Market structures and systemic risks of exchange traded funds

This article summarizes the Bank of International Settlements working paper No.343 titled “Market structures and systemic risks of exchange traded funds”. The paper defines what exchange traded funds (ETFs) are, particular in the US and Europe and presents certain differences in structure between these two regions. In particular it presents three operational structures for ETFs, the first a plain vanilla physical replication scheme structure followed by two synthetic derivatives replication structures. It discusses the motivations and reasons behind the evolvement of these more complex synthetic structures and then based on lessons learned from the current financial crisis outlines potential risks to global financial stability that may arise in the future given the continuing proliferation and demand for these schemes.

Exchange Traded Funds (ETFs)

ETFs are structures as open ended mutual funds. The provide investors with the opportunity of diversifying their portfolios by giving access to financial assets from various regions, sectors and asset classes. They are similar to stocks in that they can be traded on organized exchanges through brokers who operate on a commission basis. Investors can take long and short positions in ETF shares; they can execute market, limit and short orders; they can purchase the shares on margin.

Operation Structures

Physical replication schemes

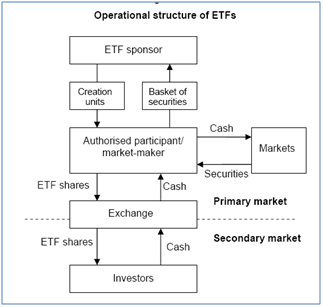

The original plain vanilla structure for ETFs were physical replication schemes- the market makers would exactly replicate the ETF index by purchasing all the underlying assets that make up the index.

In these structures Authorized participants (or market markets) purchase a basket of securities that replicates the ETF index and then delivers this basket to the ETF sponsor. In return the ETF sponsor provides the Authorized participant with Creation Units. The ETF sponsor can redeem the Creation Units through securities that comprised the ETF rather than through cash. This activity occurs in the ETFs primary market.

Investors operate or function in the Secondary market for ETFs and have no interaction with the ETF sponsor. They trade in shares of the ETF through brokers or exchanges and therefore do not incur redemption or subscription charges. The Net Asset Value (NAV) of the ETF shares is based on the market value of the basket of securities underlying the fund. The above structure is summarized in the paper by the following figure.

Source: BIS Working Papers No. 343- “Market structures and systemic risks of exchange traded funds”

Some modifications to this physical replication scheme model is that certain market makers may instead choose to purchase an optimized portfolio of assets instead of an exact replica of assets. This optimized portfolio is determined using various portfolio allocation strategies that minimize the tracking error between the performance of the ETF index and that of the replicated portfolio. Using these modified schemes would also allow security lending in order to generate additional income.

Synthetic and Exotic structures

These structures difference from the physical replication structures in that they use derivative instruments such as total return swaps or equity linked notes to replicate the performance of an ETF index instead of owning the physical assets that comprise the ETF. Two types of structures outlined in the paper are 1) the Unfunded swap structure and 2) the Funded swap structure.

Unfunded Swap Structures

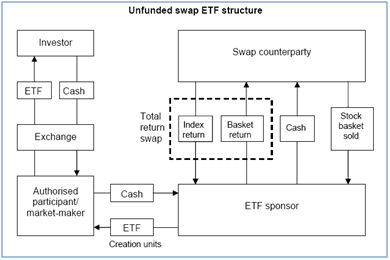

The unfunded swap structure discussed makes use of a total return swap. In this structure the Authorized participant pays Cash to the ETF sponsor instead of purchasing and transferring a basket of securities to him, in return for receipt of Creation units. The ETF sponsor then enters into a total return swap arrangement with a financial intermediary, the swap counterparty, usually its parent bank. The two legs of the swap transaction are as follows:

- 1st Leg: ETF sponsor will receive the total return of ETF index for a given notional exposure and pay Cash to the financial intermediary equal to this notional exposure

- 2nd Leg: The financial intermediary will transfer a basket of collateral assets to the ETF Sponsor and will receive the total return of this basket form the ETF Sponsor

The assets that are transferred to the ETF sponsor by the swap counterparty do not need to match those that comprise the ETF index, infact they can be quite different. In addition the swap counterparty can change the composition of the basket assets on a daily basis. The ETF sponsorare the beneficial owner of the basket which means that in the event of counterparty default they may sell the assets to repay their investors. Security lending is permissible. For the swap counterparty as this is a true sale of the assets to the ETF sponsor this sale could have an impact on their risk-weighted capital charges. The above structure is summarized in the paper by the following figure.

