This Treasury training session is based on a single session transcript of our 5 session Cross Selling Treasury Products Training Video. Also see our free treasury risk training resource, if you like this post.

Session IV of Cross Selling Treasury Products Video Course: Core Treasury products and TMU customer reactions

Hello and welcome to our session on selling treasury and derivative products. As part of this session we plan on quickly walking through a list of base line scenarios that you are likely to experience when you engage or represent the treasury sales or treasury marketing unit (TMU) in front of a customer.

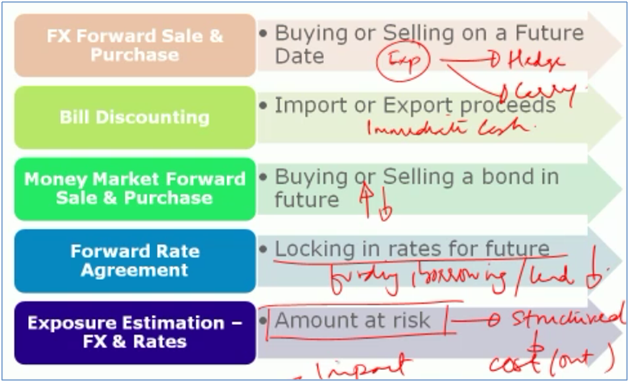

In this list the most common transaction that you are likely to see as part of your work is FX Forward Sale and Purchase transaction and a simple example will illustrate what we mean by this structure.

Imagine that you have a customer who needs to sell a million Euros and convert into Dirhams (AED) or Saudi Riyal (SAR). The challenge that this customer has is that this transaction is going to happen 90 days down the road. Using dirhams the current exchange rate is 5 Dirhams for a Euro. Since the client is in the market to sell, his primary worry is that over a period of time, especially the next 90 days the Euro is possibly going to plunge sharply. If he sells the Euros now at today’s rate he would get 5 million dirhams, but if say the rate falls to about 4.1 (or 4.2) then rather than getting 5 million he may only get 4.1 million dirhams, which is almost a 20% reduction. He would rather opt for a structure where this risk of losing 20% of value over the next 90 days is reduced.

If I summarize this, there is an amount that is due on a future date and the primary risk is price risk. The client is worried about volatility in prices and exchange rates. The structure to suggest to this customer is, let us enter into a forward contract where I agree to buy 1 million Euros as a bank from you at a fixed exchange rate. 90 days down the road I am actually willing to buy a million Euros from you at a rate of 4.95, which locks you in at this level and ensures that irrespective of what happens to rates whether they go up or come down you will be guaranteed a payment of 4.95 million Dirhams for selling 1 million Euros.

If you revert this transaction, if you turn it around on its head you could do it the other way where you [client] would agree to buy a million Euros at a know rate. (As a client) Rather than selling a million euros the client needs to buy a million Euros and is worried about the Euro rate going up rather than coming down.

The FX Forward Sale and Purchase transaction is generally the most common transaction you will see as part of your work, but there is another variation of this transaction which is a little different and this is known as Bill Discounting (aka LC Bill Discounting). Rather than looking at outright sale purchase or sale purchase over a period of time, as sale purchase deferred at some point in time in the future, a Bill Discounting transaction is generally associated with an Import or Export payment. I have gone out and shipped one million barrels of oil and against this a payment is due. I’ve gone out and bought 10 new Porsche 911’s, I’ve gone out and purchased a shipment of the latest iPhone 5 or the next generation iPads. And against all these purchases a payment is due.

Let us assume that you have gone out and sold a product worth a million Euros and a payment for this million Euros will now be made to you somewhere over the next 90-180 days. The problem is that you can’t afford to wait that long and you would rather have cash now. You go to you bank. In this specific case the shipment has been done against a letter of credit (L/C). You ask the bank, “look I am going to get this cash 180 days down the road; it’s going to be in a foreign currency; can you give me a local currency equivalent amount today? At the end of 180 days when this money comes you can use this to discharge my liability”.

Structure wise, mechanics wise the basic principle between the FX Forward Sale Purchase and a Bill Discounting transaction is the same but the net impact is very different. In the FX Forward Sale transaction the money comes at the end of 90 days and it is set at a fixed exchange rate. In a Bill Discounting transaction the money comes at the end of 90 days but the cash equivalent is given to the customer today. At the end of 90 days or 180 days whenever the FX currency amount comes in it is converted and sold to cover and discharge the liability of the customer. This is structured in such a fashion that the bank carries no exchange risk on taking on the exposure of receiving a million euros at the end 90 or 180 days.

The third transaction that you see when you work or represent a treasury sales unit or treasury marketing unit is when customers are in the market to buy or sell a fixed income instrument on a future date [Money Market Forward Sale & Purchase Transaction]. I have a ten year bond and my worry is that rates are going to go up and as rates go up the value of this bond will come down. Rather than waiting for rates to go up I actually want to lock in the value I can get for this bond today and agree on selling or (purchasing or buying) or disbursing or getting rid of this specific instrument in my portfolio at a rate that we’ve agree upon today, but on a future date. Similarly, if I expect rates to come down and I expect prices to go up, rather than wait for rates to come down and prices to go up I actually want to enter into a transaction where I can buy this instrument at a future date, today.

