Basic Accounting Crash Course: Cash Book and recording cash discounts

Up until this point we have only dealt with credit transactions. We haven’t dealt with any cash. We will now be learning how to record cash transactions. All the cash (or for that matter bank) transactions are recorded in the cash book. Following is an excerpt from a typical cash book.

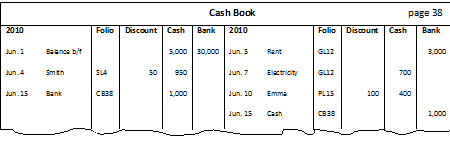

Cash book excerpt

Within the cash book you are familiar with the folio column. The discount column on the left side is the cash discount that we give to our customers. Businesses usually give discounts to their customers to act as an incentive for making payments quickly. For example, a business might allow $50 off for payments within 10 days of purchase. This is called cash discount. We record discounts that allow or ‘discount allowed’ on the debit side of the cashbook and ‘discount received’ on the credit side. For an example consider the two transactions, one on 4 June involving Smith and the other on June 10 involving Emma. By looking at the first transaction we can tell that we received a payment of $950 from Smith within our account receivable. The fact that $50 is under discount tells us that Smith was supposed to pay $1000 but we allowed him a discount of $50. Similarly, in the other transaction involving Emma we were supposed to pay Emma $500 but we received a discount of $100 from Emma.

If we do not record discount anywhere then this will cause problems. Imagine, in Smith’s case when we would have sold inventory worth $1000, we would have credited sales and debited Smith’s account by $1000. Now at the time he makes the payment, if we do not take into account the $50 discount we would be only recording $950 (as that is the cash we received) and Smith’s account will still be in debt by $50. This is why we have to record all the cash discounts. Discount received and discount allowed accounts are found in the general ledger. So in summary, in Smith’s case when he would make the payment, we will debit cash by $950 and discount allowed by $50 and credit Smith’s account by $1000. Discount allowed is our expense while discount received is our income.

Just to understand how cashbook works lets go through all the transactions listed in the above cashbook one by one. First consider the debit side. On June 1 there is a balance b/f of $5,000 cash and $30,000 bank, meaning we have these balances with us at that time. Note that balance b/f can also be credit for bank, in which case it will be bank overdraft and will be a liability. We have already talked about the transaction on June 4 involving Smith. On June 15 we have withdrawn $1,000 from the bank account. This reduces the bank account by $1,000 while increases the cash by $1,000. We have credited bank and debited cash by $1,000.

Now on the credit side, we have paid the $3,000 in rent on June 5 through bank. This will debit rent account in the general ledger (since rent is an expense and an increase in expense is debited) and will decrease bank by $3,000. Similarly, on June 7 we paid $7,000 cash for electricity. We will debit electricity account in the general ledger and credit cash by $7,000. On June 10, we made a payment to one of our accounts payable Emma. We were supposed to pay $500 but we paid $400 and were given a discount of $100.