Source: BIS Working Papers No. 343- “Market structures and systemic risks of exchange traded funds”

Funded Swap Structures

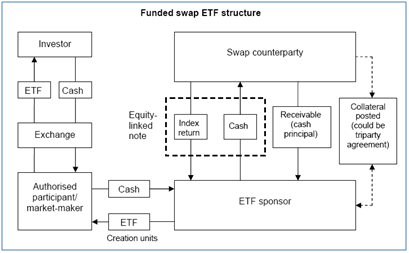

The funded swap structure discussed makes use of a credit- or an equity linked note. This structure is similar to the ETF sponsor purchase a structure note that is security by collateral pledged by the counterparty. The Authorized participant pays Cash to the ETF sponsor and in return receives Creation units. The ETF sponsor transfers this cash to the swap counterparty for which he will receive the total return of the ETF index. On termination of the arrangement the counterparty repays the principal amount of cash. The swap counterparty pledges collateral (usually held in a custodian account by a third party). The ETF sponsor has a legal claim to these collateral assets but is not the beneficial owner of them. This means that in the event of a default by the swap counterparty there could be delays in realizing the value of these assets to repay investors. The collateral basket tends to be overcollateralized (up to 120% of the ETF’s NAV). For the swap counterparty in this instance as there is no true sale of assets to the ETF sponsor, there is not likely to be an impact on it risk weighted capital. This structure is not as commonly used by ETF sponsors as compared to the unfunded structure. The above structure is summarized in the paper by the following figure.

Source: BIS Working Papers No. 343- “Market structures and systemic risks of exchange traded funds”

Other structures

- Synthetic structures for commodities – Physical replication is possible for more liquid indices such as gold and copper however, for other commodity indices, synthetic replication structures using forwards and futures contracts are more common

-

Exotics – greater product complexity and investor risk; actively traded (constitutes 20% of the turnover of total ETF assets)

-

Leverage ETFS – return is a multiple of the ETF index’s daily performance

- Path dependent returns- investor exposure similar to Asian options

- Inverse leverage ETFs – return is a multiple of the inverse of the ETF index’s daily performance

- Options of ETFs – American style exercise feature with expiration schedules the same as exchange traded options

-

Why ETFs

- A weak investor appetite for structured credit products after the financial crisis

- Low global interest rates and a need for higher return alternatives

- Cost- and tax-efficient alternatives to mutual funds

-

Product innovation led to synthetic & exotic versions – The reasons/ motivations for these innovations include:

- Greater demand for ETFs by investors by a limited supply and/or liquidity of underlying assets

- Need to greater liquidity in diversified asset classes

- Reduced costs for ETF sponsor/ Authorized participant – for tracking broad market or less liquid indices physical replication structures can be expensive

-

Cost saving for swap counterparty

- Less liquid stocks and bonds require larger haircuts. Transferring these assets via collateral to the ETF sponsor may result in lower warehousing costs for these assets for the parent bank (swap counterparty).

- Can fund lower and illiquid assets more cheaply using this option as compared to the unsecured or repo markets.

- If collateral assets are of lower quality and/ or are less liquid than those needed for a physical replication structure, the synthetic structure could lead to lower regulatory capital charges

- In volatile market conditions, physical replication schemes that rely on optimized baskets can lead to greater tracking errors

- Alternative funding sources to meet LCR standards under Basel III which could lower the cost of compliance, e.g. a reduction in the run-off rates on the collateral posted

- ETF’s parent (the swap counterparty) can use this as a way to cheaply fund their warehoused securities

-

Tracking error risk transferred from investor to swap counterparty

- Increased counterparty risk

What risks do synthetic and exotic ETFs pose to financial stability?

- Lack of transparency of the underlying assets and markets and how swap counterparties replicate the ETF index and complexity of structures would make risk assessment difficult. No investor monitoring. Notions that ETF markets are liquid (even when collateral pledged may be illiquid)

- As tracking error risk is passed to counterparty there is a risk that underperformance might be co-mingled with the rest of the financial intermediary’s trading book risk. This would be compromise to risk management and oversight.

- At present there are no restriction mechanisms in place for investor withdrawal. The ability of the financial intermediary to effectively manage counterparty risk as well as market making in the event of a run on the bank has not been tested.

- The recent financial crisis showed us that in the event of counterparty risk institutional investors are usually the first to withdraw funds. Also there were instances when defaulted counterparties’ pledged collateral assets were frozen and made inaccessible to the investors. This made the overcollateralization requirement redundant as it failed to protect investors. Allowing securities lending could worsen a default situation as it may be difficult to access assets when they are needed to repay investors.

- Investors are charged for receiving a more liquid alternative, i.e. the total return on a trade-able ETF index portfolio. For this they pay cash which is a cheap source of funding for the swap counterparty. However in the event of sudden and large investor withdrawals the swap counterparty could be exposed to an increased funding liquidity risk because adequately charged for this liquidity option.

- Using illiquid assets as collateral assets in order to meet LCR standards and reduce warehousing costs, etc could further increase counterparty risk in stress situations.