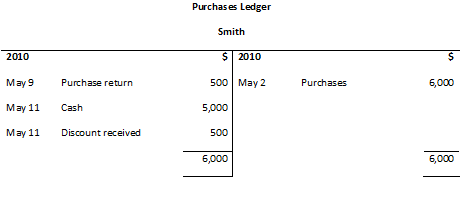

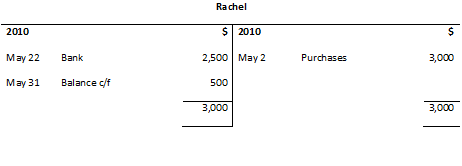

May 2 Bought inventory on credit from: Smith $6000, Rachel $3000, John $5000.

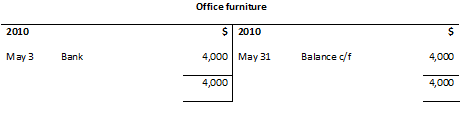

May 3 Bought office furniture for $4000 paid by bank.

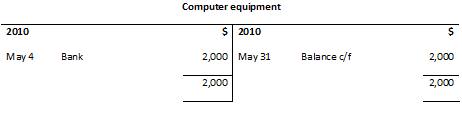

May 4 Bought computer equipment for $2000 paid by bank.

May 5 Sold inventory on cash for $500.

May 6 Withdrew $6000 cash from the bank.

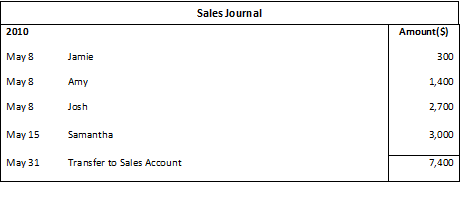

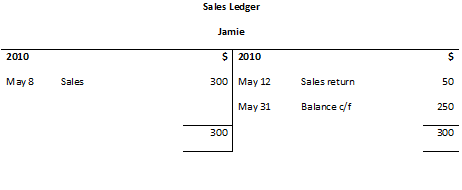

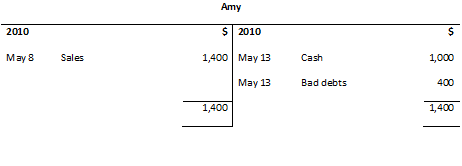

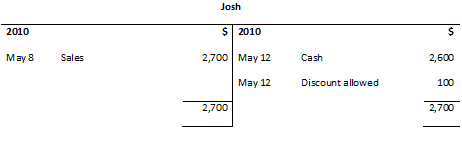

May 8 Sold inventory on credit to: Jamie $300, Amy $1400, Josh $2700.

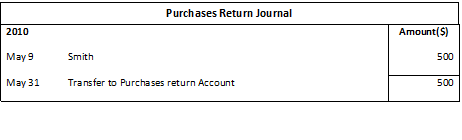

May 9 Returned inventory worth $500 to Smith.

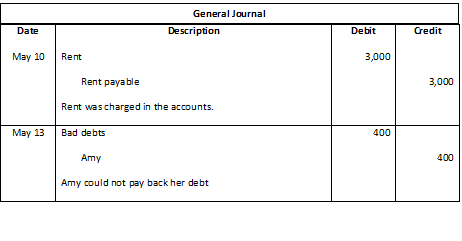

May 10 Rent of $3000 was charged in the accounts.

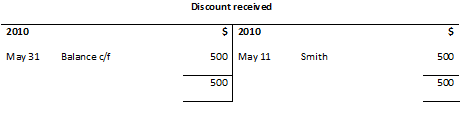

May 11 Paid $5000 cash to Smith, who allowed us a discount of $500.

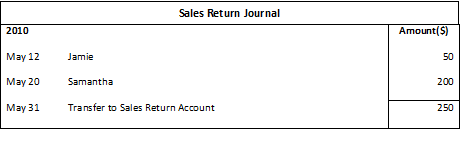

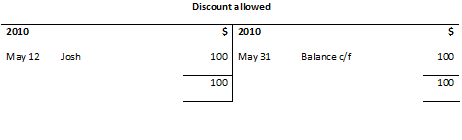

May 12 Jamie returned goods worth $50 while Josh paid $2600 cash for his account as he was allowed a $100 discount.

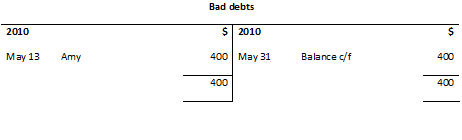

May 13 Amy has become bankrupt and can only pay $1000 cash. The rest is to be treated as bad debt.

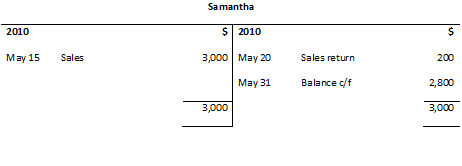

May 15 Sold goods on credit to Samantha $3000.

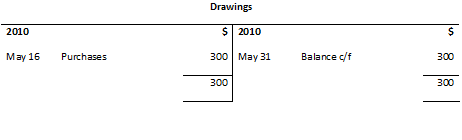

May 16 Withdrew $300 worth of goods for personal use.

May 17 Cash sales of $1300.

May 18 Paid rent by cash.

May 20 Samantha returned goods worth $200 to us.

May 22 Paid Rachel $2500 and John $3500 by cheque.

May 23 Bought goods on credit for $2000 from John.

May 25 Paid electricity bill of $800 by cash.

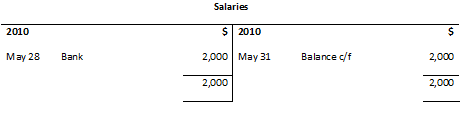

May 28 Paid salaries to employees $2000 by cheque.