There is something to be said about whether the market is able to price this opinion, whether the market is able to price the expectation that rates are going to go up or come down in its pricing and whether you can actually go out and beat the market. But at the same time there are opportunities and there are reasons, and there are scenarios where a customer is not interested in making money from the transaction but much more interested in making sure that he is locked in at a fixed level and that there is no variation from the amount that he has budgeted for that specific transaction.

A variation on the Money Market Forward Sale Purchase transaction is the Forward Rate Agreement. In this specific case, I want to borrow a billion US dollars. I am concerned that while [interest] rates right now are low, they may go high. What I want to do is create a hedge for this change, this expected future change in interest rates in such a fashion that my cost is locked in even if [interest] rates go up. This is known as a Forward Rate Agreement or a FRA.

The common theme across all of these four scenarios or instances that we’ve looked at is “how do you estimate the amount of money the customer is likely to lose, i.e. the estimated approximate loss, or the exposure?” So, on a forward sales deal what is the most that you can lose? On the bill discounting transactions what is the most that you can lose? On a money market forward sale and purchase transaction what’s the most that you can lose?

The exposure estimation on the FX rate side is the last and final piece. We have done some work on this in our Cross Selling Treasury Products course that is covered separately, but a large part of our work is dependent on completing this step.

The last piece is the exposure estimation exercise which is where we actually find out on the FX forward sale transaction what’s the most that you can lose? On the bill discounting transaction what’s the most that you can lose? On the MM forward transaction what’s the most that you can lose? And on the Forward rate agreement what’s the most that you can lose?

Answering this question is important for a range of reasons. For example on the FX forward sale and purchase transaction where I am buying or selling on a future date, the exposure estimation exercise allows me to determine what portion of my exposure am I willing to hedge and what portion of my exposure am I willing to carry on an as is basis. If you look at the bill discounting example where I am realizing on monetizing import/ export proceeds my primary reason is not a significant movement in rates but in immediate generation of cash. If I look at the MM forward sale transaction my primary interest is assessing the impact of interest rate movement on the value, the mark to market value or the price of my inventory. On the forward rate agreement side my basic objective is to lock in my funding cost, my borrowing cost for a given transaction. Alternatively I also want to lock in the rate at which I lend especially if I expect rates to come down.

To summarize, the principle objective of estimating the amount at risk in each of these transactions is to determine how the transaction should be structured and what would be the impact of the structure on cost both out of pocket and explicit cost as well as implicit cost and what is the long range impact on the customer’s portfolio and profile of the structure that you have suggested.

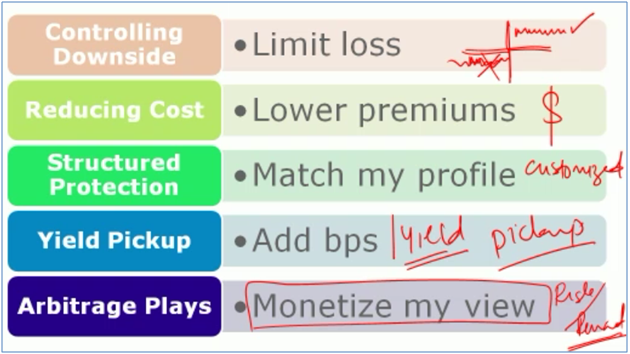

Once you have an answer to the exposure estimation question, and you come back to the customer and suggest “Look I am going to go out and suggest structure A”, a customer could come back and react in a number of different ways.

The most common reaction that you are likely to see is that the customer will come back and say “This structure is great, I really like it, it hedges my exposure but my primary problem is that I don’t like the downside. Let’s say this is the world and this is the best case scenario where I am making money under your suggested profile, I’m okay with this part. The part that I don’t like is the part where I actually go out and lose money. So can we do something to limit my downside?”

A second reaction that customers come out and say is “Love the structure, love the solution that you have suggested but my out of pocket cost is too much. Can you do something to reduce the dollar amount?”

Third reaction customers have is “What you’ve done works well for somebody who is looking for an off the shelf solution but I don’t want an off the shelf solution. Give me something that is customized to my needs.”

There are times when customers say “The only reason why I want to do this transaction or this trade is because I want yield, I am searching for yield. So if you can pick something up that’s fine, if you can’t then I’m not interested.”

And last and finally every now and then you come across a customer, and these are the customers that you have to watch out for, who wants to monetize his point of view. He wants to do it in such a fashion that from a risk/ reward point of view there is no change in his profile.

If I quickly take a step back at what we have looked at, we’ve said that there are FX forward and sale transactions as part of our base line set, bill discounting as part of our base line set, MM forward sale and purchase as part of our base line set, Forward rate agreement as part of our base line set. We can’t do any of these activities unless and until we understand what the customer is likely to make or lose in a range of different scenarios and how these products, or the products that we have suggested for these base line scenarios would perform.

Then we move on to gauging the reaction of customers to our product suggestions. We focused on the fact that a customer may come and say “Can you take what you have done and revise it so that my downside is limited? To doing something where my cost is reduced; to doing something where you have a customized profile for my needs; to doing something where you add a few basis points (bps) compared to the competition” and finally strategies and solutions where a customer has a specific point of view and wants you to help him monetize that.