You are required to record all these transactions in the relevant books and accounts and then draw a trial balance as at 31 May 2010.

Let’s start with all the journals and then draw up all the accounts in the ledgers. We will be ignoring the folio and the invoice no columns for the moment.

Sales journal

Purchases journal

Sales return journal

Purchase return journal

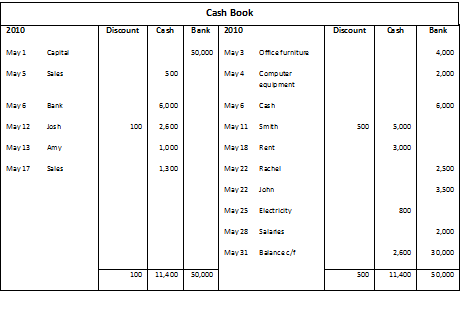

Cash book

General journal

As we can see that there is nothing new here. We have been learning how to record these transactions in the past few sections. Let’s record these transactions to the ledgers.

Sales ledger for Jamie

Sales ledger for Amy

Sales ledger for Josh 1

Sales ledger for Samantha

Purchases ledger for Smith

Purchases ledger for Rachel

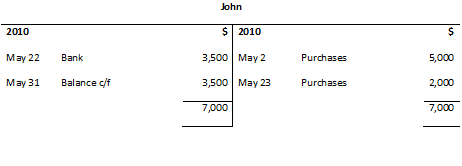

Purchases ledger for John

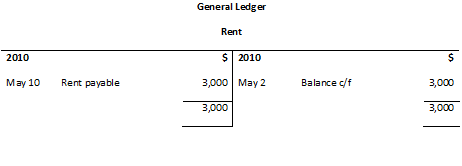

Rent account

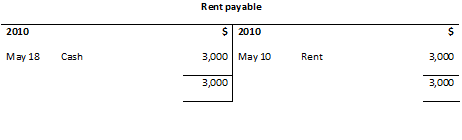

Rent payable account

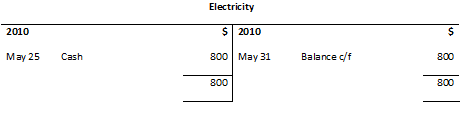

Electricity account

Salaries account

Office furniture account

Computer equipment account

Drawings account

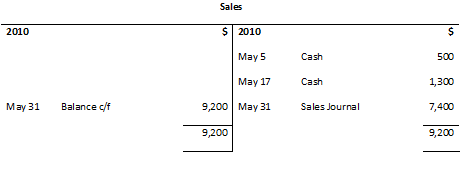

Sales account in general ledger

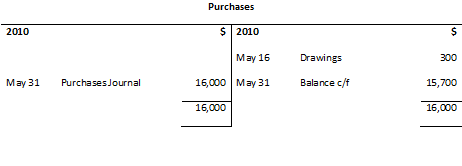

Purchases account in the general ledger

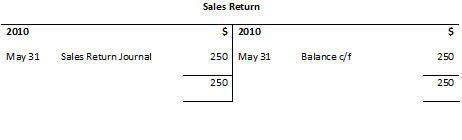

Sales return account

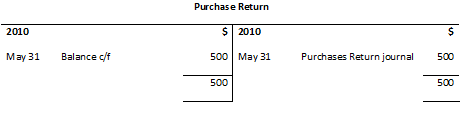

Purchase return account

Bad debts account

Capital account

Discount allowed account

Discount received account

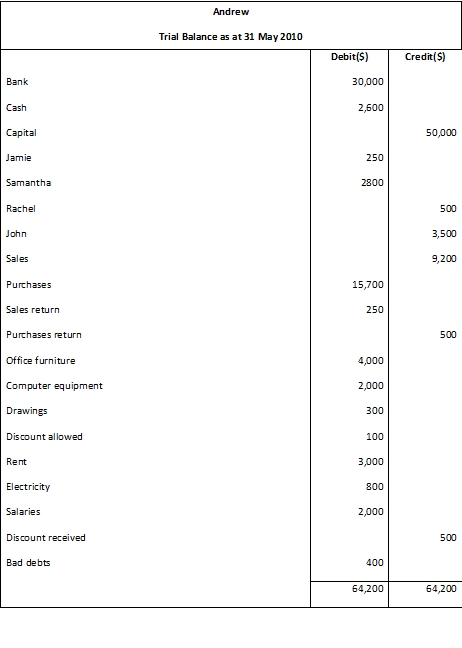

Now that we have recorded all the transactions in the books, we are in a position to draw up a trial balance for the month.

Trial balance as at 31 May 2010

You can see that both the debit and the credit side match, which means that there are no immediately visible. Having said that, there are still some errors that will not affect the trial balance and will not be detected by a cursory review of the trial balance. Some examples of such errors include:

- If we forget to enter a transaction completely in the books, it won’t affect the trial balance’s balance.

- Putting a transaction into an expense account when it was needed to go into the asset account.

- If two errors compensate each other, they will not affect the trial balance.

- If we completely reverse the order of the entry, it will also not affect the trial balance.

Even with all its limitations, trial balance still remains a very useful tool for checking the efficiency of double entry system of the business and is drawn by many businesses on a regular basis. Review of a trial balance is a core pillar of accounting process and control.

Very Nice & usefull content , thanks for uploading , just my suggestion is that if you could suggest a software or attach excel sheet to download for filling examples and practice will be great. thanks

Thank you Malik. Working on the spread sheet. Will have it up and running by the end of this month Inshahallah.

Warm regards

Jawwad